Allocating to Liquid Alternatives.

In the U.S. and U.K., SEI has been allocating to liquid alternatives for over a decade and a half. In recent years, liquid alternatives have become a more prevalent strategic allocation in many of SEI’s U.S. and U.K. multi-asset portfolios. SEI has now launched a Canadian Liquid Alternative Fund.

Risk and return drivers

The SEI Liquid Alternative Fund is the primary vehicle for exposure to liquid alternatives in our portfolios. The Fund is a systematic strategy that seeks to generate hedge fund-like returns using liquid securities1. The fund has two underlying components, a hedge fund replication strategy and a commodity trading advisor (CTA) replication strategy (aka or managed futures). Taken together, we expect the strategy to deliver roughly 0.4 equity beta over time, while reflecting both (1) the evolving risk factor exposure of a diversified pool of hedge funds and (2) diversification via its CTA strategy.

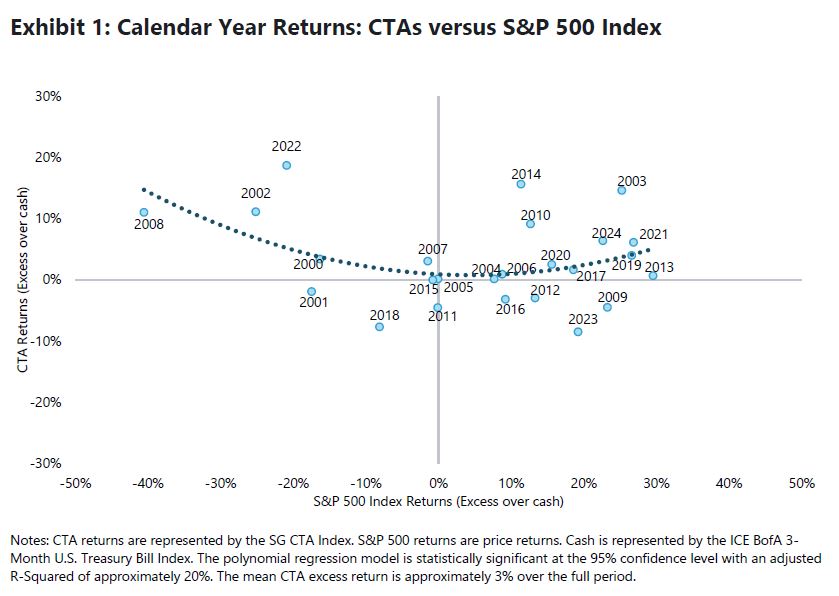

Investors can conceptualize CTAs as a momentum strategy that performs best in periods of sustained market trends. As illustrated in Exhibit 1, CTAs have historically performed best in extreme down and up S&P 500 markets. In “normal” market environments (think between the 25th and 75th percentile of outcomes), CTAs tend to earn no return over cash (and often below). Said differently, investors in CTAs accept returns at or below the risk-free rate much of the time for the opportunity to experience strong returns in extreme market environments. This curved relationship in returns between CTAs and the broad market is often referred to as “convexity.”

Over the long term we expect CTAs to earn a premium over cash. One explanation for this is that market participants tend to anchor to the recent past and underappreciate the persistence of a new economic trend.

There are two important risks to CTA strategies that may cause actual experience to deviate from the convex return profile we generally expect. First, CTA strategies are vulnerable to a sudden reversal in trend (i.e., an exogenous shock). Additionally, CTAs take positions in multiple asset classes, not just stocks. For instance, a CTA strategy may be long equities in an extreme S&P 500 up market, but may still have a negative return due to the strategy’s currency and/or rate exposure.

The role of liquid alternatives in portfolios

Compared to traditional long-only strategies, alternative investment strategies tend to maintain less directional exposure to equity and fixed-income markets, and this exposure can be highly dynamic. As a result, we generally expect the SEI Liquid Alternative Fund to exhibit significantly lower volatility than long-only equities. Given this lower volatility, liquid alternatives can serve a valuable role in a broader portfolio even if expected returns are lower than those of long-only equities, particularly if their correlation profile is favourable.

