Economic Outlook: The Canadian Economy and the Challenges Beyond NAFTA

Canadians breathed a sigh of relief when the U.S. came to terms over a re-vamped North American Free Trade Agreement (NAFTA) deal, now known by the ungainly acronym USMCA (United States-Mexico-Canada Agreement). The deal gives the U.S. access to 5% of the Canadian dairy market, a similar share granted to European and Pacific-Rim nations as part of the EU-Canada Comprehensive Economic and Trade Agreement (CETA) and the Trans-Pacific Partnership (TPP) trade agreement. In return, the U.S. agreed to keep intact a NAFTA dispute-resolution mechanism known as Chapter 19. Canadian autos also would not be subject to import tariffs if the U.S. eventually decides to impose them on other countries. The USMCA still needs to be approved by a fractious U.S. Congress, but we’re assuming it will be supported once the politicians have their say in front of the cameras and, perhaps, after making some additional modest tweaks to mollify the newly empowered Democratic majority in the House of Representatives. In the meantime, U.S. President Donald Trump has generally left Canada alone, reserving his anti-NAFTA tweets for Mexico and the southern border.

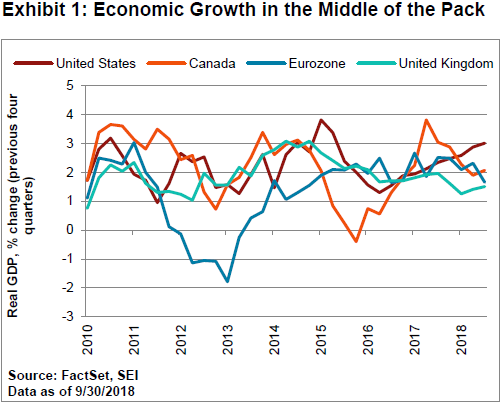

And so, economic life between Canada and the U.S. should go on as before. But there are other challenges facing Canada beyond NAFTA. . Inflation-adjusted economic growth—that is, real gross domestic product (GDP)—has been running at about a 2% pace for the 12 months ending September 30. That’s slightly better than the growth achieved in Europe, but it certainly looks disappointing versus the U.S. acceleration to 3% in the same one-year period (Exhibit 1). There has been a material downshift in Canadian household consumption, for example, as rising interest rates and high debt levels weigh heavily on disposable income. Fixed investment, meanwhile, has fallen in recent quarters. Businesses may have been discouraged from investing in plants and equipment owing to the uncertain outlook for NAFTA. Perhaps we will see some recovery in 2019.

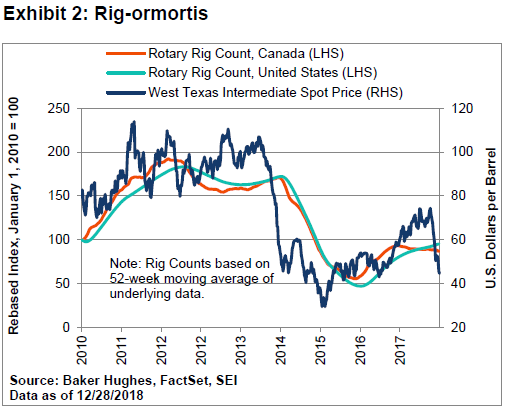

Investment in the oil patch is a different story, however. Canadian oil and gas producers recorded a reduction in total rig activity in 2018, even as global oil prices were rising (Exhibit 2). Pipeline and rail constraints that kept Canadian oil locked up in western Canada led to a sharp expansion in the discount at which Canadian oil traded versus West Texas Intermediate (WTI), a grade of crude oil that originates in the U.S. and is used as a benchmark in oil pricing. That differential has narrowed considerably since October, but mostly because the WTI price has collapsed. In addition to the negative effect on investment, the woes of Canadian oil should also bite into the revenues of the provincial governments of Alberta and Saskatchewan.

Trade in goods has been mixed. Total exports (measured as a 12-month moving sum to smooth out the fluctuations) have risen 6% in the year through October. Energy exports are up 17% (although the slide in oil prices should dampen this amount considerably in coming months), while other merchandise exports have advanced by a more sedate 3.6%. Non-oil exports have shown only modest growth since 2016 despite the relatively robust growth seen in the U.S. and the advantage of having a weak currency.

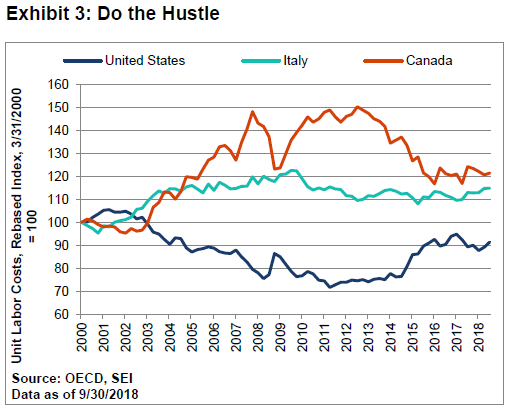

There’s an obvious reason why non-oil exports are growing more slowly than they should—Canada’s competitiveness, as measured by the trend in unit labour costs, leaves much to be desired. As Exhibit 3 highlights, Canada’s cumulative increase in unit labour costs over the past 18 years is worse than that of Italy. This poor performance even takes into account the decline in relative unit labour costs achieved between 2012 and 2015. That reduction was caused primarily by the sharp depreciation of the loonie against the U.S. dollar and the euro. More recently, it’s surprising to see that wage rates and other measures of labour compensation have eased. This has happened despite a relatively tight labour market. The unemployment rate fell to 5.6% in November, an all-time low.

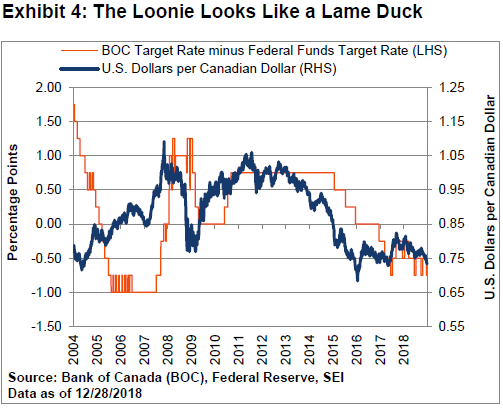

Like the U.S. Federal Reserve (Fed), the Bank of Canada (BOC) is expected to slow the pace of interest-rate increases in 2019. However, Canada’s policy rate of 1.75% remains a substantial 75 basis points below the U.S. federal-funds rate (Exhibit 4)—a differential that is probably more than is warranted by the economic fundamentals. Until that gap is reduced, we may see the Canadian dollar depreciate further.

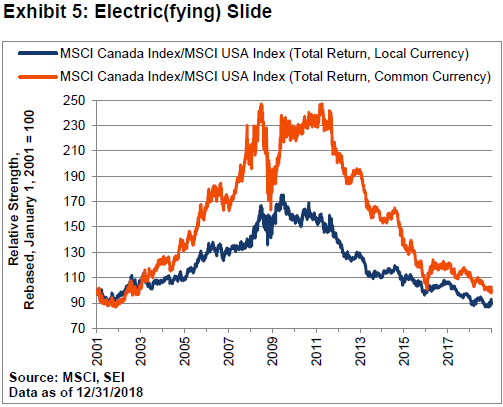

Canadian equities (as measured by the MSCI Canada Index, total returns) underperformed the U.S. stock market (as measured by the MSCI USA Index, total returns) in local- and common-currency terms in 2018. This continues a multi-year trend of poor relative performance that extends back to 2011. A weak loonie exaggerates this in common-currency terms, as seen in Exhibit 5. However, even in local-currency terms, the MSCI Canada Index languished at an 18-year low versus its MSCI USA Index counterpart.

SEI’s equity managers made minor modifications to their sector exposures, overweighting stocks with value characteristics and underweighting momentum. Sector-wise, our large-cap Canadian equity managers maintained overweights to consumer staples, consumer discretionary, information technology and telecommunications. Underweighted sectors included energy, financials, materials, utilities and real estate. Our fixed-income managers remained cautious on the rate outlook, favouring shorter-duration positions.

