Commodities set to keep inflation hot

It’s no secret that inflation has been running hot. Central banks around the globe began hiking interest rates in an effort to bring it down. Even though most measures have shown that inflation is cooling, SEI believes expectations for future inflation may still be too low.

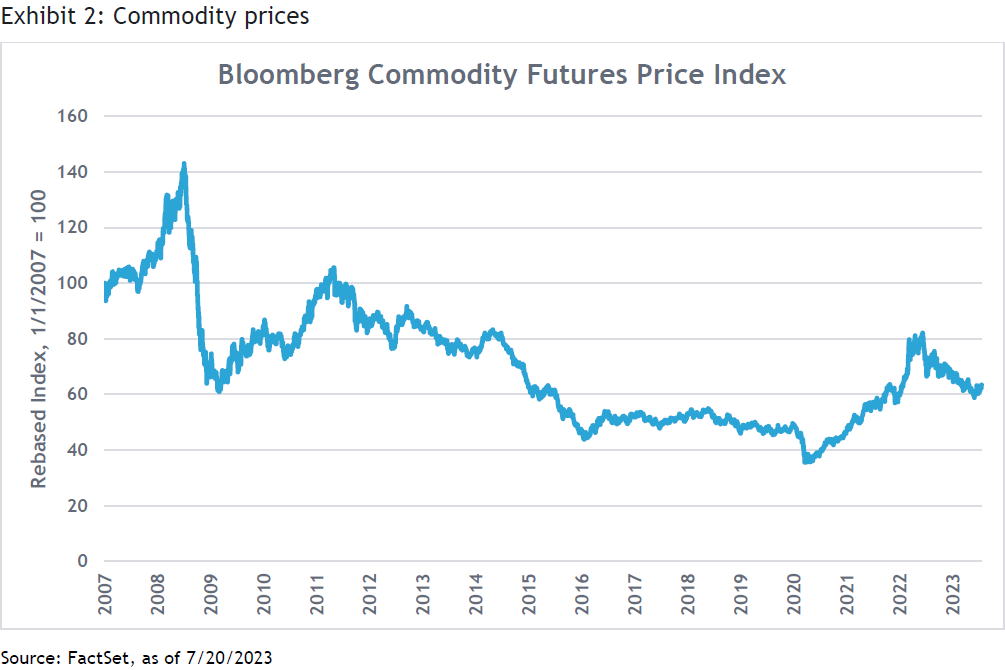

Simply put, much of the recently lower inflation can be attributed to falling commodity prices. In our view, the trend in commodities seems ready to reverse higher, and higher commodity prices feed into costs and can contribute to inflation staying higher for longer.

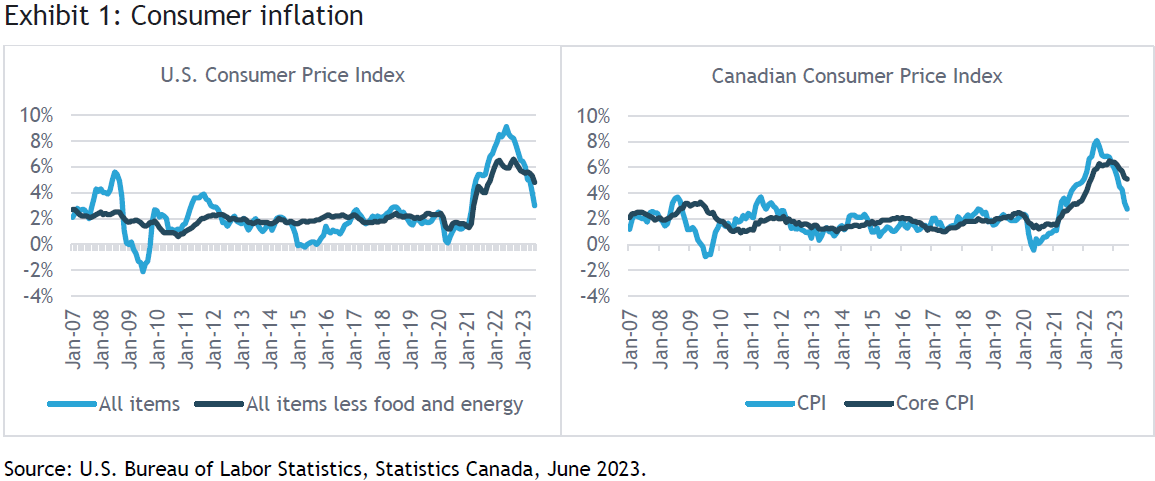

Consumer prices jumped in 2008 ahead of the Great Financial Crisis (GFC), and then swung lower as the crisis took hold. Inflation trends reverted following the GFC and consumers enjoyed a relatively stable decade of modest inflation until COVID-19 shook the world. Following a brief but sharp decline, inflation as measured by the U.S. Consumer Price Index (CPI) soared to over 9% for the year ended June 2022. Inflation has notably cooled since then, and much of that can be attributed to falling energy prices. As shown in Exhibit 1, inflation for the all items CPI—which includes more volatile food and energy costs—is significantly less than the all items less food and energy CPI. The story for Canada is strikingly similar.

