Correlation anxiety and the reality of diversification

In recent months, the correlation between stocks and bonds has been a controversial topic in the financial press. A rise in the degree to which they move in tandem has pundits questioning the future of traditional 60/40 stock/bond strategies1 and, in some extreme cases, the asset classes’ diversification profile2 altogether. We consider these concerns overwrought—and the math is on our side.

Diversification math

There is a common misconception that traditional stock/bond strategies rely on a negative correlation (in which one tends to rise in value when the other falls) for their diversification benefit. In reality, the benefits of diversification are not so fragile. While a lower correlation between stocks and bonds reduces a stock/bond portfolio’s expected volatility, all else equal, that relationship holds across all levels of correlation. As long as the asset classes do not exhibit perfect positive correlation (as represented by a correlation coefficient of +1), owning exposure to both will inherently yield diversification benefits. Positive correlation does not negate the benefits of diversification; meaningful benefits exist even when correlation is consistently above zero.

Fundamental portfolio mathematics helps to explain this dynamic. In a multi-asset portfolio, expected returns are a linear function of expected asset class returns; the portfolio’s expected return is a simple weighted average of that of its components. In contrast, portfolio risk (e.g., expected standard deviation) does not follow that linear relationship. As long as the correlation between asset classes is less than perfect, the portfolio’s expected risk will be lower than that of the weighted average of its components. This math, and the associated benefits for portfolio construction, holds true whether correlations are positive or negative.

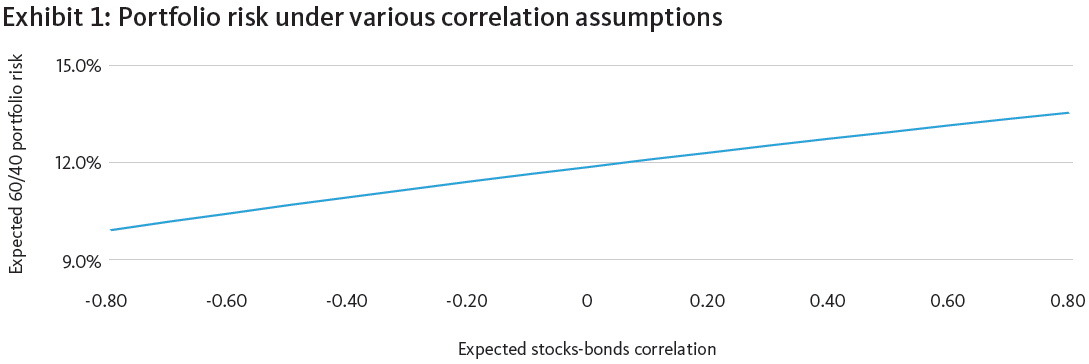

Correlation and 60/40 risk Focusing specifically on a 60/40 portfolio, the numbers demonstrate that most investors need not be overly concerned with a rise in correlation between stocks and bonds. The simple reason is that correlation is not a major driver of overall risk in a 60/40 portfolio. With stocks generally measured as three-to-five times riskier than investment-grade bonds, a 40% allocation to bonds represents a minimal contribution to the 60/40 portfolio’s overall risk. This limits bonds’ ability to diversify the risk from stocks in 60/40 strategies, regardless of the asset classes’ correlation profile.3

We can demonstrate this mathematically. By taking the derivative of portfolio risk (i.e., standard deviation) with respect to the correlation coefficient, we arrive at a linear approximation of the impact on the total volatility of a 60/40 portfolio from a change in the correlation coefficient:

Note: σportfolio represents the risk of the portfolio, wstocks represents the portfolio weight in stocks (60% in this case), wbonds represents the portfolio weight in bonds (40% in this case), σstocks represents the risk of stocks, σbonds represents the risk of bonds, and ρstocks, bonds represents the correlation coefficient between stocks and bonds.

When reasonable assumptions are applied, the resulting number is quite small, suggesting that the impact on the risk of a 60/40 portfolio from a change in correlation is modest. We illustrate this relationship below.

Stock (global large-capitalization equity, currency-hedged) and bond (global investment-grade fixed income, currency-hedged) risk figures are based on SEI’s capital market assumptions. Stock risk assumption equals 19.2%; bond risk assumption equals 5.7%. Please see the important information section below for calculation methodology.

Starting with a fairly aggressive correlation assumption of negative 0.5, the equation above suggests that portfolio risk would rise by fewer than two-and a- half percentage points (roughly 2.49%) for a one-unit move in the correlation coefficient. This translates to a modest change in estimated risk given an extreme move in correlation (in this case, a change from -0.5 to +0.5). In less dramatic (and more realistic) scenarios, the impact on a 60/40 portfolio’s risk from changes in correlation is even smaller. The takeaway is clear: Changes to expected correlation, large or small, translate to only modest changes in expected risk in a 60/40 portfolio.