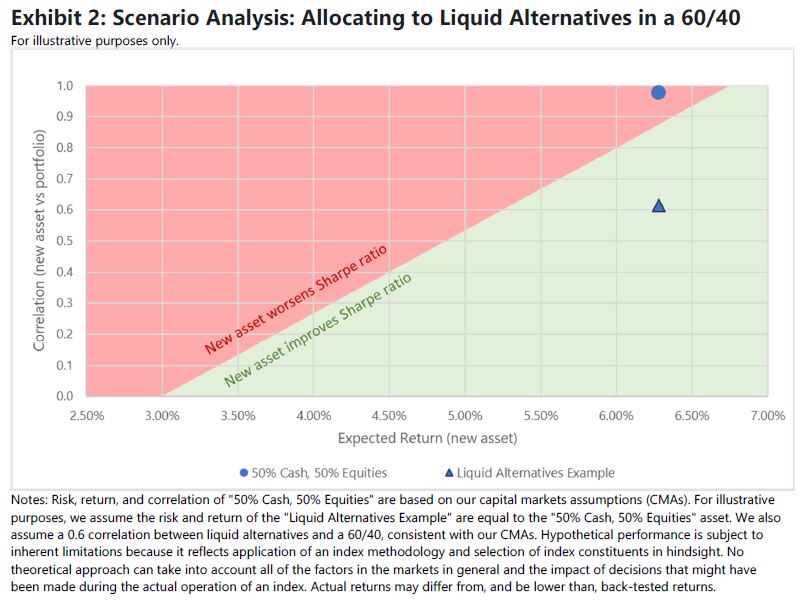

Consider an example where an investor currently owns a 60/40 stocks/bonds portfolio and is deciding whether to add an allocation to liquid alternatives that carry roughly 50% of the risk of the S&P 500. Exhibit 2 illustrates when it would be worthwhile from a mean-variance perspective (green) and when it would not (red) to add that asset, based on the given expected returns and correlations.

Note that if we were to simply add a strategy consisting of 50% stocks and 50% cash, the resulting portfolio would have a lower return at essentially the same level of risk as the initial 60/40. Therefore, adding this watered-down version of equity beta does not improve portfolio efficiency. However, if liquid alternatives can offer the same risk and return as this 50% stocks, 50% cash option but a more favourable correlation profile (e.g. correlation = 0.6), a 10% allocation can improve expected risk-adjusted returns.

How SEI allocates to liquid alternatives

The goal of asset allocation is generally to maximize return given a target risk level, based on the investor’s risk tolerance. Since investment performance is never guaranteed, we must consider the entire range of probable outcomes. For instance, in the previous exhibit, the blue triangle represents an expectation for the liquid alternative fund on average. But any forward-looking estimates—and particularly those for a strategy as dynamic as our liquid alternative strategy—are inevitably subject to uncertainty. For this reason, we believe investors should size liquid alternatives allocations appropriately such that traditional sources of risk premia, like stocks and bonds, generate most of the portfolio’s risk2. We typically fund liquid alternatives from a roughly risk-equivalent combination of equities and fixed income.

For a 100% equities portfolio, we are unable to add liquid alternatives because it would cause the portfolio to become under-risked. A portfolio with 80/20-like risk is still dominated by equities—in an 80/20, we expect equities to contribute 97% of the risk over the long-run, based on our capital market assumptions. We believe asset classes with duration exposure, such as core fixed income, remain the best diversifiers when portfolios are dominated by equity risk, given their correlation profile.

In middle- and lower-risk portfolios, where risk is less dominated by equities, we find that liquid alternatives can play a larger role. We believe that adding modest exposure to liquid alternatives in these portfolios can improve diversification and return efficiency. Our allocations to liquid alternatives typically peak in more risk-balanced portfolios (e.g., a 40/60). In the lowest risk profiles, we also find a role for liquid alternatives. However, when risk budget allows, we tend to prioritize exposure to equity risk, often paired with short duration to manage the overall level of portfolio volatility. This enhances exposure to economic growth risk in an asset allocation where it is in short supply.

The decision to add a liquid alternative investment to a diversified multi-asset portfolio is not a question of whether or not it will outperform stocks, but whether expected return efficiency and diversification benefits will improve risk-adjusted returns.

For the SEI Liquid Alternative Fund, we expect risk roughly similar to 50% of equities and returns between investment-grade fixed income and equities. The strategy’s differentiation to 50% equities/50% cash comes from both the factor tilts related to its hedge fund replication component and its CTA component. For the CTA component, we generally expect a convex return profile wherein the strategy experiences muted returns in normal market environments and its best returns in extreme up and down equities markets. Investors should be aware of risks that could cause the strategy to deviate from this expected return profile—for instance, if an exogenous shock causes a sharp reversal in trend. Taken altogether, we view liquid alternatives as a valuable complement to traditional long-only strategies, offering the potential to increase portfolios’ overall risk-adjusted returns.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affiliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and the information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from qualified professionals. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.