Brexit’s in the Bag: Now What?

At the end of January, the U.K. officially left the EU, giving way to an 11-month transition period during which the UK and EU will negotiate the terms of their future relationship. Although nothing between them changed economically on February 1, 2020, the day after the official divorce, everything conceivably can change on January 1, 2021, when the transition period is set to expire.

Gross domestic product (GDP) in the EU grew by just 1.1% in the fourth quarter of 2019 compared to a year ago, the area’s weakest figure in six years. That performance lags economic growth in the U.S. (2.3%), Japan (1.7%) and Canada (1.7%); Germany (0.5%) and Italy (0.0%) fared even worse over this period.

While other global economies have also decelerated, three-plus years of Brexit uncertainty has had the impact of depressing investment and increasing economic volatility in the area. Questions surrounding the eventual terms of trade have forced some businesses to hold off adding employees or expanding.

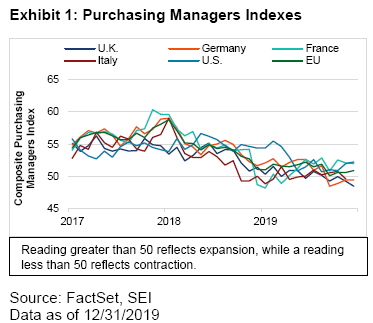

Other data—such as the purchasing managers’ composite indexes, including manufacturing and services—also suggest a deterioration in EU economic activity over the last two years.

Government policy is geared toward encouraging growth in Europe, although there is constant debate regarding the efficacy of negative interest rates. It remains to be seen in what direction newly appointed European Central Bank (ECB) President Christine Lagarde takes the central bank.

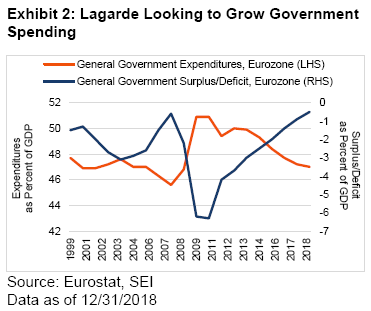

Exhibit 2 shows the trend in eurozone general government expenditures and its annual deficit/surplus as a percentage of area-wide GDP since 1999. Despite the euro area’s slow economic growth, government spending as a percent of GDP amounted to 47% in 2018, down from a 2010 peak of 51%. The eurozone-wide aggregate deficit, meanwhile, contracted from a hefty 6.3% to just 0.5% over the same period. If Lagarde’s call for government spending is supported, perhaps there’s hope that fiscal policy will shift from a steady headwind to a tailwind for eurozone growth.

Our Outlook

We remain optimistic that European growth will begin to recover from the lows of 2019 and expect a respectable reacceleration in growth among the more industrialised emerging markets. This should benefit Europe, particularly Germany. Just a few months ago, a disorderly Brexit seemed a possibility. That threat seems to have passed. Apart from Brexit, the lessening of trade tensions and improvement in China’s economic growth should also provide export-dependent Europe with a moderate boost in 2020.

We expect rationality to prevail, but a no-deal Brexit remains a residual risk. As the transition deadline nears at the end of 2020, European markets could experience renewed volatility if the negotiations appear to be foundering on irreconcilable differences. In the near-term, equity investors may still react positively as signs of improved global economic growth accumulate.

Important Information

SEI Investments Canada Company, a wholly-owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affiliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations.