U.S. Value Stocks: Neglected Opportunity

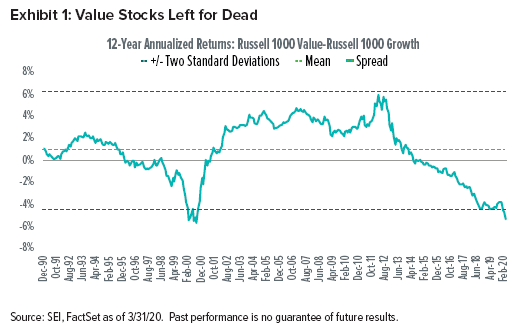

Value stocks, represented by the Russell 1000 Value Index, significantly outperformed growth stocks, represented by the Russell 1000 Growth Index, from the top of the tech bubble (March 2000) through the market top that preceded the global financial crisis (October 2007). This edge vanished during what has since largely been a decade-plus of outperformance by growth stocks. Historically low interest rates, muted inflation, moderate gross domestic product growth and the explosive revenues of technology, social media, and internet retail companies have propelled growth stocks, leading them to large gains relative to value stocks.

Value, on the other hand, has performed so poorly over the past dozen years (shown in Exhibit 1) that only about 5 percent of previous dozen-year periods have been worse (defined as a two-standard deviation event), according to our analysis. With only a few short-term wins since 2008 and staggering overall underperformance, many investors have lost faith in value.

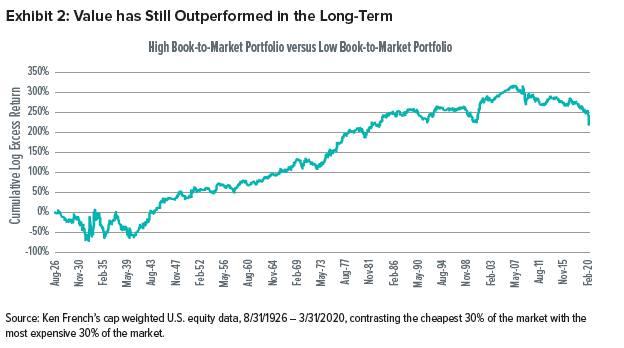

Yet, even with the past dozen years of significant underperformance, value still has outperformed over the long term as indicated by data from famed academic and author Ken French 1 (Exhibit 2)—which is why we maintain exposure to value stocks as part of our portfolio construction process.

Furthermore, we believe the current performance gap between growth and value represents what may be the most attractive investment environment for value stocks that we have seen in nearly 20 years. In our opinion, it is a question of when—not if—a value orientation will pay off.

Historically, value typically mean reverts (or outperforms) relative to growth after periods of prolonged underperformance. Accordingly, our domestic equity funds favor value managers—overweighting positions in value stocks in recognition of attractive earnings, cash flows, dividends and assets.

Why do Mean Reversions Happen—and What do They Look Like?

Benjamin Graham—widely considered the father of value investing—said that “in the short run, the market is a voting machine; but in the long run, it is a weighting machine.”

He argued that short-term popularity should not be confused with long-term value; that, eventually, a company’s intrinsic value will be reflected in the price of its shares. Mean reversion is the vehicle by which that value recognition occurs.

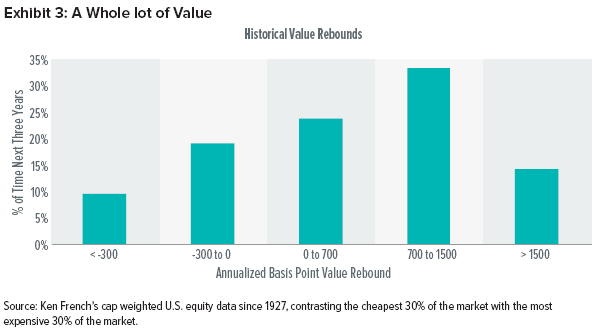

Ken French data show that prolonged periods (defined as rolling five-year time horizons) in which value underperforms have historically been followed by significant outperformance by value over the following three years. Although recent returns may imply otherwise, value has rebounded and outperformed in more than 70 percent of these scenarios since 1927.

It’s not just the frequency, but also the magnitude of the gains generated by these formerly unloved stocks. In about one-third of observations, value stocks outperformed by an average of 7 percent to 15 percent annually. In nearly 15 percent of instances, value’s outperformance exceeded an annualized 15 percent.

While the returns in Exhibit 3 appear quite attractive, they also came after periods of underperformance. The current environment is one of the longest and most significant periods of value’s underperformance on record.

Value’s Uncomfortable Truth

Most investors believe buying low and selling high is a strategy that will generate long-term gains. But purchasing stocks when they’re down tends to feel unnatural and uncomfortable. Holding cheap value stocks while growth-oriented technology stocks continue to soar also frustrates many investors. When it comes to value investing, however, patience really is a virtue.

Our portfolios are diversified across a number of factors, including value, momentum, stability, size and quality. While our value tilt has detracted over the past decade, history shows that the times when value is hardest to embrace have been the times when it has provided the biggest subsequent payoffs.

