Quarterly Economic Outlook : Rate cuts and politics continue to breed uncertainty.

It was an eventful third quarter, and the fourth quarter of 2024 promises to be at least as interesting. Central banks in most advanced economies have now joined the Bank of Canada (BOC) in cutting policy interest rates. The Canadian economy continued to avoid recession, while the U.S. economy continued to exhibit surprising strength. China finally pulled out the “policy bazooka” in an attempt to reinvigorate its economy and stock market. Finally, ongoing conflict in the Middle East intensified, creating a further push-pull in energy commodities. Against that eventful backdrop, elections are looming in both Canada and the U.S. We’ll explore the potential outcomes and also briefly revisit the Canadian housing market.

Paving the way for central bank easing

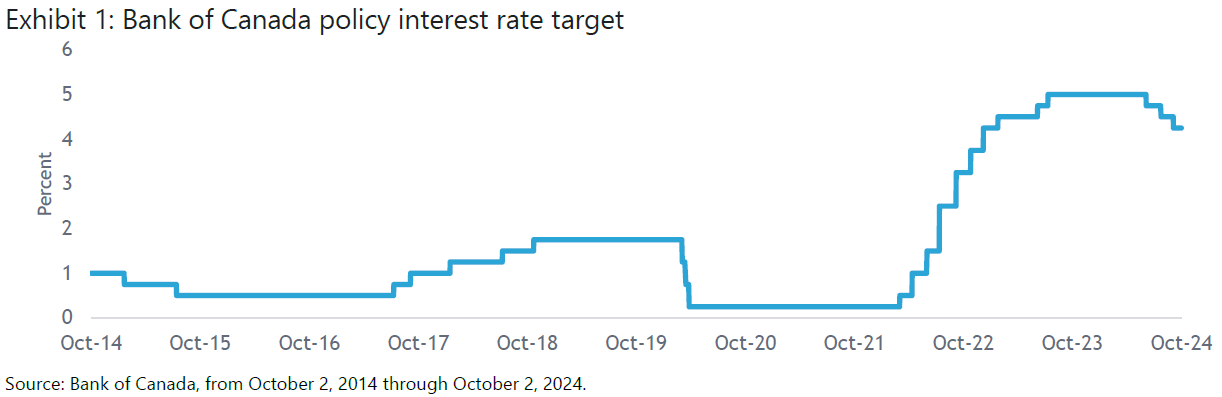

After leading the way with initial rate cuts this year, the BOC has now been joined by several other key central banks as inflation has continued to recede from the elevated levels of recent years. The BOC was able to continue lowering its interest rate target in the third quarter thanks to further progress on inflation (as well as lingering concerns about Canadian households and consumers), cutting in 25-basis point (a basis point equates to 0.01%) increments three times from July to September, as Exhibit 1 illustrates.

