Bonds: Opportunity amid stubborn inflation and rising rates.

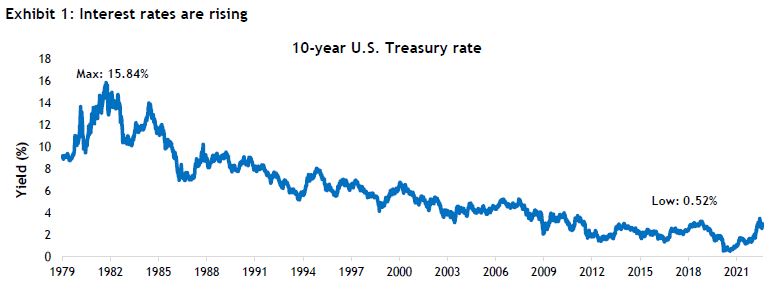

Bonds were on a winning streak from the end of 1981 through to the summer 20201, with prices rising as yields fell. Today, the dynamic is changing as fixed-income markets witness the end of a 40-year bull market in bonds.

This regime change is a double-edged sword. Rising bond yields are accompanied by falling prices, as bond prices and yields have an inverse relationship. Investors buying bonds today will get paid a higher rate of interest than they would have in the recent past. Investors holding bonds today are seeing the value of their holdings decline.

What happens next?

Will inflation push bond yields even higher or will recession concerns overwhelm the market?

We believe inflation will remain elevated and stubborn as the components of inflation have broadened across the U.S. economy. As of August 2022, around 70% of the items in the U.S. Consumer Price Index (CPI) basket were running at above a 4% year-over-year increase. Despite some recent relief at the gas station, the CPI was running at an 8.3% year-over-year pace in August. The Core Personal Consumption Expenditures Price Index (which excludes energy and food), is the Federal Reserve’s (Fed) preferred measure of inflation and was running at 4.6% year-over-year in July, well above the Fed’s 2.0% inflation target. Therefore, we expect inflation to remain the Fed’s primary focus (overshadowing job growth) as the U.S. central bank raises the federal funds rate to curb inflationary pressures.

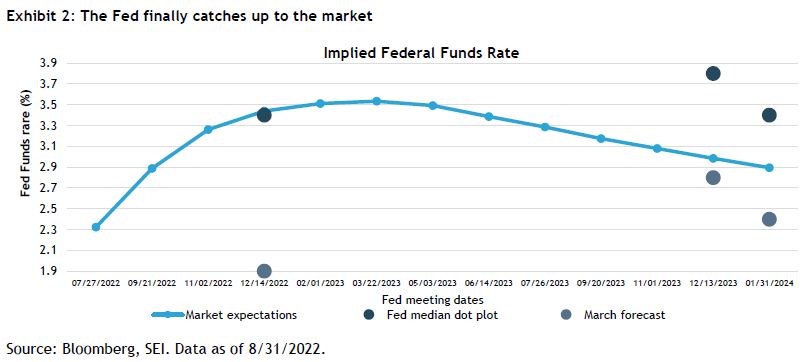

Fed Chairman Jerome Powell recently hinted that the long-term neutral interest rate (the level at which monetary policy neither supports nor restricts economic activity) is near the current federal funds rate of 2.25%-2.50%. This noted, Powell has since stated “in current circumstances, with inflation running far above 2% and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.” In June, the Fed’s dot plot (which projects the future state of the federal funds rate) median was adjusted higher to show (Exhibit 2) that Federal Open Market Committee (FOMC) members expect the federal funds rate to end 2022 at 3.40%, up from the 1.90% forecast in March. The shift higher in the median dot plot moved the projections closer in line with market’s expectations at the time and clearly projects the expectation for further rate hikes over the final months of this year.

We also believe broader inflationary pressures will persist over the near-term, leading to additional rate hikes. This, in turn, may cause U.S. Treasury yields to drift higher. We do not expect them to rise at the pace we’ve observed over the past 24 months (during which time the 10-year U.S. Treasury yield increased by more than 2%), as the market grapples with the fact that a soft landing scenario in which the Fed tames inflation without doing significant damage to the economy is now less likely.

Second quarter U.S. gross domestic product (GDP) data signaled that the U.S. is headed towards a recession. This news will continue to get airplay if economic conditions soften further. While two consecutive quarters of economic decline is typically used to define a technical recession, the current downturn is accompanied by exceptionally low unemployment—something not typically seen in textbook definitions of recession. The National Bureau of Economic Research (NBER), the body that maintains a chronology of U.S. business cycles and that opines on whether the U.S. has entered a recession, has yet to declare a formal decline. The NBER defines a recession as “a significant decline in economic activity that is spread across the economy and lasts more than a few months.”