Party Over, or Will the Beat Go On?

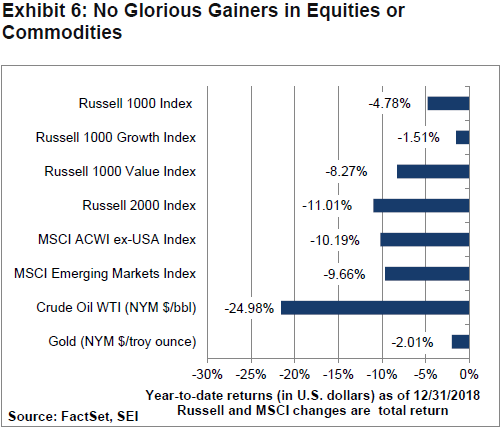

The year of 2018 provided few reasons for equity investors to celebrate, as illustrated in Exhibit 6. U.S. equities may have done better than those in most other regions and countries last year, but the correction in the fourth quarter was extremely harsh: U.S. large-cap stocks, as measured by the Russell 1000 Index, were down 4.75% for the year.

The Russell 1000 Growth Index did much better than the Russell 1000 Value Index, but the former came down hard in the fourth quarter after being up nearly 17% on a year-to-date basis through September.

Many stock markets outside the U.S. also ended the year with double-digit year-to-date declines. According to Ned Davis Research Group, 45 out of the 47 markets in the MSCI ACWI Index were down for the year. Nearly all of them (97%) registered peak-to-trough drops of at least 10%; more than a third (37%) are down in excess of 20%.

Among commodities, oil was the big loser, down almost 25% for the year. While gold displayed resiliency, even this defensive haven fell in price last year.

Among currencies, the U.S. dollar outperformed most others. This strength proved to be a major headwind for commodity pricing above and beyond the impact of China’s slowing growth, tariffs and the rumblings in energy markets caused by the U.S. shale boom. The U.S. dollar’s gain also added to the pain of U.S.-based investors in international assets who were not protected by currency hedging.

It should not be surprising that bonds provided superior performance on a relative basis, given the sharp retreat in equities. But even in fixed income, absolute performance was disappointing.

Poor asset returns were widespread in 2018 because economic performance outside the U.S. was mediocre. Political uncertainties and tensions also dented investors’ animal spirits. Unfortunately, there are few signs that these trends will change dramatically for the better in the near term.

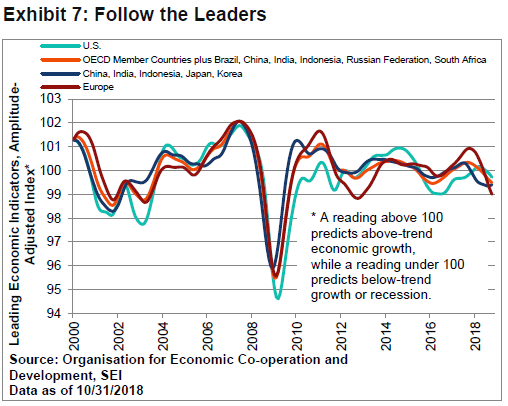

Exhibit 7 shows the leading economic indicators (LEI) figures for various country groupings, the broadest of which includes the 36 members of the Organisation for Economic Co-operation and Development (OECD) and six important non-member countries (Brazil, China, India, Indonesia, Russia and South Africa). As of October, all LEIs in the chart were below 100; this means economic activity is likely to be below trend into the spring and perhaps past the middle of the year.

The LEI statistics do not suggest recessionary conditions per se, but they do signal further deceleration in the growth of global GDP during the first half of 2019. Europe still appears particularly depressed. Its LEIs are currently as low as they were in 2012 when the region was in crisis. Italy is close to falling into recession yet again, after suffering a three-year downturn between 2011 and 2014. Germany recorded a negative GDP reading for the third quarter, although that result probably overstated the economy’s weakness. Meanwhile, the U.K. has endured a sustained period of sluggish growth owing to uncertainties surrounding Brexit and the country’s future economic relationship with the European Union (EU).

Overall, GDP growth in Europe has been trending in the 1.5% to 2.0% range, with further deceleration possible in 2019. This time last year, we were hopeful that Europe could build upon the improvement recorded in 2017. It certainly did not work out that way.

A Slower Tempo for the U.S. Economy

The economic performance of the U.S. also appears set to slow in 2019. Following a gain of more than 3% in 2018, we expect inflation-adjusted GDP to ease back toward 2.5% growth in the coming year. There already has been some deterioration in interest-rate-sensitive areas of the economy, especially housing and autos.

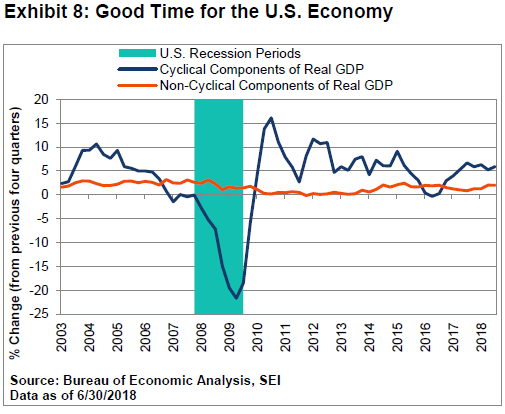

We nevertheless still view the U.S. economic position as fairly solid. Exhibit 8 breaks down U.S. GDP growth into cyclical (consumer spending on durable goods, residential and non-residential fixed investment and the change in business inventories) and non-cyclical (consumer spending on non-durable goods and services, government expenditures and net exports of goods and services) components. The cyclical components have been logging respectable year-over-year gains of more than 5% for the past several quarters.

We should point out that the less-cyclical components of GDP (household consumption of non-durables and services, government expenditures and net exports of goods and services) also appear rather healthy. The rate of change has picked up from the near-zero readings recorded for several years following the global financial crisis.

Catalysts for this acceleration include the improving economic position of U.S. households as labour markets tighten and real wage growth accelerates; increased government spending has also helped, with Congressional Republicans and Democrats wriggling out of the spending-sequester strait-jacket that had restrained defense and non-defense discretionary expenditures in previous years.

With Democrats controlling the House of Representatives and Republicans holding power in the Senate, any fiscal-policy agreement made during a period of political gridlock will likely mean slightly more federal-government spending—not less.

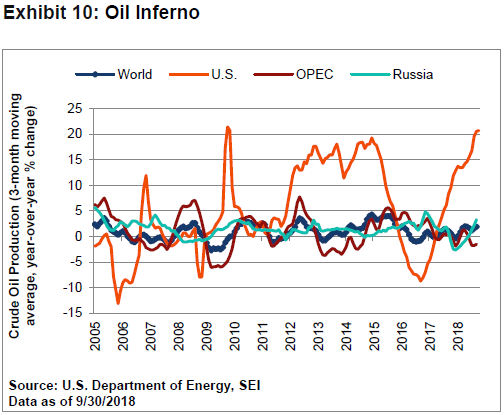

At SEI, we are not convinced that there will be the kind of sharp economic slowing in the U.S. that we had in the 2015-to-2016 period. Back then, investment in shale projects collapsed as oil prices tumbled below $30 a barrel. We do not believe that conditions in the oil-patch are as dire as they were three years ago; although some may think otherwise, given the precipitous slide of nearly 40% in the price of WTI crude oil since the end of September.

Despite the severity of the stock-market decline, we believe that the U.S. economic expansion has a good deal of life left in it. There is no expectation whatsoever of another global financial crisis, when both consumption and investment suffered catastrophic declines.

Even in an extraordinarily unfavourable economic scenario in which the tariff wars with China and other countries deepen and the Federal Reserve (Fed) raises interest rates too far and too fast, we doubt that the U.S. economy would experience anything worse than a garden-variety recession by 2021. The economic and credit excesses that usually precede a deeper recession simply aren’t to be found.