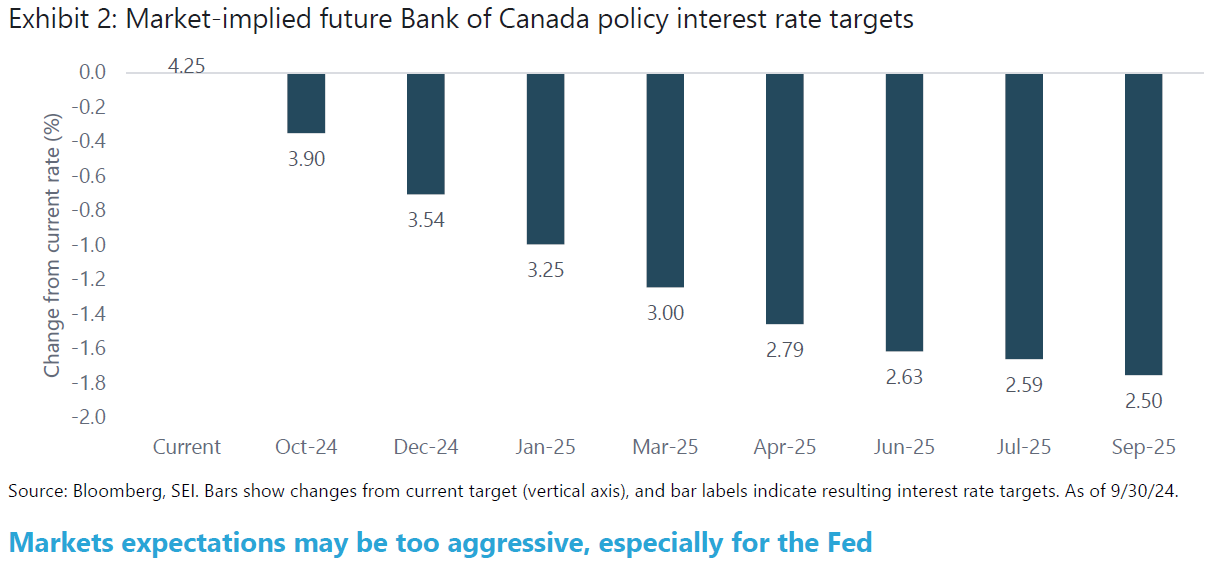

Meanwhile, markets expect the BOC to continue on this dovish path into late 2025, as shown in Exhibit 2.

Markets expectations may be too aggressive, especially for the Fed

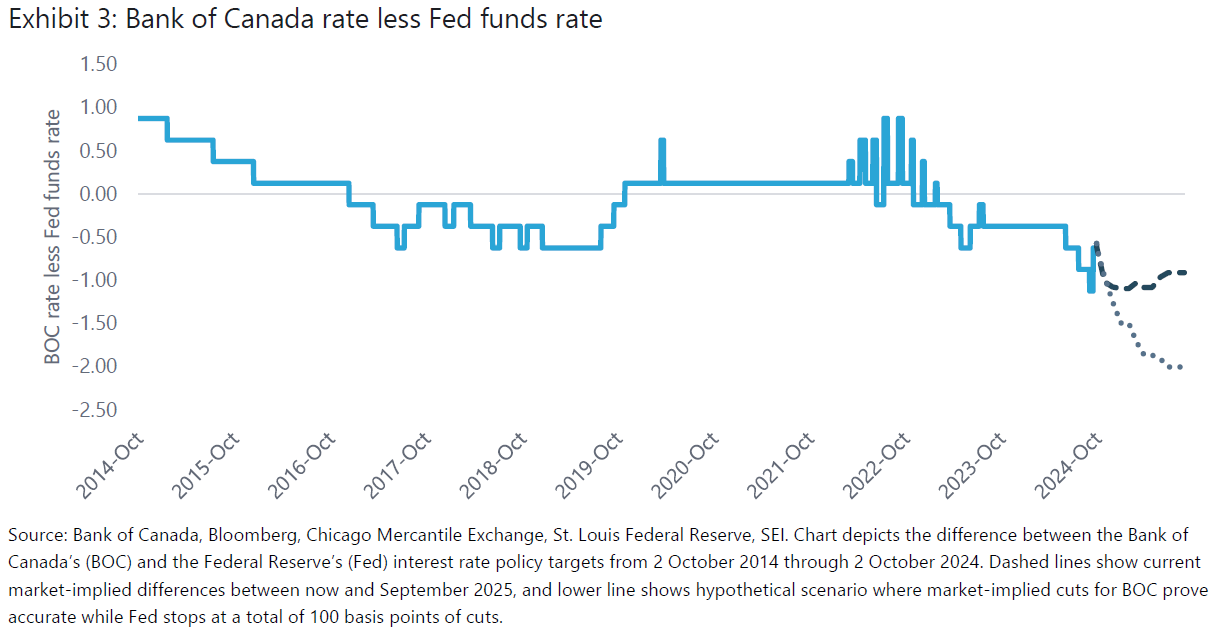

While Canada has made the most impressive progress against inflation among advanced economies, we continue to think the so-called “last mile” to many other central banks’ desired inflation-rate destinations could prove challenging, especially in the U.S. and perhaps in the U.K. as well. As expressed in the latest SEI Forward1, we believe markets are pricing in an overly aggressive number of rate cuts by the Federal Reserve (Fed) given the still-strong economic backdrop in the U.S. Should SEI be proven correct, that could pose a challenge to the BOC, as Canadian and U.S. interest rates have tended to track fairly closely in recent history. For example, as shown in Exhibit 3, the spread between the BOC and Fed policy rates has become fairly wide compared to the last 10 years. That will remain the case if recent market expectations prove roughly correct. However, if the Fed disappoints by keeping rates higher than expected, that would stretch the current rate differential even further. In Exhibit 3, we show how this situation might look if (for hypothetical and illustrative purposes only) the Fed were to cut only 100 basis points in total from September 2024 through September 2025 while the BOC adheres to market expectations. While by no means assured—the market’s current outlook for BOC cuts might also be overly aggressive as well—a further widening of the rate differential could create interesting challenges, both for policymakers at the BOC and the loonie.

