Capital Market Assumptions Update: Lower Returns Expected

At SEI, we recently updated our capital market assumptions (CMAs) as part of our review and monitoring process. This brought our estimates for risk premiums over cash in line with our current expectations for capital markets (cash is used as a proxy for the theoretical return on a risk-free asset).

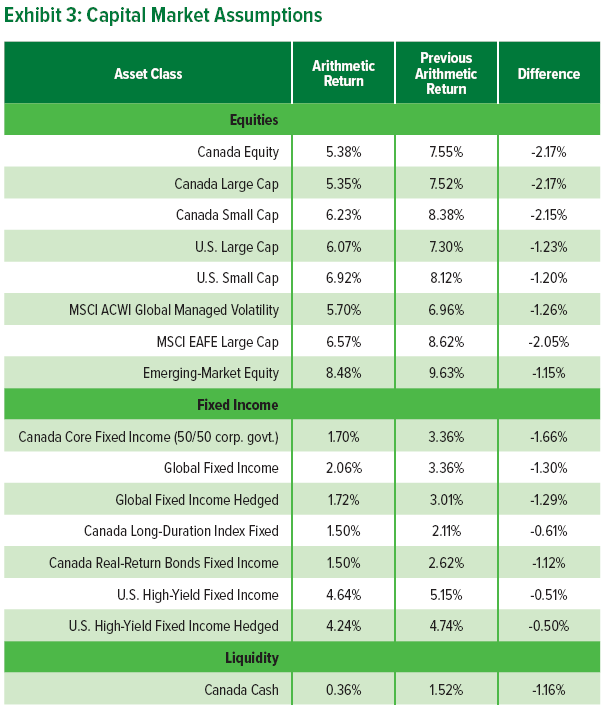

Fixed-income return expectations lowered

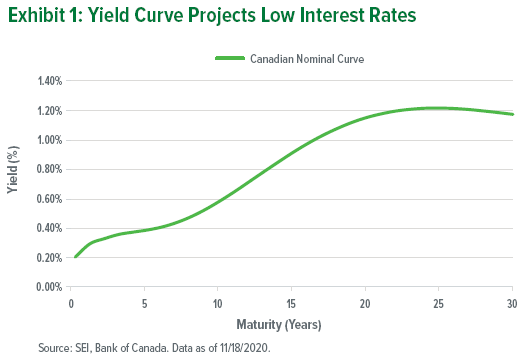

Central banks around the world have reacted swiftly and significantly in their efforts to prop up the global economy in light of the COVID-19 pandemic. The Bank of Canada (BOC) has indicated its willingness to keep interest rates low throughout the recovery, which leads us to believe that short-term rates will be anchored for some time. We also view longer-term rates as unlikely to move notably higher as the global bond market has shown no sign that inflation is expected to run wild.

With low interest rates rising only gradually back to more normal levels, we expect fixed-income returns to be subdued for some time. Given roll-down return assumptions (falling yields and rising prices as a bond’s maturity date approaches) and lower expected returns on cash, we do not see an improvement in risk/return ratios for bonds relative to equities. Accordingly, despite the low level of expected returns on bonds, this does not change our view that fixed-income investments have a role to play in investors’ portfolios.

Global equity return expectations lowered

Based on current global central bank policies implemented in light of the COVID-19 pandemic and recent BOC projections of zero or near-zero overnight lending rates, our base-case view is a slow return of interest rates to more typical levels. Equity asset classes are still expected to deliver similar levels of risk premiums as they have historically; however, we anticipate lower absolute returns given the lower interest-rate environment.

About SEI’s capital market assumptions

At SEI, we develop forward-looking, long-term capital market assumptions about risk, returns and correlations for a variety of global asset classes, interest rates and inflation. Our assumptions are based on quantitative analyses of historical data and current market environments along with qualitative reasoning. We believe this approach allows for greater impartiality than methods that rely on historical data alone, which are often skewed by a single time period or event.

We aggregate our asset-class assumptions into a diversified portfolio, and then run Monte-Carlo simulations to develop scenarios across a wide variety of market environments that can provide insight into the potential impact of future market variability over time.

In our view, the value of these assumptions is ultimately not in their accuracy as point estimates, but in their ability to capture relevant relationships and changes in those relationships as a function of economic and market influences—and in our ability to help investors make well-informed decisions.

Please refer to our recent publication, Developing Capital Market Assumptions, for more detail about how we develop CMAs at SEI. Information regarding the actual assumptions that we use in a specific portfolio can be requested from your SEI representative.

CMAs are not predictions of how asset classes will perform or reliable indicators of future performance; instead, they are expected long-term characteristics of asset classes. The below figures are SEI’s mean estimates for select asset classes. They do not represent all asset classes SEI analyses nor should they be considered projections for any SEI investment products. Different tools and models can simulate various market conditions using these assumptions as inputs. CMAs are used in the strategic asset allocation process, for asset/liability studies, and in proposal-generation systems. All assumptions are pre-tax and gross of any fees or expenses related to investing.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is for educational purposes and should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds. There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There are other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information contained herein that is based on external sources is believed to be reliable, but is not guaranteed by SEI, may be incomplete or may change without notice. SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.