The decline in energy prices is especially good news for the broader economy since it reduces concerns about inflation accelerating beyond the Fed’s comfort zone anytime soon. It also lowers costs for consumers and businesses for a broad range of petroleum-based products, from gasoline to disco-style polyester suits.

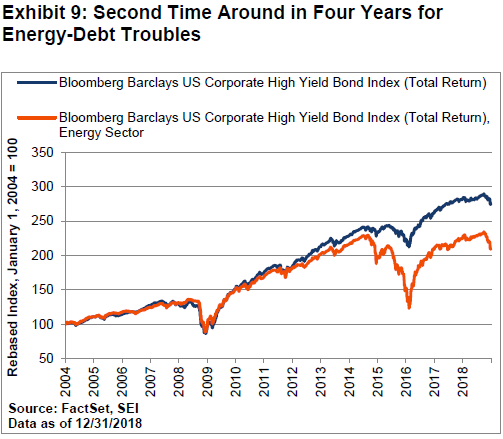

Of course, as in the 2015-to-2016 period, a collapse in oil pricing well below the cost of production would hurt oil-producing regions; it would also likely cause gyrations in the high-yield bond market as investors worry about shale producers’ ability to service their debt. Exhibit 9 highlights the recent decline in high-yield bond total returns for both the asset class and for energy-related issuers.

Still, this year’s price drop should lead to production cuts in some important shale basins, helping to bring supply into better alignment with demand. The current excess supply has mostly been caused by increased Saudi production. The Kingdom ramped up production on the assumption that sanctions on Iran would diminish supply. The supply/demand balance was upended when President Donald Trump’s administration granted 180-day waivers in October to eight key buyers of Iranian crude. That meant that at least 75% of Iran’s exports would continue to flow.

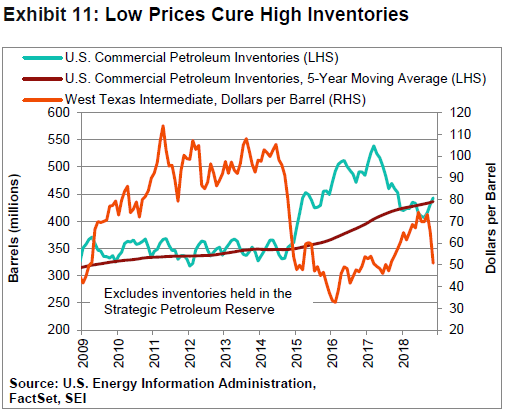

Members of OPEC, along with Russia, have agreed to cut production by 1.2 million barrels per day starting in January. Canada will also cut production by 325,000 barrels per day to ease infrastructure burdens in Alberta. Exhibit 11 compares the price of WTI crude oil to the level of commercial inventories in the U.S.

The price decline during the 2014-to-2016 period was precipitous, and the inventory rise relative to the five-year average was equally dramatic. It wasn’t until 2017 that production fell sufficiently to elicit a sustained rise in prices. The inventory gain in October exceeded the five-year average and dealt a heavy blow to prices and trader sentiment—yet we believe it should be far easier to correct than the inventory excess that prevailed two and three years ago.

The Fed Dances a Fine Line

The vibrant performance of the U.S. economy (relative to most developed economies, at least) in 2018 hardened the Fed’s resolve to normalize its federal-funds policy rate from the historic lows set during the global financial crisis. However, as the federal-funds rate approaches a level that can be judged as “neutral,” there is concern that the central bank will go too far and tip the economy into recession. Volatility in the U.S. financial markets has increased, at least in part, owing to this reason. Fed Chairman Jerome Powell’s press conference on December 19 was not well-received by investors because he seemed to downplay negative signals coming from the financial markets. We view this response by investors as an overreaction.

Powell and the other members of the Federal Market Open Committee (FOMC) are quite aware of the impact that rising rates and a flattening of the yield curve are having on interest-sensitive industry groups. Among S&P 500 Index sectors, the investment banking & brokerage group was down almost 25% on a total-return basis versus the 4.3% drop in the overall S&P 500 Index through December 31, 2018. The auto and housing sectors were down 30% and 25%, respectively.

The latest communication debacle notwithstanding, there has been a change of tone at the central bank. Some Fed officials, including Powell himself, explicitly acknowledge that the federal-funds rate now is near a level that can be considered neither stimulative nor deflationary. The so-called Fed dot plot—which reflects the individual policy-rate expectations of all Fed governors and regional presidents—also has shifted a bit to the downside, reversing the upward revision revealed six months ago in the FOMC’s Summary of Economic Projections report.

After raising the federal-funds rate in a steady and predictable fashion over the past two years, the Fed is changing course to a more reactive, data-dependent policy stance. This is reminiscent of the 2015-to-2016 period. During those two years, the FOMC overestimated the number of times the central bank would raise the funds rate—with only two increases ultimately implemented. Similar to today, global economic uncertainties abounded. Global oil markets were in a deep depression, leading to a bust in U.S. shale investment. The Chinese equity market imploded and economic growth slowed in that country, adding to the woes of other developing economies. In Europe, the travails of Greece spotlighted the fragility of the eurozone banking system and the region’s vulnerability to political fragmentation. Again, the Fed was forced to rethink the timing of its exit from near-zero interest rates and quantitative easing.

Fast forwarding to the present, the U.S. economy is clearly in better shape than it was three years ago. Labour markets certainly are much tighter, with the unemployment rate at its lowest level in five decades. The federal-funds rate is still quite low historically, and is just half a percentage-point above the inflation rate. Further increases in the funds rate should be expected. FOMC members still expect to push through two quarter-point rate hikes, followed by one additional increase by the end of 2020.

At SEI, we are penciling in just one rate increase in 2019, and perhaps one in 2020—but these are just guesses. Even the Fed’s decision-makers have no firm idea what they will end up doing. The important thing to remember is that the central bank is adopting a wait-and-see approach to monetary policy and has ended the nearly automatic quarterly rate increases of 2017 and 2018. Market expectations implied in the federal-funds futures market show that traders are skeptical that the Fed will raise rates at all from here.

While we disagree with the notion that federal-funds rate hikes have ended completely for this cycle, we recognize that there is sufficient reason for the Fed to pause. Although hourly wages in the U.S. have accelerated beyond 3% on a year-over-year basis, broader measures of labour compensation remain well behaved. Hourly compensation in the non-farm business sector, for example, is up just 2.2% year-over-year through the third quarter. Meanwhile, productivity (output per hour worked) has been perking up, gaining 1.3% over the same period. Unit labour costs expanded a mere 0.9% in the four quarters ended September.

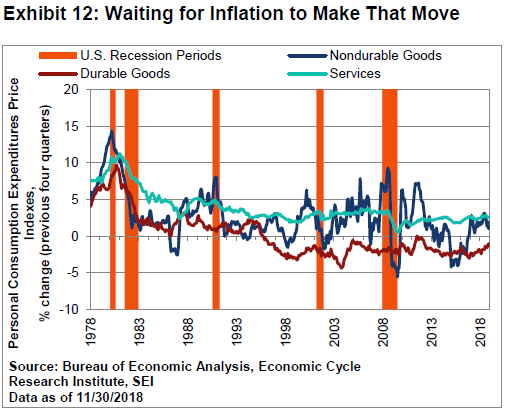

Some economists fear that inflation will accelerate as profit margins are pressured by rising wages and other input costs. So far, there is little evidence of that. Our best guess is that inflation, as measured by the U.S. Commerce Department’s personal-consumption expenditures price index (Exhibit 12), will remain near the Fed’s 2% target for another year. Despite the imposition of tariffs on aluminum and steel last spring and on a broad swath of Chinese goods in September, U.S. consumer prices for durable goods have continued to decline. Non-durable goods inflation is also likely to post outright declines in the months immediately ahead as the drop in oil prices feeds through to consumers. Services inflation, meanwhile, remains slightly elevated but is not yet accelerating in any worrisome way.

