Emerging-markets equity: 2023 outlook

A strategic choice

While some investors tend to be overly bullish or bearish on events in emerging markets at any given time, particularly with regard to China, we believe emerging market equities are a strategic choice for diversified portfolios regardless of market conditions and we are reasonably optimistic going forward.

Current issues facing emerging-market equities

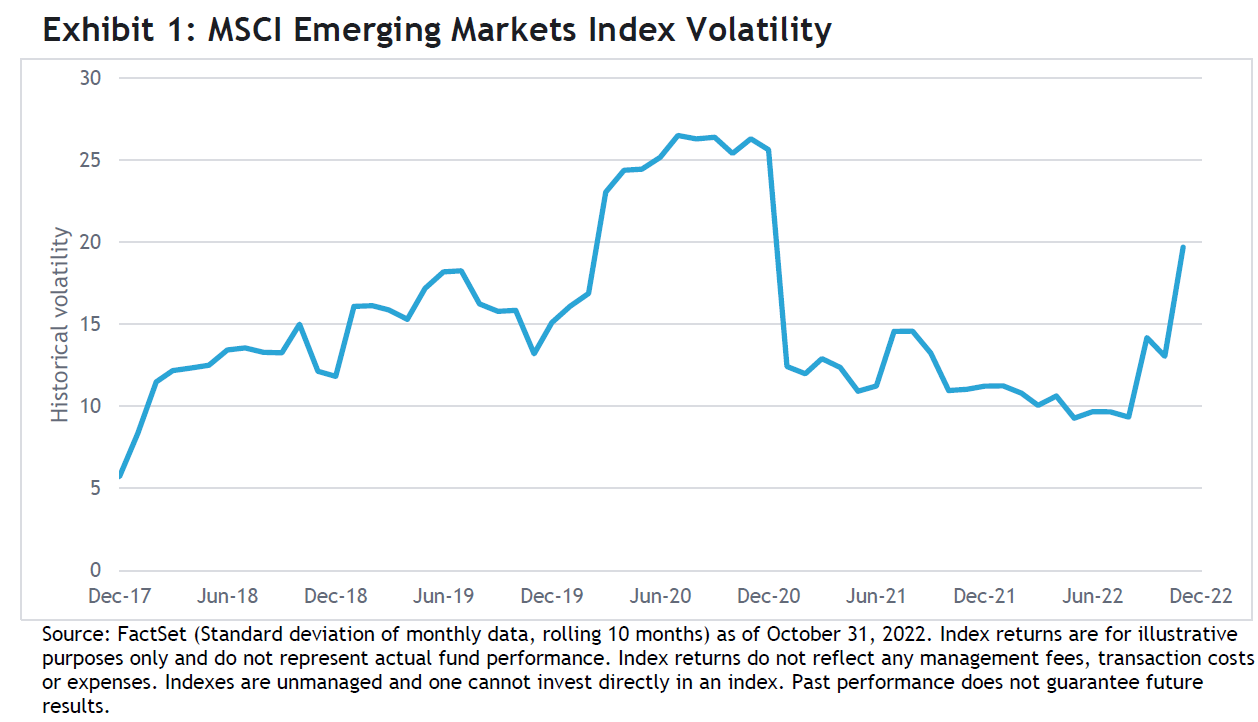

When investing in emerging markets, there always seems to be crisis somewhere in the world and even occasional systemic shocks. That noted, 2022 has been quite eventful as reflected by spike in market volatility.

This year’s turmoil started with Russia’s invasion of Ukraine, which led to the decimation of Russian stocks. This was followed by a second-quarter rally in Chinese stocks as stringent COVID-19 lockdowns there began to ease. Optimism was quickly dashed as a few new COVID-19 cases set in motion China’s “Zero COVID” policy—major cities were locked down, the economy was paralyzed, and consumer discretionary stocks plunged.

It was not just the domestic side of emerging-markets economies that faced challenges either; the outlook for exports has been just as gloomy. The expectation of a global demand slowdown triggered considerable declines in the stocks of global manufacturers. Even TSMC (Taiwanese Semiconductor Manufacturing Co.)—historically a bellwether of quality stocks—has lost roughly a third of its market value so far this year. As if these concerns were not enough, China is struggling with a whole host of issues that have led to foreign capital outflow of roughly US$8 billion just in October.

China, by far the largest country by market capitalization weight in the MSCI Emerging Markets Index, has a significant impact on emerging-markets performance. China’s index weight has slipped from about 40% of the index two years ago, to approximately 30% of the index at the time of this writing. Its poor performance relative to other emerging-markets countries has weighed on index performance. Beyond its direct weight on the index, China also has a disproportionally large impact on other emerging-markets countries due to its economic power with regard to tourism, consumption, and commodities.

Today, COVID-19 lockdowns, the global economic slowdown, foreign capital outflow, de-listing of Chinese tech stocks, and the meltdown in the China’s real estate sector are some of the most significant issues facing emerging markets. A close look at each of these areas provides insight into our perspective.