While the U.S. is seeing a healthy job market (with unemployment below 4%), inflation is biting for U.S. consumers, with the average U.S. household spending $460 more each month to buy the same basket of goods and services as last year2. When consumers see higher prices for groceries and gasoline accompanied by lower (real) wages and lower balances in their retirement savings, the wealth destruction is tangible. As U.S. consumers get back from their summer vacations, the impact of inflation and the murkier economic backdrop may lead to a tightening of the belt. All while the Fed continues to increase the cost of borrowing, which has started to pressure the recently ‘hot’ U.S. housing market. The U.S. 30-year fixed-rate mortgage average has increased by around 3% in the past 12 months.

While investment managers generally don’t believe a deep U.S. recession is imminent, they are weighting the increased likelihood of a recession in the coming year. This has resulted in a more conservative stance.

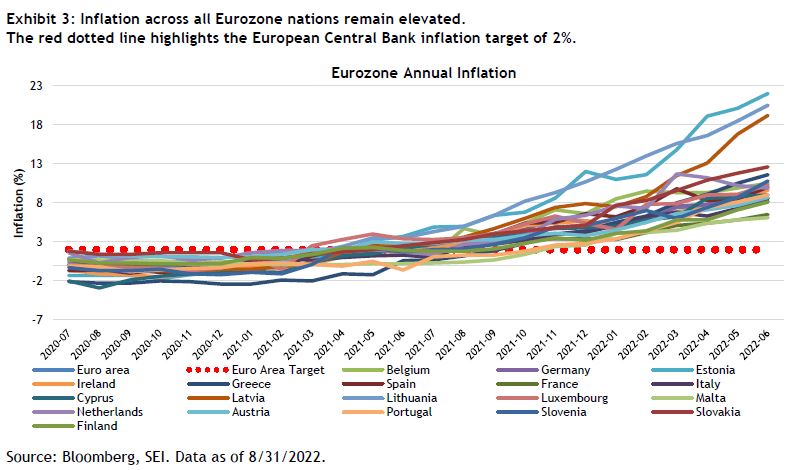

Outside of the U.S., the risk of a serious recession and stagflation (high inflation/low growth) is even greater. As a result of the Russia/Ukraine conflict, the Nordstream pipeline (a key artery feeding natural gas to Germany) is shuttered as Russia and the West engage in economic warfare. The Bundesbank (Germany’s central bank) warned that if Russian energy supplies stop their economy may shrink by more than 3%, taking a toll on Europe’s most powerful manufacturing in 2023. Europe at large could potentially see a notable GDP decline. The additional burdens of supply chain challenges, food shortages, geopolitical tensions, and inflation at 8.9% year over year as of July, put the possibility of recession in Europe much greater than in the U.S.

The Bank of England (BoE) also has a headache, as the British economy is displaying similar fragilities to Europe. The BoE expects inflation to hit as high as 13%. Other experts believe it could increase to closer to 20% as the U.K. lifts its energy price cap in October, therefore energy inflation can be expected to increase from where it is today. The UK also faces challenged consumers and slowing economic growth. Although wages are rising in nominal terms, real wages have dropped the most in 20 years and like the U.S. consumer, the U.K. public is feeling inflation in their wallets.

Investment implications

Over the course of the second quarter, and notably in June, elevated recession fears led to a widening of credit spreads as investors demanded higher compensation for the increased likelihood of economic deceleration. Despite the spread move, we remain cautious as the market continues to price in slowing economic data and pressures central banks to keep raising interest rates to fight inflation. Fed Chair Powell ‘forcefully’ reinforced our view during his Jackson Hole speech in which he underscored the Fed’s focus on reducing inflation.

In this environment, our managers are incrementally adding risk within their portfolios, although they remain cautious with the view that a more attractive entry point will arise in the near-term. Manager are closely watching spread levels, along with economic and corporate fundamentals and the technical backdrop. They are taking advantage of buying opportunities in banks with healthy balance sheets, while also targeting shorter-maturity financials (meaning less time until principal is repaid).

Also, something that may not be as easy to see at the 10,000 foot level, managers are making a number of relative value trades—selling currently held bonds and replacing them with bonds they believe to be offering a more attractive relative value (better future returns). While at the top level, you might not see a lot of changes in terms of sectors or countries, there are changes occurring in the engine room as rising interest rates and market volatility presents opportunities for active management.

Our positions

In this environment, broadly speaking, SEI’s fixed-income portfolios are positioned with:

- A modest overweight to the spread sectors, which is providing a yield advantage to the funds. This noted, we remain cautious and very selective on where we hold risk, generally favoring frontend corporates and securitized debt.

- Neutral duration in short-to-limited term U.S. strategies (which has increased from an underweight as Treasury yields pushed higher). Within our U.S. Core portfolios, we continue to hold a marginal overweight to duration, with tactical adjustments applied as interest rates exhibit short-term fluctuations.

