High-Yield Bonds: The Canary isn’t Choking

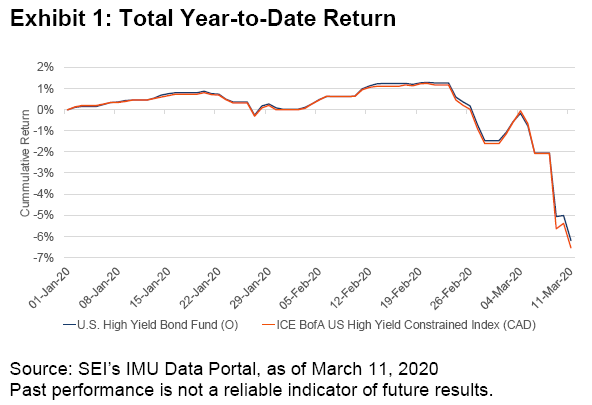

High-yield bonds are often thought of as the “canary in the coal mine” because trouble in high-yield markets can sometimes be an early warning signal for other asset classes. By most measures, high-yield bonds had held up fairly well only falling about 2% year-to-date through March 6. But as was the case with essentially all risk assets, losses in high-yield bonds accelerated dramatically on March 9. Although the high-yield canaries aren’t singing right now, they aren’t choking either.

Liquidity

Liquidity—which is generally lower for high yield than investment grade—has deteriorated, but not to the point where it has caused real issues. There is no new issuance this month and quotes are wide. Many high-yield funds, SEI included, appear to have cash to cover rising outflows. Exchange-traded funds and credit-default swaps have also been a source of funding for outflows, limiting the need to sell actual bonds. While these are all signs of stress, high-yield markets are still orderly and manageable. Outflows would really have to ramp up from here for our portfolios to become forced sellers.

Performance has been Diverse

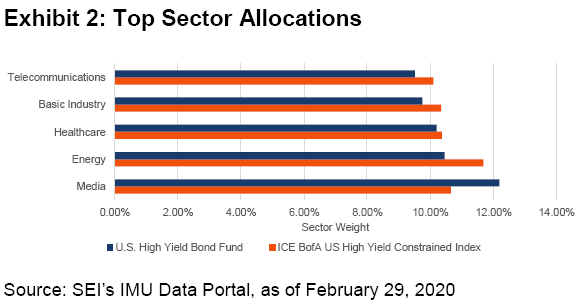

High-yield market performance has varied widely by sector, with energy suffering from reduced oil demand and a fierce battle for market share between Saudi Arabia and Russia, at the expense of prices.

Unsurprisingly, leisure has also fared poorly in a world of COVID-19-related quarantines and travel bans.

Conversely, telecommunications and healthcare (which are two larger high-yield sectors) along with bank loans (which are above bonds in the capital structure, and typically BB rated floating-rate instruments) have fared much better. This dynamic may persist for a bit.

High-yield spreads have moved considerably wider this year, some of which is deserved—particularly in the case of energy, where default risk has certainly risen. In other sectors, the spread widening has been more a case of “guilt by association.” We continue to cautiously look for opportunities, keeping in mind the lower levels of liquidity in high-yield markets and the potential for significant outflows if investors begin to panic.

Defaults and Downgrades

Defaults have been near historically low levels so there is certainly room for them to rise in a time of stress. There may be more “fallen angel” opportunities than usual if we see a number of downgrades of BBB rated securities. Sectors that are the most performance challenged right now, notably energy, are the most at risk for defaults and downgrades. Managers have indicated that they are looking to add risk, particularly in affected areas, when it makes sense.

Positioning and Outlook

We have not made any significant positioning changes to our high-yield portfolios. The bulk of assets, as always, are in higher rated B and BB rated issuers. Portfolios are diversified across sectors without taking major sectors bets, while allowing managers to focus on individual credit selection. Energy will likely remain challenged until oil prices normalize, but other sectors should fare better. We believe this dislocation may provide a buying opportunity to selectively add risk and remind investors that rash decisions to hastily sell based on short-term performance challenges often generate poor long-term results.

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.