Election season is upon us—buckle up

In addition to monetary measures, looming elections in the U.S. and Canada promise to create interesting dynamics for fiscal, trade and regulatory policies in North America in 2025. While SEI does not recommend trading around election forecasts, it can still be worthwhile to think about how electoral decisions and resulting policy shifts could impact economies, financial markets, and portfolios in order to prepare oneself emotionally for the potential risks that lie ahead.

It’s been—and remains—a fascinating presidential race in the U.S., accompanied by interesting Congressional dynamics, and the outcome is far too close to call at this point. Based on polling and aggregated forecasts, the least likely outcome appears to be a Democratic sweep of the White House and Congress. While there may be a slightly higher probability of a Republican sweep, the most likely outcome at this point appears to be some sort of split between control of the White House and one or both houses of Congress (including the possibility that control of the House and the Senate flip from Republican and Democrat, respectively, to Democrat and Republican). We believe markets are likely to prefer a split-control outcome, as it would almost certainly take the most radical policy proposals of the winning presidential candidate off the table. For a more in-depth analysis of the U.S. election, see our Chief Market Strategist Jim Solloway’s latest Outlook, “A long autumn.”2

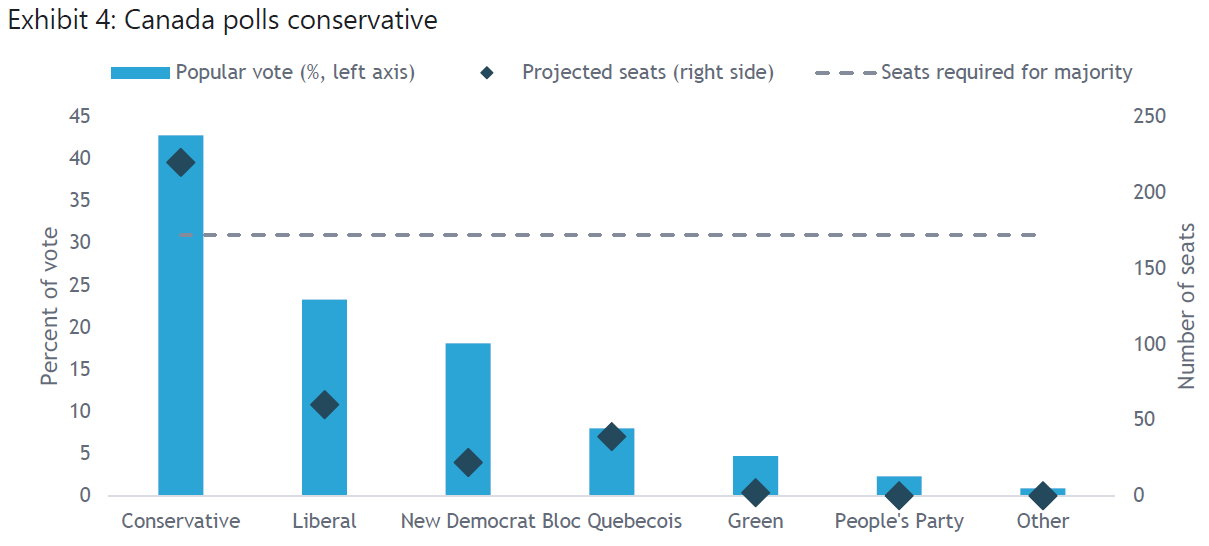

Closer to home, it looks fairly certain, based on recent polling results, as shown in Exhibit 4, that the Conservative Party is set to assume control between now and October 2025, depending on when elections are called or the current government dissolved. Whenever it happens, the election looks sure to usher in meaningful changes in regulatory and fiscal policies.

