Big moves and prowling bears. What should you do?

It’s a big year for big moves.

You’re not imagining things if you think equity markets have felt more volatile than usual in the year to date. Expensive growth-oriented U.S. shares are already well into a bear market, after all, along with emerging-market equities. Bonds prices have also been tumbling this year.

Canadian shares haven’t been spared from the tumult: performance for April and May is set to deliver the largest back-to-back monthly declines since the COVID crash. Before that, we’d need to look back to the energy-market-centric five straight months of losses in 2015 to approximate the April-to-May 2022 decline.

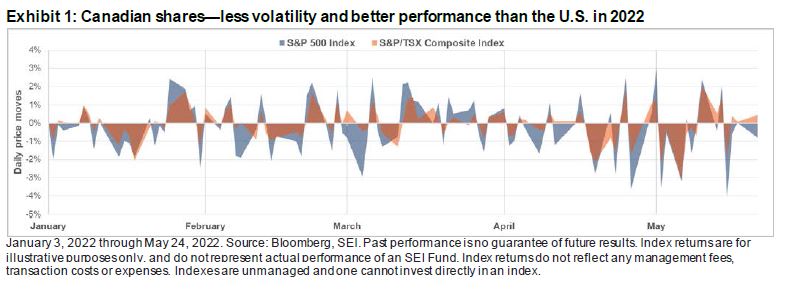

Still, there’s a wide distinction between the volatility in U.S. equities and that of domestic shares. Exhibit 1 plots the daily percent change in each market for the year to date.

The blue-shaded areas for U.S. equities generally have a much wider range than the orange-shaded areas for domestic shares. Conditions have been tamer at home than abroad.

Tamer tape = tinier tumble.

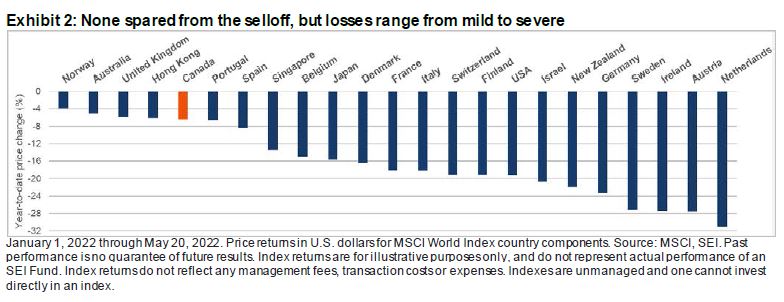

All the cheer in the world won’t distract from the fact that Canadian shares are, in fact, down for 2022. But they’ve fallen by considerably less than the lion’s share of other markets. Exhibit 2 on the next page highlights equity performance in the year to date across developed markets.

Canadian shares are thankfully the fifth best performer in 2022. Domestic equities are down by roughly a third of the loss in U.S. shares. Sometimes exposure to the U.S. and emerging markets can drive outsized gains versus the Canada, and sometimes it can introduce more volatility and deeper losses.

Investor hands are not tied, but they should sit on them.

The unpredictable nature of performance across different markets is what makes diversification such a powerful tool. Over the long term, a globally diversified investment portfolio harnesses the risk reduction and return enhancement potential that owning a wide variety of assets with varying correlations can provide.

No one can credibly answer when or where this selloff will conclude, but investors should take a great deal of encouragement from the simple fact that recoveries have been much more potent than downturns through history.

While you have no control over the depth of the decline, you do have the last word on how much of a downturn you’re willing to tolerate. We recognize that the market environment has been inhospitable in 2022. The simultaneous selloff in bonds has added an uncommon challenge into the mix.

As losses grow, it can be tempting to consider a temporary exit in favour of cash. But when would be the right time to re-invest? And while cash is always susceptible to inflationary erosion, price increases are currently running at multi-decade highs.

We urge investors to consider the wisdom of shouldering a significant downturn and then exiting. Bearing the pain of the decline is an investment in the eventual recovery, which history suggests will eclipse the selloff. Exiting for cash is akin to relinquishing this investment.

Our view.

There’s no denying that headwinds persist on the path to recovery. Inflation is raging—and central banks may be underestimating what it will take to bring it back to earth. The war in Ukraine is exacerbating the commodity shortage—most notably in fuel and food inputs. COVID-19 continues to snarl global supply chains.

As active investment managers and asset allocators we view these types of environments in terms of the opportunities they offer. A globally diversified investment portfolio will not have endured the full brunt of the selloff in U.S. or emerging-market stocks.

Opportunities are beginning to abound. High-priced U.S. shares started selling off earlier than the broad market and have fallen by much more. This means they’re moving back toward valuation levels that are more in line with the rest of the market. Value-oriented equities still look attractive, and we expect to see bargains in equities if the market falls a bit further.

We remain nimble in fixed income, as always, adding credit or duration exposure as spreads widen and removing risk once spreads tighten. Higher volatility creates more opportunities to manage these exposures.

Less-efficient areas like emerging markets offer significant opportunities for active managers. Emerging-market equities have been in a bear market for several months. The diverse opportunity set in emerging markets tends to reveal itself during downturns, providing the opportunity to identify attractive risk-and-return tradeoffs.

Glossary of financial terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Duration: Duration is a measure of the sensitivity of the price of a bond or other debt instrument to a change in interest rates. The longer the duration, the more sensitive the bond will be to changes in interest rates.

Growth: Growth-oriented shares exhibit earnings growth above that of the broader market.

Value: Value-oriented shares are those that are considered to be cheap and are trading for less than they are worth.

Index definitions

The MSCI World Index is a free float-adjusted market-capitalization-weighted index that is designed to measure the equity market performance of developed markets.

The S&P 500 Index is a market-capitalization-weighted index that consists of 500 publicly-traded large U.S. companies that are considered representative of the broad U.S. stock market.

The S&P/TSX Composite Index is a capitalization-weighted index designed to measure market activity of stocks listed on the Toronto Stock Exchange (TSX), including about 250 companies which represent roughly 70% of the total TSX market capitalization.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.