High-yield bonds: 2023 outlook

Default worries may be overblown

Historically, a U.S. recession has induced a significant number of defaults in the high-yield bond market. As the probability of a recession continues to rise, SEI believes high-yield bond default worries may be overblown. In our view, defaults should be kept in check by: a prior spike indefaults, record issuance in recent years, maturity management, and strong corporate fundamentals.

A neutral view in a challenged environment

High-yield bonds had a solid 2021, as they gained more than 5% (as measured by the ICE BofA US High Yield Constrained Index—USD Total Return) and notched three consecutive calendar years of gains. However, like most asset classes, 2022 has been a year of challenges with the asset class slumping more than 12% year to date through October 31, 2022. Persistently high inflation and the

corresponding tightening of monetary policies (dramatically higher interest rates and quantitative tightening) by central banks have presented formidable headwinds.

On the other hand, oil prices have eased, the U.S. job market remains robust and bond yields are moving higher—the latter of which is good news for investors seeking long-term income. The yield for the ICE BofA US High Yield Constrained index has risen more than 400 basis points (a basis equals 0.01%) and is now about 9%. In relative terms, high yield’s attractiveness versus investment-grade credit (those securities rated BBB or above) has improved, while the spread (the difference in yield between a non-government and a government bond of similar maturity) has increased significantly and now exceeds 450 basis points.

Will a recession induce a wave of defaults? We think not.

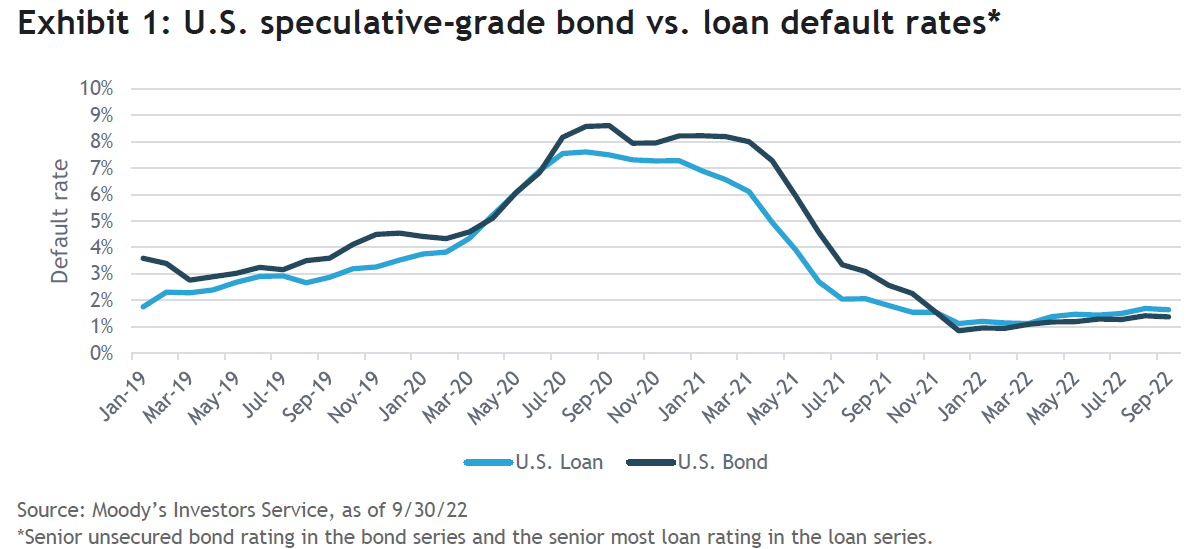

Predictions of a looming recession have continued to grow louder. Some pundits claim the U.S. is already in a recession, while other suggest it could happen later this year or in 2023. Regardless of timing, it’s only natural for high-yield investors to have concerns about increased default rates during a recession. As of September 2022, Moody’s U.S. Speculative Grade Default Rate was 1.5% which was the eleventh consecutive month below 2%—the first time that has happened since April 2007 through February 2008. The market anticipates a gradual rise in the default rate to 4.8% by September 2023—the average default rate for the past five and ten years was 4.1% and 3.7%, respectively.

In SEI’s view, there are four key components that will keep expected default rates in check:

- A previous spike in defaults

- Record high-yield issuance in 2020 and 2021

- Maturity management

- Strong corporate fundamentals

Previous spike in defaults

COVID-19 related shutdowns contributed to a spike in high-yield default rates in 2020 and 2021 as default rates reached nearly 9%. While it’s unlikely that all of these companies would have defaulted without the pressure of the pandemic, it undoubtedly brought forward a wave of defaults that cleared the runway a bit in the coming years. This is supported by the below average default rate since the latter half of 2021.