Looking at the trends in CPI, investors may believe that the inflation fight is nearing its end. Indeed many investors expect central banks to end their rate hiking cycles over the next few months or quarters, and then even cut rates at some point next year. As much as we would enjoy inflation receding to around 2%, we do not share that same optimistic view and see numerous reasons why inflation will potentially be higher for longer.

Lack of investment

Commodity prices suffered a precipitous drop from their highs following the GFC and then spent roughly another decade in a downward trend. This discouraged investment in more traditional mining, exploration, and refineries. In the early 2010s, hydraulic fracturing—commonly called fracking—brought significant additional crude oil supplies to market and hampered oil prices. At the start of the fracking boom most frackers pumped as much oil as they could in an effort to gain market share, however this was short lived. Starting around 2015, frackers have shown significantly more discipline in their operations and have generally chosen to prioritize the return of cash to investors in the form or dividends and stock buybacks. The decline in capital investment in energy and metals has led to a reduction in capacity—a situation exacerbated by the disruptions caused by COVID-19.

Transition away from fossil fuels

Longer term, the transition away from fossil fuels should continue to put some downward pressure on oil prices, but the effects of this transition will not be felt evenly across the commodity complex. For example, part of the transition is greater adoption of electric vehicles (EVs). As demand for EVs surges, so does demand for metals—copper, lithium, manganese, and cobalt for example—that are required for battery production, but supply may well be constrained by the lack of investment. It can take a decade plus to bring a copper mine on-line from the time a deposit is discovered. Further, environmental obstacles can add additional years to the developmental timeline. Overall, we believe this points to higher commodity prices.

Business environment

Energy producers, meanwhile, face an increasingly unfriendly business environment as governments seek to accelerate the transition away from fossil fuels. Higher-cost producers have no incentive to explore for new oil and gas deposits or build pipelines and refineries if they are not guaranteed a source of adequate demand for the next 20 or 30 years. This could lead to periodic price spikes, as we saw in 2022, in the event of a supply disruption whether it be a war, a major fire at a refinery or just a bad hurricane in the Gulf.

Geopolitics

Geopolitics are seemingly constantly in play when pricing commodities. Historically, turmoil in the Middle East always roiled oil markets, but today the geopolitical concerns are even greater as globalization has not only increased demand for commodities, but inserted many more choke points in the supply chain. China has threatened to cut off exports of rare-earth metals to the U.S. and other countries. Indonesia has banned the export of raw nickel since December 2020, requiring foreign buyers to set up smelters within the country. Peruvian copper mines are subject to attacks by indigenous protestors. Of course these are all additional concerns to ongoing war in Ukraine.

Climate changes

It’s not just energy and metals either. Even agricultural commodities face the possibility of more structural disruption owing to climate change with the increased frequency of droughts and high temperatures in major growing areas like the U.S. Midwest. Note that an El Nino weather pattern is developing in off the coast of Latin America which has historically led to generally higher global temperatures. Depending upon its severity it could have a major impact on Argentinian wheat along with Brazilian soybeans and coffee production. In the meantime, Ukraine again faces a blockade of its wheat exports owing to the war.

Our view

We have a high degree of conviction in our view for rising commodity prices and find this view incongruent with the seemingly broadly held view by investors that inflation will quickly return to its benign pre-COVID-19 levels. The bottom line is, higher commodity prices feed into costs and contribute to inflation staying higher for longer.

Index definitions

The Bloomberg Commodity Total Return Index comprises futures contracts and tracks the performance of a fully collateralized investment in the index. This combines the returns of the index with the returns on cash collateral invested in 13-week (three-month) U.S. Treasury bills.

Consumer-price indexes measure changes in the price level of a weighted-average market basket of consumer goods and services purchased by households. A consumer price index is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected periodically.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock. All data as of 6/30/2023 and in U.S. dollar terms unless otherwise noted.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.