The Bull Market in Equities Will Revive,

Knock on Wood

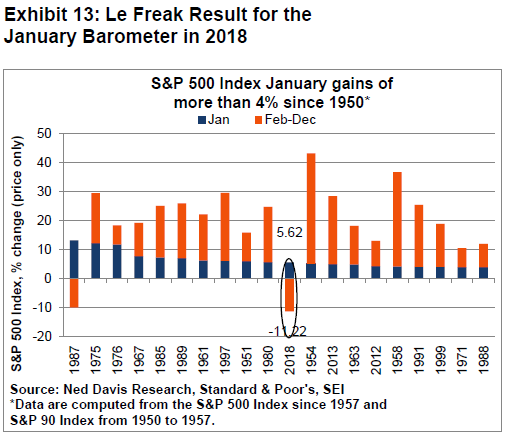

There’s no denying that U.S. equities have logged a disappointing performance in the past year despite a bullish fundamental backdrop of solid domestic economic growth, moderate inflation and a boom in corporate profitability. Indeed, it’s been one of those rare years when the market got off to an excellent start, only to stumble over the following 11 months (Exhibit 13). In January, the S&P 500 Index jumped by 5.6%. Between February and December, however, prices fell by 11.2%. There has been only one other year (1987) in which the S&P 500 Index gained more than 4% in January but failed to build on that performance through the remainder of the year.

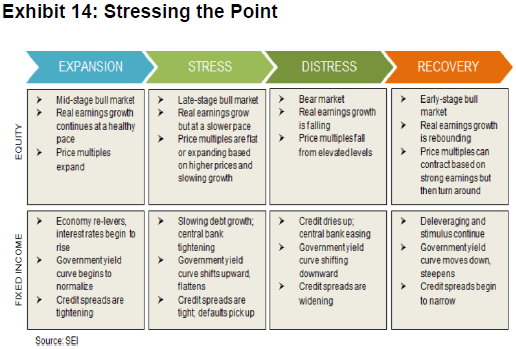

Exhibit 14provides a stylized cycle analysis for the equity and bond markets. We highlighted this chart nine months ago, when both asset classes were still judged to be in the expansion phase of their cycles. It’s a good time to reassess where we are now. There certainly seem to be additional signs of stress, even some distress, but also signs of expansion.

Perhaps the best that can be said is that financial markets are in the midst of a messy transition. Corporate earnings and inflation-adjusted household income growth have been strong in the U.S. (expansion phase), but investment-grade and high-yield credit spreads have widened (distress). Earnings multiples have declined meaningfully and the Chicago Board Options Exchange Volatility Index (VIX) briefly surged above a reading of 30,which signals distress. Meanwhile, the Treasury yield curve has continued to flatten, indicating stress.

In all, the U.S. financial markets and economy definitely appear to be in the later stages of their cycles. Bearish investors probably disagree with the notion that the stock market can still be considered a turnaround candidate. We think the odds favour a strong rebound in U.S. equity prices for the following reasons:

- The U.S. economy should continue to grow while corporate earnings are expected to post a mid-to-high single-digit gain in 2019.

- Valuations for the S&P 500 Index have declined from almost 19 times one-year forward earnings to an attractive level of almost 14 times following the decline in share prices.

- Bond yields remain rather low and have moved down again in the past two months, bolstering the case for riskier assets.

- Investor risk aversion has increased, so we think much of the bad news of recent months is reflected in current stock prices.

- Upside surprises remain possible; for example, China and the U.S. could step back from a full-blown tariff war, the Fed could refrain from further rate increases until later in 2019, the U.K. may agree to a soft Brexit/no Brexit deal and corporate profit margins could stay elevated as unit labour costs in the U.S. continue to track below expectations.

- Fiscal policy should not be the strong catalyst for growth that it was in 2018, but the impact of political gridlock should still be mildly expansionary.

SEI’s U.S. large- and small-capitalization portfolios have mostly held to their positions during the fourth-quarter selloff and remain overweight to the financial sector. Value-oriented strategies have struggled this year and are behind their benchmarks, mainly owing to overweight positions in financials, materials and energy. Utilities, which active managers tend to underweight on account of their high debt and regulatory burdens, outperformed in the fourth quarter as investors sought safe havens. Our factor analysis shows that the most important differentiator for returns (not just in U.S. equity, but across geographies) is high-versus-low volatility. Value in the past was a reliably low-volatility equity factor, but has shifted toward high-volatility. The stability factor was the big winner in the quarter, led by utility stocks. Momentum, meanwhile, badly underperformed, reflecting sharp price declines in technology shares.

Our fixed-income portfolios have made modest changes in their positioning. They have moved to a slightly long duration stance from neutral and now have a modest underweight to corporate credit.

The investment managers that we work with generally expect Treasury bond rates to drift higher from current levels, although most expect the increase to be well-contained. There continues to be an inclination to add to duration when the 10-year benchmark bond yield moves above 3.10%.

In high yield, our portfolio continues to be short the benchmark’s duration and feature higher yields. The leisure, retail and media sectors are favoured, while the basic materials and financial sectors represent the biggest underweights.

The Brexit Saga: Never Can Say Good-Bye

U.K. Prime Minister Theresa May was probably humming Gloria Gaynor’s 1978 hit “I Will Survive” on the evening of December 12 as she waited for the results of the no-confidence vote held in Parliament.

She did survive, at least temporarily, with a required promise to step down prior to the next general election—which must be held by May 5, 2022. May could leave her post earlier than that, either via another leadership challenge at the end of 2019 or if she voluntarily steps down, depending on the outcome and the economic fallout of the Brexit saga.

This time last year, we accurately pointed out that the Northern-Ireland-border debate would be one of the most difficult items to address. Sure enough, the prospect of an open-ended arrangement—in which goods flow between Northern Ireland and Ireland in exchange for the free movement of European citizens and adherence to EU regulations and legal structures—has led to a political impasse. The deal that May’s government negotiated has enraged Brexiteers and badly splintered the prime minister’s own Conservative Party.

We think it unlikely that the U.K. will fall out of the EU without some sort of deal in place. A no-deal Brexit would strike a mighty blow to the economy. Bank of England (BoE) Governor Mark Carney has likened the probable impact to the oil shocks of the 1970s.

The negative shock on merchandise trade would be substantial because dealings with the EU would revert to the most-favoured-nation rules of the World Trade Organization (WTO). It’s estimated that U.K. import prices would increase by more than 4% on average. Autos, for example, would face a 10% tariff and car parts a rate of just under 3.7%. Many plastic goods would be hit with a 6.5% tariff. Some agricultural products imported from the EU would be subject to a tariff in excess of 20%. Monitors and televisions would be hit with a 14% rate. In addition to the tariff increases, a hard Brexit is expected to cause massive border delays. This would be damaging to trade in perishable products and could severely disrupt manufacturers’ supply chains and just-in-time production processes.

Trade in financial services, a category not well-addressed by WTO rules but critical to the U.K.’s economic well-being, would be saddled with increased regulations, paperwork and costs. According to an article1 in The Wall Street Journal, consulting firm Boston Consulting Group UK LLP estimates that £2.4 trillion ($3 trillion) of loans, securities and derivatives may need to shift into EU-based bank entities if the U.K. leaves the EU in a hard-Brexit scenario. The BoE has warned that over-the-counter derivatives totaling £41 trillion ($52 trillion) at U.K. clearing houses may need to be repapered. In mid-December, EU governments agreed to grant “equivalence” rights that will maintain EU companies’ access to U.K.-based clearing houses for 12 months following Brexit. This buys time for markets to adapt and contracts to run off without disruption—but a no-deal Brexit would be an especially costly outcome for companies in both the U.K. and the EU due to decreased access to low-cost capital.

Even at this late date, there is tremendous uncertainty as to the ultimate outcome. Some observers see May’s survival of the no-confidence vote as strengthening her hand, eventually leading to approval of the deal that’s on the table. Others see her as a lame duck, perhaps still in power but not having power. We believe that the real choice now is between the prime minister’s Brexit deal or no Brexit at all; we view a no-deal Brexit as a non-starter because the pain would be so great.