COVID-19 lockdowns in China

With recent announcement of easing on COVID restrictions, China is clearly preparing to open up without formally dropping its tough zero COVID policy. We believe the market has mostly anticipated this outcome—the MSCI China Free Index was up almost 30% (U.S. dollar terms) just in November—however, the pace of the easing may significantly drive not only the market, but sector and industry returns as well. Along the way, infections will likely surge and there might even be targeted lockdowns in some isolated locations, but we believe the government will stay the course with its decision to start living with COVID. If Hong Kong is any indication, the desire to reopen is clear, but needs to be balanced with the burden on local hospitals.

From an investor’s perspective, these uncertainties further add to the risks of Chinese stocks. One outcome that the market came away with from the 20th Party Congress was that the concentration of power within the government has become even stronger. With fewer opposing voices, and less check-and-balance, policies can become more extreme—hence the tail risks are higher than before. Investors hate tail risks, and therefore demand a higher risk premium (higher discount rates) to own these stocks, which has led to lower prices—even when considering the recent rally. Despite the enthusiasm and the stock market surge, investors should continue to approach Chinese stocks with caution.

Global slowdown

A global slowdown in developed markets will certainly have major impacts on industrial exporters, especially those in South Korea, China, and Taiwan. Yet, emerging markets are less dependent on exports than they were a couple of decades ago. Today the major economic exposures can generally by categorized into three main types—commodities, domestic consumption, and exports. China, for example with 1.4 billion people, has been aggressively developing its own economic ecosystem and diversifying its economy to reduce reliance on exports. India and Vietnam, with younger populations, have promising demographics for strong growth in domestic consumption. Countries with higher commodity exposures include most emerging markets in Latin America and the Middle East, along with South Africa, Indonesia, and Malaysia. While emerging-market economies are more diverse, and have evolved from decades ago when they were often strictly viewed as suppliers to developed countries, commodity prices and the ongoing recovery of domestic consumer sectors remain important drivers of the performance of emerging market stocks.

Foreign capital outflow

Rising U.S. interest rates typically have a negative effect on foreign capital flows into emerging markets. According to the Institute of International Finance (IIF), for the three months ending in October, net capital flow into emerging-markets equity was a positive US$14 billion, while China had a negative US$8 billion. This reflects the market concerns regarding China and the brighter prospects of emerging-markets countries outside of North Asia. India, for example, is benefitting not only from growth recovery, but also supply chain restructuring at the expense of China even though the process takes many years. Smaller countries such as Vietnam and Thailand are beneficiaries of the same theme, as the market expects further manufacturing capacity to shift from developed economies, particularly Germany. Chinese stocks seem to be the main source of emerging-markets capital outflows so far―a trend that looks encouraging for most other emerging-market regions, excluding North Asia.

De-listing of Chinese technology stocks

Despite much media attention, the negative impact of potential U.S. de-listing of Chinese stocks may be limited. De-listing from U.S. exchanges might drain liquidity as some U.S. investors have to withdraw, but it doesn’t change corporate fundamentals or choke off financing completely. Many investors will still be able to access the securities via non-U.S. exchanges, mostly likely in Hong Kong. From a company perspective, to hedge this uncertainty, many have already looked into alternatives or are pursuing dual listing (as Alibaba has done, for example).

For investors, the outcome of de-listing is difficult to forecast and risk remains real. The optimists often point to the on-going progress in the U.S./China audit agreement, conducted in Hong Kong, as a potential solution. Unfortunately, given the controlling behavior that both sides have exhibited in the past, we believe the probability that implementation will be free of major conflicts is low. It is also possible that some, but not all companies will get de-listed. Given the high profile nature of this issue, even if it happens, there should be a period of transition to help cushion the impact of lower liquidity.

Impact of Chinese real estate

Real estate is a significant sector for the Chinese economy, as it accounts for roughly 30% of gross domestic product (sources: CNBC). For home buyers, the biggest problem now is consumer confidence. Unlike other major countries, when a Chinese family buys a new apartment, it is usually in pre-construction, but full payment is required. However, safeguards regarding escrow are questionable, so most buyers have to trust the developers with their life-savings even before construction starts. Hence, when major developers default, consumer confidence plunges and takes a long time to heal.

To deal with this problem, the government has some levers. After all, the latest crisis started with new government regulations, aimed at strengthening the balance sheet quality of developers and reducing the risk of a housing bubble. Lack of demand does not appear to be a problem. Hence, if the government chooses to relax regulations and introduces support policies, the sector will likely respond positively, even though few would expect a return to the prior growth rate. Recently, because of valuations, more investors are starting to look at some of the highest-quality developers. As the Chinese real estate market continues to stabilize, incremental supportive policies are expected to be announced. In the future, an improved housing sector will not only help the Chinese economy, but also countries that supply commodities that support construction efforts. Latin America countries, for example, should benefit. We saw this in Brazil from 2003-2010 when President Lula of Brazil enjoyed a robust economy and strong popularity in part due to heavy Chinese demand for commodities at that time. It would be a coincidence if his recent return to the presidency aligns him with improving Chinese commodity demand again if China’s housing market recovers.