Record high yield issuance in 2020 and 2021

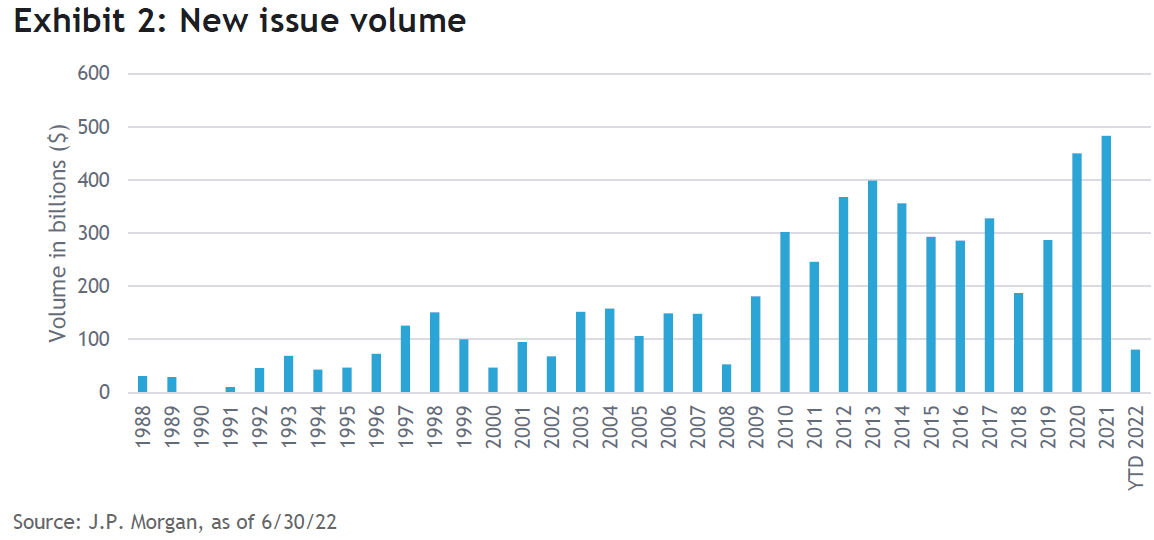

As liquidity improved in the middle of 2020, and given the anticipated uncertainty related to the pandemic, high-yield companies immediately began accessing the new-issue market to address both near-term and long-term financing needs. Historically, a $300 billion year of new issuance was considered a notable threshold, but that mindset was reset beginning in 2020. In 2020, $450 billion came to market exceeding $400 billion for the first time in a calendar year. In 2021, $483 billion came to market exceeding, $400 billion for the second consecutive year.

Maturity Management

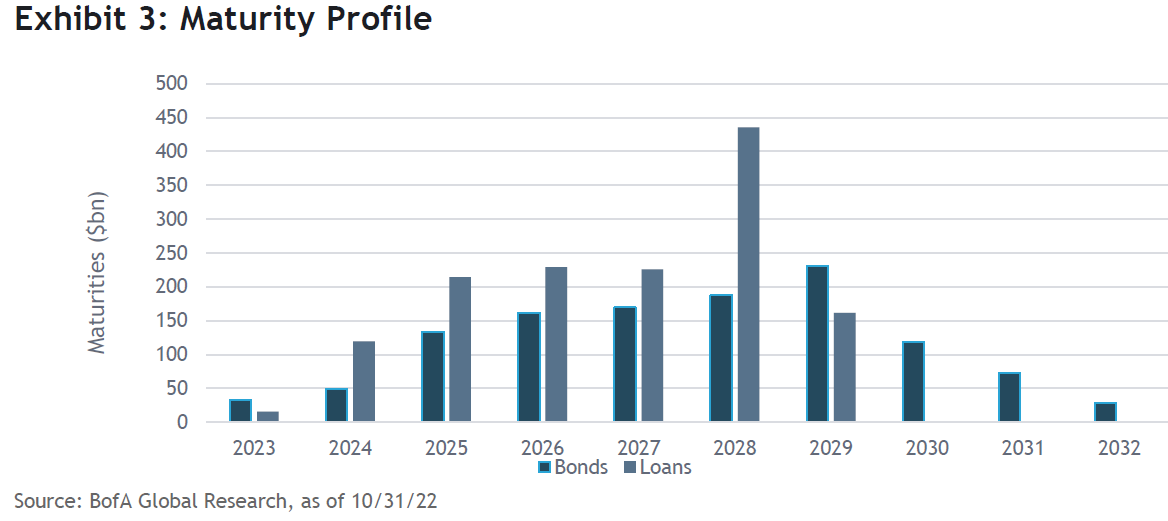

The combination of the previous spike in defaults and the record-setting high-yield issuance has resulted in a manageable amount of maturities in 2023. Looking ahead, most high-yield debt does not mature, as companies seek to refinance existing debt while extending maturities. As long as the primary market is functioning properly, SEI expects that trend to continue.