A no-Brexit-at-all scenario could take one of two forms. In the first alternative, the U.K. government could unilaterally revoke Article 50, basically calling off the divorce from the EU. It would remain a full member with all the obligations and benefits membership entails. The European Court of Justice ruled that such unilateral action is permitted. No other member country can block it.

Of course, this decision would be in defiance of the June 2016 referendum that started the whole Brexit process in the first place. It could lead to the downfall of the government, paving the way for general elections and the possibility of a Labour government headed by socialist Jeremy Corbin. To say this would be an anti-business and anti-market event would be to engage in British understatement.

The second alternative is to go back to voters and hold a second referendum. Although the legality would be disputed, we think this is the far more likely scenario—assuming that the survey polls are correct about enough voters changing their minds about Brexit now that they are aware of how complicated and costly leaving the EU can be. The financial markets probably would respond quite positively to this decision. Of course, there is always the chance that the Brexiteers will prevail yet again. We anticipate another close vote if one were to take place. Although May continues to say that a second referendum is out of the question, we believe the odds have increased.

A second referendum would take time to organize. The May government would likely need an extension of the Article 50 deadline beyond March 29. Such an extension would likely be granted by the other EU members, but it just takes one member country to throw a spanner into the works. Another complicating factor: EU parliamentary elections are scheduled for May 23. The U.K. could well be eligible to participate under an Article 50 extension even if it votes to leave soon thereafter. Clearly, the complications are immense and the permutations many. The next big Brexit development will be the “meaningful” vote in Parliament in mid-January.

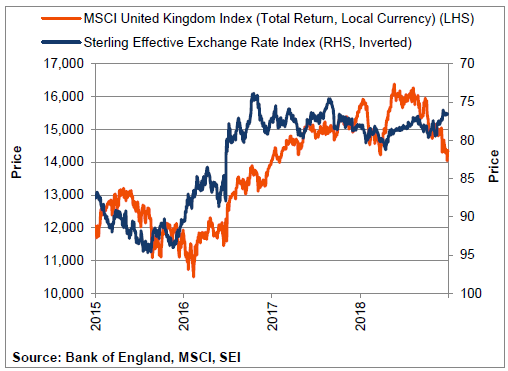

Since the Leave referendum on June 23, 2016, it has been a tale of two markets for U.K. equities. Following the initial shock one day after the vote, U.K. equities caught fire as investors responded positively to sterling’s decline. This is illustrated in Exhibit 15 (note that the axis tracking sterling is inverted; when the currency is weak, the line goes up).

Exhibit 15: More Night Sweats than Night Fever

Rebounding oil and metals prices and stronger global demand during the second half of 2016 and into 2017 also helped investors place Brexit worries to one side. In contrast, equities have been on a downhill path since mid-2017, when May’s gamble to increase her majority by calling a snap election backfired. Investors quickly revised their view of Brexit, anticipating the problems we now see.

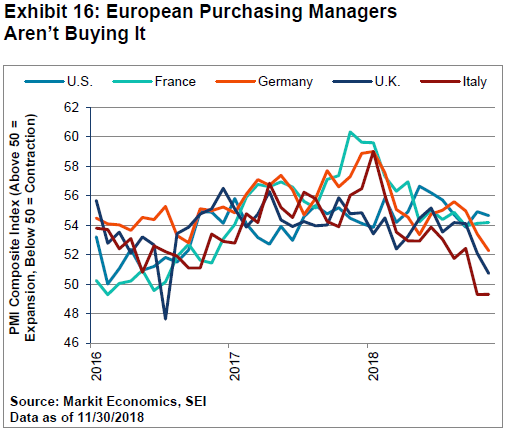

It hasn’t helped that economic growth in the U.K. and Europe has been disappointing. Purchasing managers in the major European economies have signaled declining momentum throughout the year from what had been high levels of manufacturing and services activity (Exhibit 16). The deceleration has been especially pronounced since mid-year. Italy’s composite purchasing managers’ index (PMI) has fallen into contraction territory.

There’s no mystery as to why economic performance has been so disappointing. Globally, trade volumes are down.

EU exports are highly leveraged to the global trade cycle, so investors were quick to reduce exposure to European exporters. It doesn’t help that the German auto industry has been working through its diesel emissions scandal, resulting in a sharp output decline.

Brexit uncertainties are nearly as much a factor on the Continent as they are in the U.K., but there is so much more helping to cloud the outlook. The push to ease fiscal austerity in Italy and the recent riots in France have served as a reminder that all is not well within the eurozone. In recent weeks, the coalition government in Italy has back-pedaled on its demands, enabling the country to reach an agreement with Brussels. That’s the good news. The bad news is that Italy will likely continue to push hard against budgetary rules in the years ahead, especially if the populist parties remain in power. It’s not at all clear how the country’s politics will play out.

In France, President Emmanuel Macron is facing a tough political challenge to his reform agenda. His popularity has plummeted, with a current approval rating of only 25%. Although there is no danger that his government will fall, it is possible that economic reforms will be severely watered down. It would not be the first time a French president with big ideas has seen his agenda shredded by citizens taking to the streets. The situation shows how hard it is to change the economic status quo in that country.

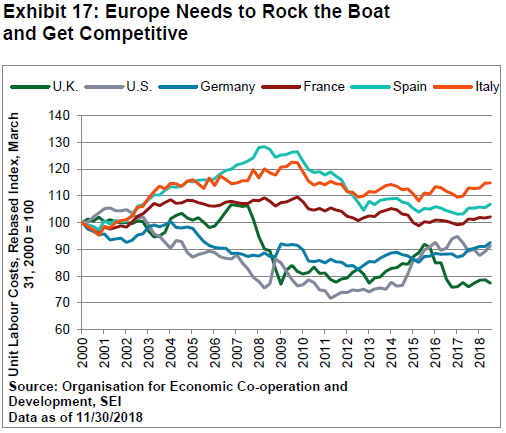

Exhibit 17 shows the trend in unit labour costs of the major European countries. We include the U.S. as a reference. Unit labour costs have been rising modestly in recent years for the countries shown in the chart—with the notable exception of the U.K., which has seen its competitiveness improve as a result of sterling’s depreciation.

Ominously, Italy’s unit labour costs are rising faster than most. There continues to be a wide gap between the high-cost structures of Italian companies versus those of other countries. Since the country cannot improve its competitive position through currency devaluation, it is destined to continue to struggle economically.

Europe’s growth issues probably mean that inflation will continue to run well below target in 2019. Core inflation (excluding energy, food, alcohol and tobacco) is running at just a 1% year-over-year pace, a trend that has been in place the past six years. Headline inflation, which fluctuates with energy prices, could pull back sharply from the 2% it recently reached.

We think monetary policy in the eurozone could stay on hold through the entirety of 2019. The European Central Bank (ECB) has completed its tapering of quantitative easing. It should now keep its balance sheet steady, reinvesting interest and the proceeds from maturing securities. Policy rates are not likely to be normalized anytime soon.

Meanwhile, ECB President Mario Draghi’s term ends October 31, 2019. This could add a layer of uncertainty for investors in European securities if it appears as if a more hawkish central banker will take his place. Although the ECB now has certain crisis-fighting programs in place (for example, the European Stability Mechanism), the continuing reluctance of creditor countries to support the debtor countries by shoring up the latter’s banks or guaranteeing bank deposits means that any attempt to respond to a crisis will be as arduous and hard-fought as during previous episodes of financial and economic stress.

All in all, it is hard to wax enthusiastic over Europe’s economic prospects. This is reflected to some extent in the valuation of Europe’s equity markets. The MSCI EMU Index (European Economic and Monetary Union) price-to-earnings ratio has sunk to less than 12 times from nearly 15 times at the start of the year. On the other hand, valuations aren’t nearly as depressed as they were in the middle of the periphery debt crisis. A variety of concerns have to ease before investors are likely to jump back into a region where growth is sluggish, banks remain stressed and the monetary authority doesn’t have as many tools in its toolbox to support economic growth as other major central banks.