Source: CBC, SEI. National polling averages by party and projected seats in Parliament according to the CBC News Poll Tracker (https://newsinteractives.cbc.ca/elections/poll-tracker/canada/) as of 29 September 2024.

Given the U.S. election is likely to occur first, let’s take a closer look at potential implications associated with a sweep by either party there. One prominent Wall Street bank’s trading desk has created four baskets of securities—one group of long positions and one group of short positions for each party—expected to be impacted meaningfully by the presidential candidates’ policy proposals.3 On the Republican side, favourably impacted industries include banks and other financial services companies, along with energy and commodity producers, all of which should benefit from deregulation; domestic, non-residential construction-exposed firms and tariff beneficiaries are also featured on the long side. On the short side, consumer and industrial companies exposed to tariffs would be expected to underperform, along with renewable energy companies. The largest components of the Democratic basket reverse the positioning in energy and financials while adding a long position in infrastructure-related companies. The health care sector is split into long exposures to research & development spending, entitlement spending, and companies that should benefit from continuation of the Affordable Care Act4, with short positions in pharmaceutical companies given Democrats’ desires to expand recent Medicare drug-price negotiations.

For Canada, favourable movements in U.S. energy and financial regulations under Republicans could have positive effects, but those would likely be overwhelmed by a large, broad hike in U.S. tariffs given the importance of U.S.-bound exports to Canada’s economic performance. As a result, a Republican sweep could arguably be the riskiest election outcome for the Canadian economy and equity market. That said, it’s possible a Trump administration would prove willing to negotiate on trade (Trump’s existing U.S.-Mexico-Canada Agreement is already scheduled for renegotiation in 2026), and that might be even more feasible with a Conservative-led Canadian government.

A brief note on housing

Like many other advanced economies, home affordability remains a pressing issue in Canada. In a recent analysis5, Oxford Economics estimated that it will likely take another decade and over four million new homes to bring the housing market back into balance. However, they also expressed concern that the Canadian Mortgage and Housing Corporation’s (CMHC) plan6 to improve affordability by adding a further 3.5 million homes would likely run into severe capacity constraints in the near term (perhaps stoking inflation pressures) and eventually create an oversupply that could lead to a prolonged housing slump. This wouldn’t unfold over a short period of time, but it would mark a nearly 180-degree turn from the current situation. Of course, with an election looming in Canada and current polling indicating a significant shift in political control, housing policy seems likely to undergo some important changes.

Advice to investors

Perhaps you’ve heard someone utter the allegedly Chinese blessing/curse, “May you live in interesting times.” According to most internet sources, this is not a Chinese saying but something that was invented in the west in the 20th century.7 There are a couple of important lessons to take away from this. First, humans, being the often-anxious creatures we are, seem prone to believe they are living in especially interesting times, whenever that might be. Second, received wisdom is often worth a reexamination with sometimes surprising and bemusing results. However, at SEI we would argue that the received wisdom of portfolio diversification remains steadfastly true. No matter how interesting or anxiety-inducing the economic, political, geostrategic, and market environment may be. Investors will always be well served by diversifying the sources of risk in their portfolios.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

1 https://www.seic.com/en-ca/insights/third-quarter-sei-forward

2 https://www.seic.com/en-ca/insights/long-autumn

3 Goldman Sachs’ “Democratic Policy Pair” and “Republican Policy Pair” baskets include both long and short positions in various sectors and industries based on expectations of US sectors and industries that would be positively or negatively impacted by the respective candidates’ policy platforms.

4 https://housedocs.house.gov/energycommerce/ppacacon.pdf

5 Oxford Economics Research Briefing | Canada, “Housing market will take another decade to rebalance,” 30 July 2024.

6 Canadian Mortgage and Housing Corporation (2023), “Housing shortages in Canada: Updating how much housing we need by 2030,” available at: https://assets.cmhc-schl.gc.ca/sites/cmhc/professional/housing-markets-data-and-research/housing-research/research-reports/2023/housing-shortages-canada-updating-how-much-we-need-by-2030-en.pdf.

7 See, for example: https://en.wikipedia.org/wiki/May_you_live_in_interesting_times