SEI’s Approach

Forecasting macroeconomic events, especially in China, has always been difficult. We believe there is no better way to mitigate these risks than diversification. SEI focuses on three distinct alpha sources—value, momentum, and quality—which have historically led to more consistent outperformance. We’re currently biased toward value stocks since they are generally attractive based on historical valuations, and re-opening trades tend to benefit them.

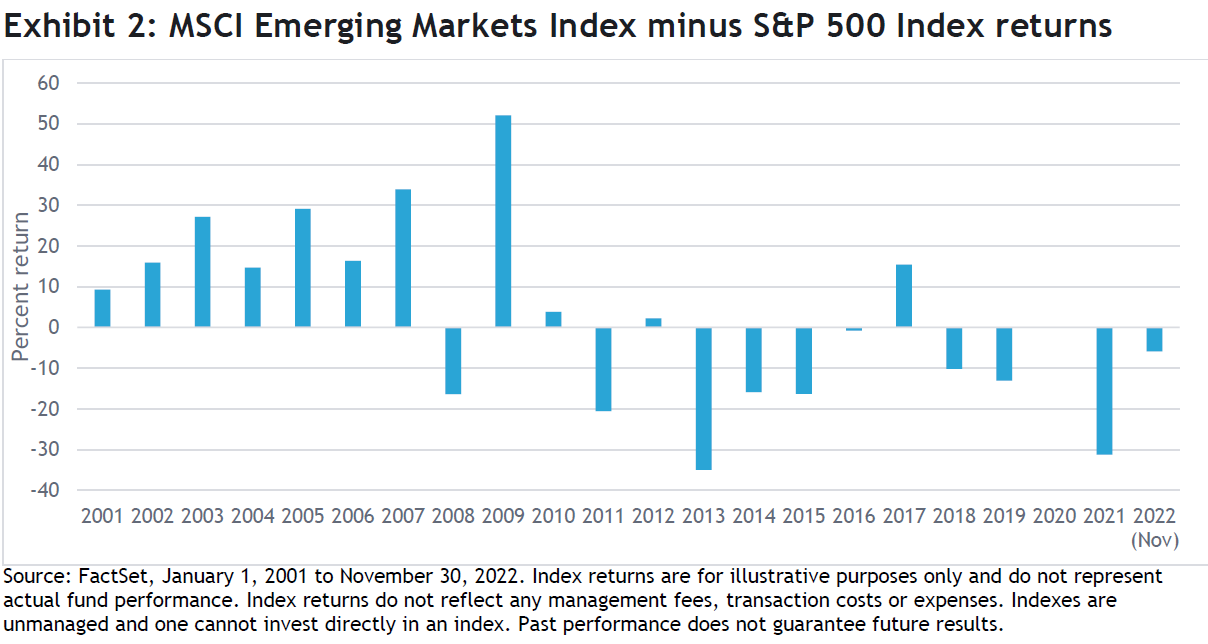

At an asset class level, emerging-markets stocks have lagged their U.S. peers in most of the past decade, and they are on track to trail again this year, even though the decade prior was the essentially the reverse (see Exhibit 2). The current cautious sentiment is mainly driven by numerous concerns facing emerging markets, and China in particular. However, investors have historically been rewarded by investing during times of uncertainty. Remember, as we move forward, equity returns don’t need economic or corporate earnings growth to turn positive, they only need conditions to be not as bad as where we are today. Given the current state of affairs, it doesn’t seem like a high bar, and we’re reasonably optimistic on emerging-markets equities.

Index definitions

The MSCI Emerging Markets Index is a free float-adjusted (i.e., including only shares that are available for public trading) market capitalization-weighted index that tracks the performance of emerging-market equities.

The MSCI China Free Index includes large and mid-cap Chinese companies. The index constituents include B shares, H shares, Red chips, P chips and foreign listed shares. Currently, the index includes Large Cap A and Mid Cap A shares represented at 20% of their free float adjusted market capitalization.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

Glossary of alpha sources

Alpha source: Alpha source is a term used by SEI as part of our internal classification system to categorize and evaluate investment managers in order to build diversified fund portfolios. An alpha source is the investment approach taken by an active investment manager in an effort to generate excess returns. Another way to define an alpha source is that it is the inefficiency that an active investment manager seeks to exploit in order to add value.

Momentum: A trend-following investment strategy that is based on acquiring assets with recent improvement in their price, earnings, or other relevant fundamentals.

Quality: A long-term buy and hold strategy that is based on acquiring assets with superior and stable profitability with high barriers of entry.

Security selection: An investment strategy that employs research and judgement to uncover individual opportunities that have been mispriced by other financial market participants.

Value: A mean-reverting investment strategy that is based on acquiring assets at a discount to their fair valuation.

Glossary of financial terms

Liquidity is the conversion of an asset into cash, with considerations to the impact of that transaction on a security’s price.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. Diversification may not protect against market risk.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law.