To sum up:

- The outlook for the U.K. and Europe is far from rosy, although not in the kind of full-blown crisis seen in the periphery debt debacle of 2010 to 2014 or the global financial upheavals of 2007 to 2009.

- A resolution to the Brexit question will eliminate one major source of uncertainty for investors, but the next few months can still be volatile as the late-March Brexit date nears.

- Although the banking system is in better shape than it was in the immediate aftermath of the global financial crisis, it is still vulnerable at a time when the ECB is in a holding pattern, policy-wise, and possesses only a few options in the event of a financial emergency.

- Europe can be viewed basically as a low-growth value stock, heavily exposed to financials, materials and utilities, with little exposure to technology. A recovery in China’s economy (and in global trade more generally) is necessary for better economic and stock-market performance.

- Valuations are undemanding, reflecting investor bearishness. Note that European equities outperformed U.S. equities in the final quarter of 2018.

As in the U.S., SEI’s international equity portfolios have not engaged in any material positioning changes and are waiting out the market turbulence. Equities with value characteristics appear attractive.

Japan Still Trying to Turn the Beat Around

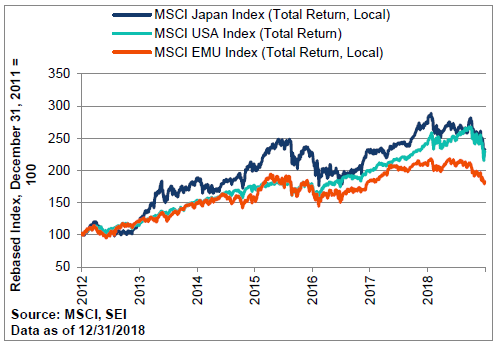

Japan’s stock market has not been roiled by anything as dramatic as Brexit or Italian fiscal defiance as we’ve seen in Europe, but its performance this year has been even worse than that of the eurozone in local-currency terms: The MSCI Japan Index has plummeted by nearly 15% and the MSCI EMU Index was down about 12% for the year, versus a 4% decline for the MSCI USA Index (local currency terms). Over the course of Shinzo Abe’s term as prime minister, however, Japan’s equity market has done rather well (Exhibit 18), posting a cumulative total return of almost 130%. That’s in line with U.S. performance and far better than the 80% total return achieved by the MSCI EMU Index (local-currency terms).

The Japanese government should certainly get high marks for its bold pursuit of monetary, fiscal and structural reform, known as the “Three Arrows.” We think the most successful of these has been the structural reforms. Labour policies have resulted in increased participation of women in the workforce (although most are still relegated to lower-level corporate positions). Trade barriers have been reduced (the country took a leading role in concluding the Trans-Pacific Partnership talks after the U.S. pulled out on the very first day of Trump’s presidency).

Most importantly for investors, corporate governance has increased. To be sure, there is still room for improvement, as the Ghosen affair at Nissan highlights. Yet, return on equity among publicly-traded companies has risen, and shareholders have been receiving better treatment via dividend increases and stock buybacks.

Exhibit 18: Japan to Investors: “I’ll Be Good to You”

Growth, however, continues to be constrained by a number of factors, some temporary and some structural. The aging of the population and its decline represent the most important structural headwind. Natural disasters had a significantly negative impact in 2018, pushing the economy into negative territory in both the first and third quarters; there was no growth in GDP measured over the four quarters through September.

Among the concerns for 2019: the outcome of the tariff war between the U.S. and China and the blowback it could have on global trade; a scheduled increase in the national sales tax in October (the previous increase in April 2014 is now viewed as a mistake because it blunted the economy’s forward momentum); and the ongoing battle against deflation.

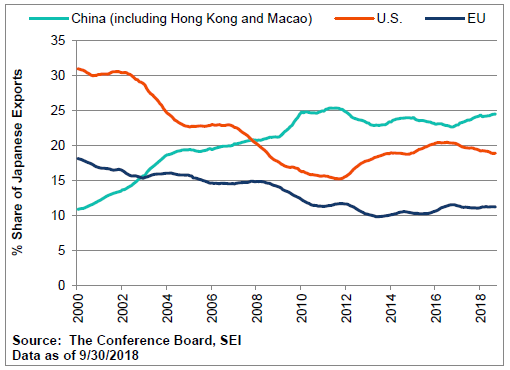

As far as the tariff war is concerned, Japan appears to have benefited in the early stages of the conflict. As shown in Exhibit 19, the share of Japanese exports to China (measured in U.S. dollars as a running 12-month total) rose at a robust pace through the first nine months of 2018.

More timely data indicate a decline in exports to China, however. German exports (not shown) also exhibited decent growth. By contrast, U.S. exports have fallen hard. China apparently substituted industrial goods it would normally import from the U.S. with goods from other countries. Of course, Japan cannot be seen as undermining U.S. policy against China, lest it become the focus of the Trump administration’s ire. Japanese companies with large export businesses have been badly lagging the market since September.

Exhibit 19: Japan Can’t Get Enough of China’s Love

The consumption tax, scheduled to rise in October 2019 from 8% to 10%, is an additional concern. Prime Minister Abe certainly remembers the negative impact the last hike had on consumer spending in 2014. Year-on-year household spending fell deeply into negative territory through much of 2014 and 2015. The government plans to ease the blow this time by providing shopping incentives and engaging in infrastructure projects to repair airports and floodwalls damaged by last year’s earthquake and major typhoon. According to the government, these initiatives may offset the impact of the tax hike by as much as three-fifths. However, similar measures were put in place in the aftermath of the consumption tax increase in 2014, with little apparent benefit.

There is one other possible important offset from the depressive effect of the consumption tax hike: The 2020 Summer Olympics will be held in Tokyo, which should provide a big lift to construction in 2019 and to tourism in 2020.

As for the third concern (deflation), Japan has yet to find the solution. Consumer prices excluding food and energy were virtually flat on a year-over-year basis for the third year in a row. Although monetary policy has been tweaked, we doubt there will be any serious effort to move away from negative/zero interest rates or large-scale central-bank purchases of securities. The Bank of Japan really has no choice but to continue to engage in extraordinary monetary expansionism in 2019 and beyond. Investors think so too: The Japanese Treasury yield curve remains slightly negative out to ten years.

Emerging Markets: Time for China to

Get Up on the Dance Floor

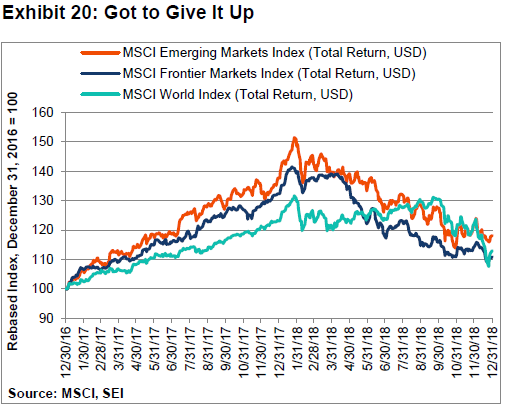

Emerging-market equities and bonds were stomped upon in first three quarters of 2018. Only a handful of emerging-market energy-sector stocks and a few sovereign bonds managed to eke out positive total returns last year. About 95% of all emerging-market assets declined in U.S. dollar terms. Such widespread carnage has not happened since the global financial crisis of 2008 and the bursting of the tech bubble in 2000. In contrast, 2017 was a banner year for emerging markets, with nearly all asset classes gaining ground. We think that 2019 could be another banner year.

Exhibit 20 highlights the rollercoaster ride since the start of 2017 in the MSCI Emerging Markets and MSCI Frontier Markets Indexes. We also include the MSCI World Index, a benchmark for developed-country stock-market performance, to highlight the comparative volatility.