When Will it Happen?

Everyone wants to know when value will return to favour and which catalyst will cause the turn.

The short answer is that value trades are notoriously hard to time, and investors risk missing out on potentially impressive gains by being late to the trade.

That said, we think a number of potential catalysts could turn sentiment in favor of value, including:

- Rising interest rates (extremely low now)

- Higher commodity prices

- Increased inflation

- Faster economic growth

- Sector differentials (energy over healthcare has led to recent value outperformance; financials have also started beating technology)

- Technology stocks failing to meet investors’ lofty expectations

- Economy emerging from recession

This is not an all-encompassing list of potential catalysts. It’s also possible the catalyst that ultimately causes the turn toward value hasn’t even been identified yet.

Being early to the trade eliminates the need to guess the correct catalyst; investors must simply be patient enough to wait for the market to turn. We acknowledge this may be a challenging mental exercise, given value’s underperformance.

A Behavioural Bias

SEI is a pioneer in behavioural finance, and this field of study continues to influence our thinking today.

Consider recency bias. This describes an investor’s ability to remember items that appear at the end of a long list of complex data, rather than those that appear earlier.

Evaluating conditions in the financial markets often involves reviewing long lists of complex information. Most investors do not have systems in place to automatically capture important data points going back many years or decades. Even those who do may not place sufficient weight on older data points.

There are many examples of recency bias throughout the history of financial markets. The last prominent example took place in early 2000. After four years of a raging bull market in technology, media and telecommunications stocks lifted the market to new highs, investors—professional and amateur—believed that it was “different this time,” and that stocks that soared during the Tech Bubble would continue to rise unabated despite the experiences of past boom and bust cycles. As we know now, this was not the case, and the Tech Bubble deflated in a tragic spectacle.

Looking back even further, the Nifty Fifty saw a few dozen companies drive market gains in the 1960s and early 1970s. Yet these same companies lagged the market in the 1980s.

Every market environment is different, but the parallels with the current market are easy to spot. The FAANG stocks (Facebook, Amazon, Apple, Netflix and Google) look quite expensive. These firms, along with a handful of other high-flying tech stocks, have led the bulk of the gains in the S&P 500 Index in recent years. Meanwhile, unloved value stocks have once again been left behind. It’s worth noting that value stocks went on quite a run after the Tech Bubble burst. It’s easy to imagine a similar environment if market leadership shifts.

Investors can fight recency bias by remembering that long-term relationships usually hold up for good reason. For example, the relationship between the cash flow that a firm can deliver and the stock price it supports will not vary by large degrees for long periods of time. Eventually, history shows it will revert toward the mean. Investors need to ask whether it’s truly different this time. We don’t believe that is the case.

A Look into Our Portfolios

Stocks with very high Price-to-Earnings ratios are concentrated in the information technology, consumer discretionary and communications sectors, so it’s not a surprise that we are underweight those sectors in most portfolios. The consumer discretionary sector has a large variety of cheap stocks as well, but their weights tend to be much lower than the expensive stocks in the sector. Sectors that combine high quality with reasonable valuations include consumer staples and healthcare at this time, and we are overweight these sectors in most portfolios.

Our portfolio construction is not predicated on market timing. We believe trying to perfectly time trades to capture market inflection points is a futile exercise. Instead, we assess where it makes the most sense to invest the next incremental dollar, and make our decisions accordingly.

Why we Keep the Faith

We stand by our research indicating that value generates long-term outperformance relative to broad equity markets. Almost by definition, value companies are smaller from a capitalization perspective as their stock prices are trading at a discount (in terms of their fundamental valuations relative to broad equity markets). Investing in small and medium sized companies is also a hallmark of active management, and our managers certainly exhibit smaller-sized holdings than their benchmarks.

After assessing the current market environment, we remain firm in our belief—based on our research and empirical evidence—that, historically, value offers attractive long-term outcomes for patient investors. We intend to maintain our stance until a shift in sentiment lifts value—which, in our opinion, is inevitable.

Definitions

Price to Book Ratio: Stock’s capitalization divided by its book value, where book value is the value of an asset as it appears on a balance sheet, equal to cost minus accumulated depreciation. The value is the same whether the calculation is done for the whole company or on a per-share basis.

Price to Earnings Ratio: Equal to market capitalization divided by after-tax earnings. The higher the P/E ratio, the more the market is willing to pay for each dollar of annual earnings.

Standard Deviation: Statistical measure of historical volatility. A statistical measure of the distance a quantity is likely to lie from its average value. It is applied to the annual rate of return of an investment, to measure the investment’s volatility (risk). Standard deviation is synonymous with volatility, in that the greater the standard deviation the more volatile an investment’s return will be. A standard deviation of zero would mean an investment has a return rate that never varies.

Index Definitions

The Russell 1000 Index includes 1,000 of the largest U.S. equity securities based on market cap and current index membership; it is used to measure the activity of the U.S. large-cap equity market.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.