Strong corporate fundamentals

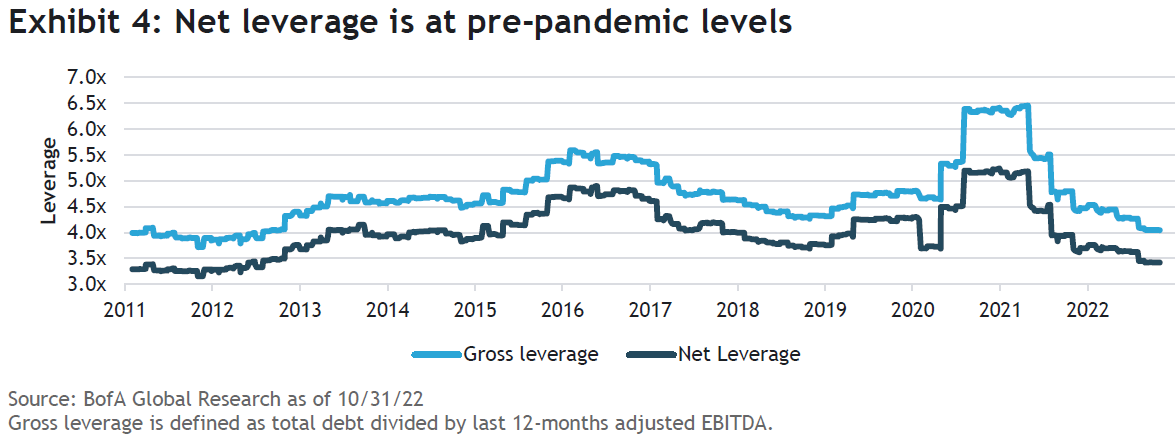

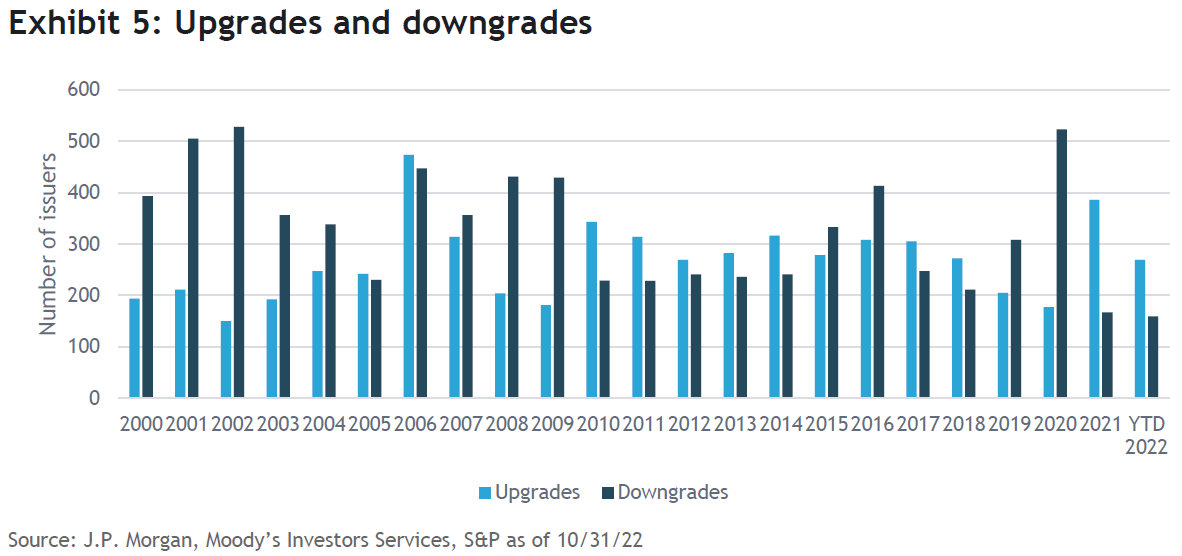

Net leverage is defined as net debt (total debt, less cash and cash equivalents) divided by last 12-months adjusted EBITDA (earnings before interest, taxes, depreciation and amortization). Given the uniqueness of the pandemic-related economic shutdowns, it was not surprising that net leverage exceeded the figures from the global financial crisis. However, that figure has come down sharply and the market is roughly in line with the historical averages. J.P. Morgan has identified two sectors that were severely impacted by the pandemic and continue to experience improvements in fundamentals, but are still inflating leverage: transportation (14.3x leverage) and gaming (11.6x). Overall net leverage is approaching near-term lows—if one were to exclude transportation and gaming from the calculation, net leverage would be even lower. In regards to corporate ratings, the number of ratings upgrades outpaced ratings downgrades through the end of June. While we have our doubts that this pace continues, if it did, this would be the first time since 2017 and 2018 that the market has experienced two consecutive years of upgrades exceeding downgrades.

Concerns remain, defaults aren’t one of them

We have mentioned several economic concerns including inflation, tighter central bank policy and the potential for a global recession. There is also the Russia-Ukraine war which has roiled commodity markets and still has the potential to expand and escalate. COVID-19, could mutate and cause further disruptions. The list of economic, geopolitical and pandemic concerns is long, and that doesn’t even include any surprise issues. Even though there are numerous concerns for high-yield, in SEI’s opinion, a material increase in default rates is not one of them. In terms of yield, yield spread and default rates, high-yield bonds are as attractive as they have been in some time, although given the overall state of the economy, inflation, and central bank action we hold relatively neutral outlook.

Index definitions

The ICE BofA US High Yield Constrained Index contains all securities in the ICE BofA US High Yield Index but caps exposure to individual issuers at 2%. The ICE BofA US High Yield Index tracks the performance of below-investment grade, U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI)

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law.