It may be cold comfort to investors, but the 18% cumulative rise in the MSCI Emerging Markets Index over the past two years still exceeds the 13% gain in the MSCI World Index. We also note that emerging-market equities have outperformed developed markets during the downdraft that began in September of 2018.

On a country basis, Argentina takes the prize for being one of the most volatile stock markets in the world over this two-year period. It was a darling of investors in 2017, gaining 73.4%. Last year, it fell by more 50%—resulting in a cumulative two-year loss of 25%.

Among the larger countries, China still shines over a two-year timespan, although it was down by more than 25% from its peak in January through the end of last year.

Brazil, meanwhile, was something of a bright spot in an otherwise dismal picture, recording a flat performance in 2018. The country’s stock market rose by 24.5% in 2017, lagging the MSCI Emerging Market Index by 13 percentage points.

We are leaning on the optimistic side for emerging markets in 2019; although a few missing pieces of the puzzle need to be put in place. The valuation piece is already there, in our opinion. The price-to-forward-earnings ratio collapsed from 13 times at the end of January to 10.5 by year-end. Analysts’ year-ahead earnings expectations have declined surprisingly little over the year, by only about 5%. This seems reasonable, since the global economy continues to grow, albeit at a slower-than-desired pace.

In any event, the price-to-earnings ratio for emerging-market equities has been compressed back toward the levels last seen in 2014 and 2015, a period that has some parallels to today—such as concerns about Chinese debt, global growth and weak commodity pricing.

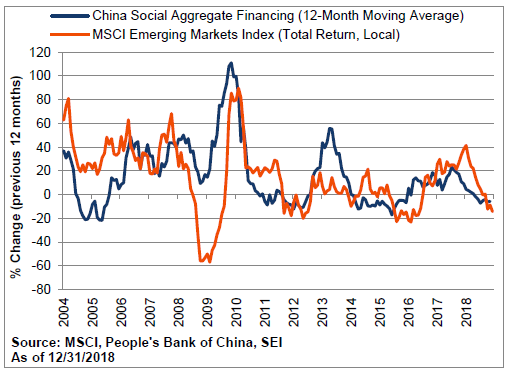

What could be the catalyst for a turnaround? In the past, it has been China. Exhibit 21 compares the performance of the year-over-year change in the MSCI Emerging Markets Index versus China’s social aggregate financing to its economy. Big debt expansions in China typically lead to big gains in emerging-market equities.

The question is whether the Chinese government has the will to go back to the debt well one more time. China’s regulators have been working hard to gain control over the shadow banking system. There is also the belated realization that excess debt creation causes economic imbalances and a severe misallocation of resources (property booms, excessive productive capacity, ghost cities, and high-speed trains to nowhere).

That said, we think that the Chinese government places social cohesion and Communist Party dominance ahead of economic virtue. China’s growth was slowing even before this year’s trade battles with the U.S. It surely would be a big positive for the country if the threat of tariffs was negotiated away, but we’re not holding our breath despite ongoing negotiations. On the contrary, the U.S.-China economic relationship will likely continue to deteriorate as the Trump administration seeks a way to level the playing field—even if it means a less efficient global trading system. When push comes to shove, the Chinese government will likely get even more aggressive in easing lending constraints if the situation warrants.

Exhibit 21: “I Need Your Lovin’”

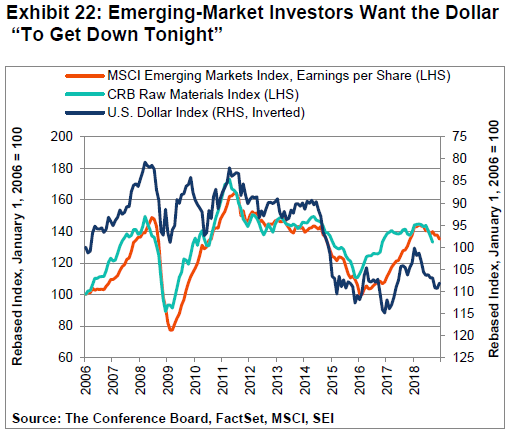

The other likely possibility is a change in the U.S. dollar’s trend. As we show in Exhibit 22, commodity prices and the earnings of emerging-market companies are closely correlated in inverse fashion with the movements of the greenback (the y-axis for the dollar is reversed in the chart, so the line goes down when the dollar appreciates).

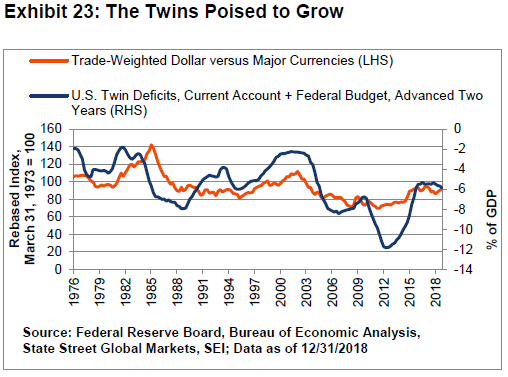

Fundamentally, there are a variety of reasons why the dollar could lose steam over the year ahead. First, last year’s appreciation has brought the U.S. currency’s broad trade-weighted value almost back to the previous highs of two years ago and the secular peak reached in 2001. A high dollar works at cross-purposes against President Trump’s desire to reduce the trade deficit. Indeed, not only will the current account deficit tend to expand as U.S. exporters and import-sensitive companies lose market share, but the fiscal budget deficit looks set to worsen too. The direction that the sum of capital account and budget deficits (popularly known as the “twin deficits”) takes usually correlates with broad movements in the U.S. currency. We highlight the twin deficits in Exhibit 23.

For most of 2018, the U.S. dollar has been gaining against other currencies, putting downward pressure on commodity prices and the earnings of the energy and materials companies that are a large part of the MSCI Emerging Markets Index. In 2017, the opposite conditions held. SEI is looking for another change in the U.S. dollar’s trend in 2019.

Second, we think that U.S. economic and corporate earnings performance will converge toward that of other developed countries (growth will not likely be head-and-shoulders above those of other countries in 2019 as it was in 2018). If there are positive developments in some of the pressure-point issues that have roiled markets, such as tariffs and Brexit, then investment capital could flow away from the U.S. and back into the world. This would remove an important source of support for the U.S. currency—and a big headwind from the rest of the world. This potential for a reversal in investment flows could accelerate if Fed policy becomes more dovish than currently projected by the central bank.

We have a positive outlook for emerging markets in our equity positioning on the assumption that the U.S. dollar will indeed decline against other currencies in 2019. Geographically, our portfolio favoured Latin America, with Brazil as the largest active weight. We were heavily underweight China and Taiwan, reflecting a structural bias toward smaller, faster-growing regions. A bias against momentum (mainly technology) also came into play.

Why CMAs (Capital-Market Assumptions)?

The awful performance of risk assets in the fourth quarter can certainly prey on investors’ emotions. Yet, as we tried to show in this report, the global economy is not exactly in dire straits. Yes, there are an unusually large number of uncertainties and concerns, some of which could have a material impact on growth if the worst came to pass.

Despite this, our confidence is increasing that we are nearing an end to the selloff. The sheer ferocity of the recent correction (the worst peak-to-trough drop in the S&P 500 Index since 2011) is reminiscent of other times in the past eight years when risk assets sold down hard, only to turn around and hit new highs.

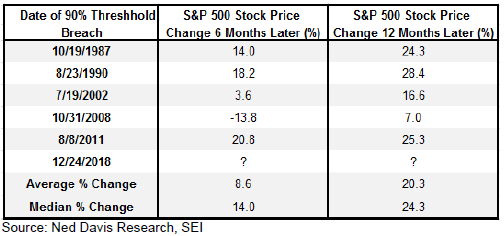

Exhibit 24 examines one of our favourite indicators that we employed when marking the U.S. market bottoms of 2011 and 2016. It’s not very complicated, and has nothing to do with fundamental analysis. It simply measures the percentage of stocks that are trading below their 200-day moving average.