SEI’s diversified approach

The dynamic detailed above highlights the importance of SEI’s diversified approach to portfolio construction. Given the limited diversification opportunity available through a simple 60/40 portfolio, we believe that it is crucial to include additional asset classes with less-than-perfect correlation in order to maximize a portfolio’s expected risk-adjusted returns. Depending on the context, we view inflation-protected securities, below-investment-grade bonds, real assets, and alternative investments as valuable contributors to diversification. When used in combination with traditional stocks and bonds, these asset classes enable portfolios to succeed in a broader range of scenarios. The recent rise in stockbond correlation, driven in part by their shared vulnerability to rising inflation, provides a useful example: When compared to traditional 60/40 allocations, portfolios with exposure to inflation sensitivity were better hedged against the

risk of higher-than-expected inflation.

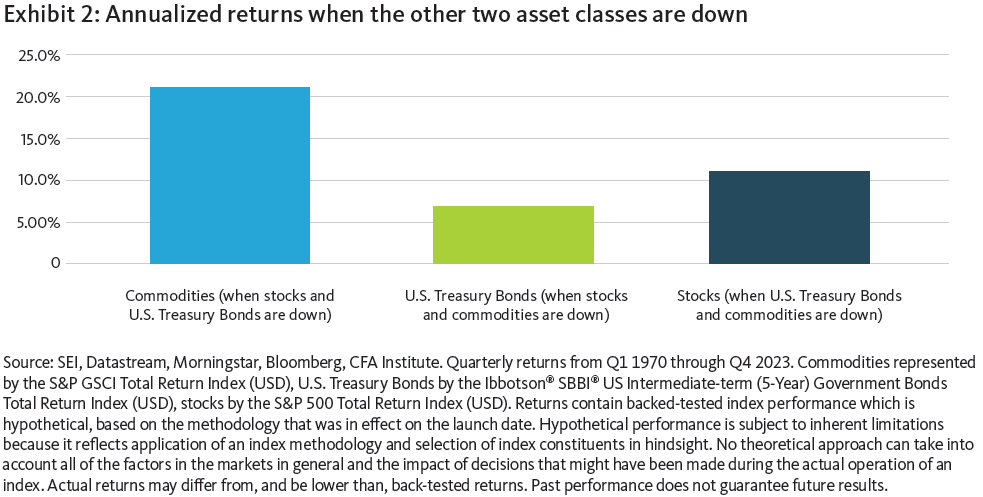

Exhibit 2 highlights the benefit of combining various sources of diversification in a broader portfolio. The chart represents the annualized returns of stocks, U.S. Treasury Bonds, and commodities in periods where two of the three asset classes deliver negative returns. The results should provide comfort for the well diversified investor: When two of the major asset classes have been down at the same time, the third has been materially positive on average. This suggests that even when correlations spike, allocating to additional asset classes can provide a significant diversification buffer.

In our view, reports of diversification’s death are greatly exaggerated. While a recent rise in correlation between stocks and bonds has marginally reduced the asset classes’ diversification benefit, this is a far cry from eliminating it entirely. Given our conservative approach to forming capital market assumptions and our robust efforts to exploit other sources of diversification, we believe our portfolios can succeed across a variety of market environments.

A note on assumptions

Our capital market assumptions are deliberately conservative, designed with the understanding that correlations can vary considerably over time and, particularly for risk assets, often rise during periods of market stress. As such, our correlation assumptions can skew higher than both historical averages and those of many of our peers. Given these conservative assumptions, we were not caught off guard by the recent rise in correlations between stocks and bonds. Quite the contrary in fact: A positive correlation between global stocks and investment-grade bonds is our baseline assumption.

This positive correlation is in no way a fatal blow to portfolio diversification. As long as correlations are not perfectly positive, combining multiple assets in a portfolio provides measurable diversification benefits. Particularly when allocations to asset classes beyond stocks and investment-grade bonds are also included, we remain extremely confident in the ability of diversified portfolios to maximize investors’ expected risk-adjusted returns.

Index definitions

Ibbotson® SBBI® U.S. Intermediate-term Government Bonds Total Return Index is an unweighted index that measures the performance of U.S. Treasury and U.S. Government Agency bonds with maturities between four and seven years.

The S&P GSCI Total Return Index is a composite index of commodities that tracks the performance of the global commodities market. It is composed of 24 exchange-traded futures contracts that cover physical commodities across five sectors. You cannot invest directly in an index.

The S&P 500 Total Return Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

Glossary

Alternative investments are financial assets outside of traditional asset classes (stocks, bonds, and cash).

Standard deviation is a statistical measure of the historical volatility of an investment. It measures the average periodic divergence from the investment’s average return. A volatile stock has a high standard deviation, while the standard deviation of a stable blue-chip stock generally is lower.

Treasurys are U. S. government debt obligations backed by the full faith and credit of the federal government. They are often used as a proxy for a risk-free asset for benchmarking and asset-valuation purposes.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence, or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research, or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative, or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting, and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial

Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is made available in Latin America, the Middle East, Australia, and the Nordics FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.