- We generally remain underweight European and UK duration within our global and international fixed income portfolios, with a tilt to the emerging markets.

- In the high-yield space, we have off-benchmark exposure to loans and collateralized loan obligations (USA ONLY), along with an underweight to BB-rated debt, which reduces the portfolio’s interest rate sensitivity. We have a modest overweight to B-rated and CCC-rated exposure. From a sector perspective we are overweight the media, technology and basic industries sectors, with leisure, services and capital goods notable underweights.

- The emerging market debt portfolio continues to favor the high-yield space, which is currently offering attractive value. This said, managers remain selective on the countries they are holding within this segment of the market. They continue to focus on opportunities in local-market interest rates while remaining cautious on foreign exchange markets.

What we’re watching: Central banks and economics

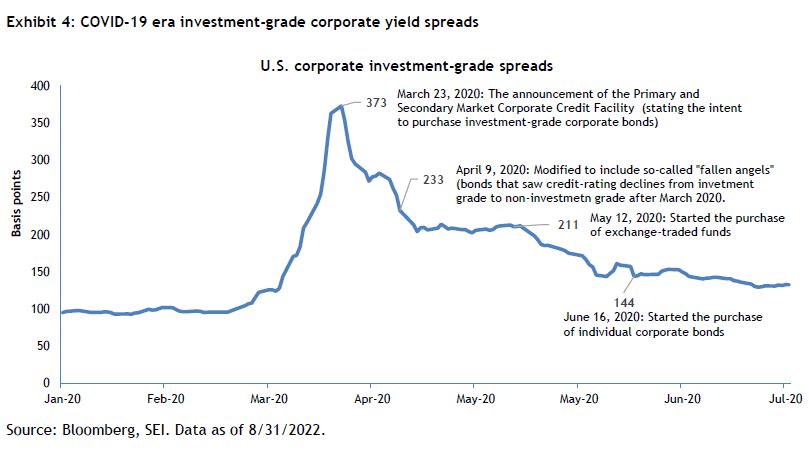

When evaluating the state of the market, we believe central bank intervention is a consideration that must be taken into account. Looking at historic periods, the U.S. Federal Reserve stepped in with lower interest rates and flooded the market with liquidity during times of economic stress. As a result of that intervention, the spread of investment-grade corporate debt decreased dramatically, as most recently observed during the pandemic period.

That’s not where we stand today. The Federal Reserve is trying to tame inflation, so we don't expect to see the same ferocious intervention seen in past episodes. Therefore, it may take longer for credit spreads to revert and push bond prices higher. (Bond prices and yields move in opposite directions.)

While we expect broader corporate default rates to pick up from their current extremely low levels as the economy slows, we are not currently expecting a 2008-2009 type of environment. To date, corporate fundamentals remain generally healthy and well positioned to weather any near-term slowdown.

It’s the macroeconomic piece of the puzzle that is getting a little bit cloudier. We continue to watch the health of the U.S. consumer, along with the U.S. job market (which has remained strong despite mixed signals in other parts of the economy). We also remain focused on the Fed and the indicators the Fed is watching, including the tightening of financial conditions, the level and trajectory of recorded inflation and expectations and employment indicators to name a few.

During periods of market stress, selecting managers that can avoid credit concerns is paramount to success and remains a key focus of SEI’s fixed-income investment efforts. We believe volatility will remain elevated over the near-term, which is generally a fertile hunting ground for skilled active managers.

Glossary of financial terms:

Collateralized loan obligations (CLO): A collateralized loan obligation (CLO) is a single security backed by a pool of debt. The process of pooling assets into a marketable security is called securitization. Collateralized loan obligations (CLO) are often backed by corporate loans with low credit ratings or loans taken out by private equity firms to conduct leveraged buyouts. A collateralized loan obligation is similar to a collateralized mortgage obligation (CMO), except that the underlying debt is of a different type and character—a company loan instead of a mortgage.

Federal funds rate: The federal funds rate is the interest rate at which depository institutions lend reserve balances to other depository institutions overnight on an uncollateralized basis.

Gross domestic product (GDP): Gross domestic product is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country’s economic health.

Index definitions:

U.S. Consumer Price Index: The Consumer Price Index (CPI) measures the monthly change in prices paid by U.S. consumers. The Bureau of Labor Statistics (BLS) calculates the CPI as a weighted average of prices for a basket of goods and services representative of aggregate U.S. consumer spending.

Core Personal Consumption Expenditures Price Index (PCE): The Core Personal Consumption Expenditure Price Index measures the changes in the price of goods and services purchased by consumers for the purpose of consumption, excluding food and energy. Prices are weighted according to total expenditure per item.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.