In the week before Christmas, more than 90% of U.S. multi-cap stocks (as measured by Ned Davis Research Group) were trading below this threshold. That is an extremely rare event. Such a large percentage has been reached less than 2% of the time since 1981, typically near the tail-end of a correction or bear market. In the table, we look at where the U.S. stock market ended up 6 and 12 months after this threshold was first breached. Since July 1981, when the data first became available, we count only five episodes. One year later, the S&P 500 Index (price only) averaged 20.3% higher.

Exhibit 24: “Ring My Bell” at the Market Bottom

During periods of market volatility like the one we’ve been going through, we make sure to remind investors about the importance of sticking with a strategic and disciplined approach to investing that is consistent with personal goals and risk tolerances. Diversification is the key to that approach, and the construction of portfolios is consistent with our long-term CMAs.

Ultimately, the value of these assumptions is not in their accuracy as point estimates but in their ability to capture relevant relationships—as well as changes in those relationships as a function of economic and market influences.

As painful as the past three months and the past year have been for risk assets, these gyrations have not been outside the norm. Rather, given our views that the global economy will continue to grow and that market participants are overreacting to the concerns of the day, we see another important risk-on opportunity developing in equities and other risk assets. We believe a rebalancing of assets back toward undervalued equity classes may be an appropriate and timely response.

Glossary

Cyclical sectors, industries or stocks are those whose performance is closely tied to the economic environment and business cycle. Cyclical sectors tend to benefit when the economy is expanding.

Duration is a measure of a security’s price sensitivity to changes in interest rates. Specifically, duration measures the potential change in value of a bond that would result from a 1% change in interest rates. The shorter the duration of a bond, the less its price will potentially change as interest rates go up or down; conversely, the longer the duration of a bond, the more its price will potentially change.

Momentum refers to the tendency for assets’ recent relative performance to continue in the near future.

Spread is the additional yield, usually expressed in basis points (one basis point is 0.01%), that an index or security offers relative to a comparable duration index or security (the latter is often a risk-free credit, such as sovereign government debt). A spread sector generally includes non-government sectors in which investors demand additional yield above government bonds for assumed increased risk.

Stability refers to the tendency for low-risk and high-quality assets to generate higher risk-adjusted returns.

Value refers to the tendency for relatively cheap assets to outperform relatively expensive assets.

Index Definitions

Bloomberg Barclays 3-Month Treasury Bill Index: The Bloomberg Barclays 3-Month Treasury Bill Index measures the performance of U.S. Treasury bills with a remaining maturity of less than three months.

Bloomberg Barclays Long U.S. Aggregate Government/Credit Index: The Bloomberg Barclays Long US Government/Credit Index measures the investment return of all medium and larger public issues of U.S. Treasury, agency, investment-grade corporate and investment-grade international dollar-denominated bonds with maturities longer than 10 years. The average maturity is approximately 20 years.

Bloomberg Barclays US Aggregate Bond Index: The Bloomberg Barclays US Aggregate Bond Index is a benchmark index composed of U.S. securities in Treasury, Government-Related, Corporate and Securitized sectors. It includes securities that are of investment-grade quality or better, have at least one year to maturity and have an outstanding par value of at least $250 million.

Bloomberg Barclays US Corporate High Yield Index: The Bloomberg Barclays US Corporate High Yield Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody's, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded.

Bloomberg Barclays US Corporate High Yield Index—Energy Sector: The Bloomberg Barclays US Corporate High Yield Index —Energy Sector measures the energy sector portion of the Bloomberg Barclays U.S. Corporate High Yield Index.

Bloomberg Barclays US Government/Credit Bond Index: The Bloomberg Barclays US Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the US Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate Treasurys, government-related and corporate securities.

Bloomberg Barclays US Treasury 1-5 year Inflation-Linked Index: The Bloomberg Barclays US Treasury 1-5 year Inflation-Linked Index measures the performance of U.S. Treasury inflation-protected securities with a maturity between 1 and 5 years.

Chicago Board Options Exchange Volatility Index (VIX): Chicago Board Options Exchange Volatility Index uses option prices on the S&P 500 Index to estimate the implied volatility of the S&P 500 Index over the next 30 days. Options are derivative contracts that give a buyer the right (and impose upon the seller an obligation, if called upon by the buyer) to buy or sell an underlying security at a specified price, usually for a specified period of time.

CRB Raw Materials Index: The CRB Raw Materials Index is a measure of price movements of sensitive basic commodities whose markets are presumed to be among the first to be influenced by changes in economic conditions.

ICE BofAML US High Yield Constrained Index: The ICE BofAML US High Yield Constrained Index measures the performance of high-yield bonds.

JP Morgan EMBI Index: The JP Morgan EMBI Index is a total-return, unmanaged trade-weighted index for U.S. dollar-denominated emerging-market bonds, including sovereign debt, quasi-sovereign debt, Brady bonds, loans and eurobonds.

JP Morgan EMBI Global Diversified Index: The JP Morgan EMBI Global Diversified Index tracks the performance of external debt instruments (including U.S. dollar-denominated and other external-currency-denominated Brady bonds, loans, eurobonds and local-market instruments) in the emerging markets.

JP Morgan GBI Emerging Markets Global Diversified Index: The JP Morgan GBI Emerging Markets Global Diversified Index tracks the performance of local-currency debt issued by emerging-market governments, whose debt is accessible by most of the international investor base.

MSCI ACWI Index: The MSCI ACWI Index is a market-capitalization-weighted index composed of over 2,000 companies, and is representative of the market structure of 48 developed and emerging-market countries in North and South America, Europe, Africa and the Pacific Rim. The Index is calculated with net dividends reinvested in U.S. dollars.

MSCI ACWI ex-USA Index: The MSCI ACWI ex-USA Index includes both emerging-market countries and developed markets, excluding the U.S.

MSCI Canada Index: The MSCI Canada Index is a free float-adjusted market-capitalization-weighted index designed to measure the performance of the large- and mid-capitalization segments of the Canadian equities market.

MSCI Emerging Markets Index: The MSCI Emerging Markets Index is a free float-adjusted market-capitalization-weighted index designed to measure the performance of global emerging-market equities.

MSCI EMU Index: The MSCI EMU (European Economic and Monetary Union) Index is a market-cap weighted index that covers about 85% of the market capitalization of the EMU.

MSCI Frontier Markets Index: The MSCI Frontier Markets Index gauges large- and mid-cap stock performance in 29 frontier market countries.

MSCI Japan Index: The MSCI Japan Index is designed to measure the performance of the large- and mid-cap stocks in Japan.

MSCI United Kingdom Index: The MSCI United Kingdom Index is designed to measure the performance of large and mid-cap stocks in the U.K.

MSCI USA Index: The MSCI USA Index is designed to measure the performance of the large- and mid-cap segments of the U.S. market. With 632 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization in the U.S.

MSCI World Index: The MSCI World Index is a free float-adjusted market-capitalization-weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of 24 developed-market country indexes.

Personal Consumption Expenditures Price Index: The Personal Consumption Expenditures Price Index measures price changes in consumer goods and services.

Russell 1000 Index: The Russell 1000 Index includes 1,000 of the largest U.S. equity securities based on market cap and current index membership; it is used to measure the activity of the U.S. large-cap equity market.

Russell 1000 Growth Index: The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

Russell 1000 Value Index: The Russell 1000 Value Index measures the performance of the large-cap-value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values.

Russell 2000 Index: The Russell 2000 Index includes 2000 small-cap U.S. equity names and is used to measure the activity of the U.S. small-cap equity market.

S&P 500 Index: The S&P 500 Index is an unmanaged, market-weighted index that consists of 500 of the largest publicly-traded U.S. companies and is considered representative of the broad U.S. stock market.

Sterling Effective Exchange Rate Index: The sterling effective exchange rate index measures sterling’s value against a basket of currencies, accounting for changes in relative prices and purchasing power.

U.S. Dollar Index: The U.S. Dollar Index measures the value of the U.S. dollar in relation to a basket of U.S. trade partners’ currencies.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affiliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and the information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from qualified professionals. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based onassumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.