Labor pains fuel inflation

Most central banks attempt to keep inflation to a relatively benign level of 2% to 3%, depending on the bank. But, recently, inflation has been running much hotter. Labor input costs are one of the most prominent drivers of inflation and, with worker participation levels softening (particularly for the working-age male cohort) and the swift ageing of populations in many major developed and emerging economies, we may see continued upward pressure on wages that help keep inflation higher for longer.

Tight labor markets

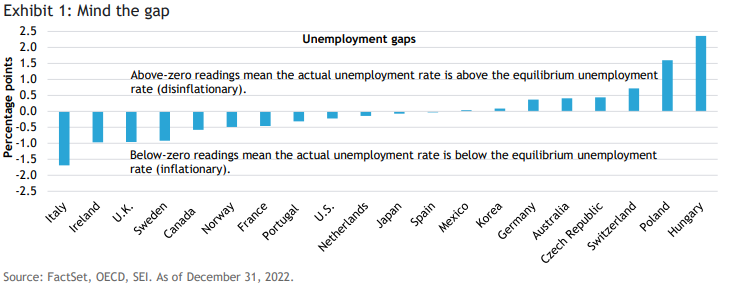

SEI has consistently predicted that inflation would be higher for longer since the spring of 2021. Our out-of-consensus call was based in part on the tight labor-market conditions that prevailed in the U.S., Canada, the U.K., and Europe. Exhibit 1 compares the so-called unemployment gap for various countries. This gap represents the difference between the actual unemployment rate and a measure of the “equilibrium” unemployment rate, also known as the non-accelerating inflation rate of unemployment (NAIRU) as measured by the Organisation for Economic Co-operation (OECD). The NAIRU statistic is a theoretical construct representing the lowest unemployment rate that can be sustained without causing wage growth and inflation to rise. The chart shows that currently reported unemployment rates are at or below long-term equilibrium levels for many countries. This implies labor markets are extremely tight and wage growth is likely to remain higher-than-desired, putting continued upward pressure on inflation.

The long-term equilibrium rate of unemployment is not directly observable and changes over time. Globalization, demographic shifts, productivity trends, workforce skills, and employee bargaining power are some of the many drivers behind changes in the NAIRU. The equilibrium unemployment rate has tended to decline in recent decades, allowing the measured unemployment rate to fall to lower levels without causing inflation to rise. But actual unemployment rates for many countries have declined sharply in the aftermath of the pandemic at a time when participation in the labor force has fallen and the working-age population has contracted.

Where are the workers?

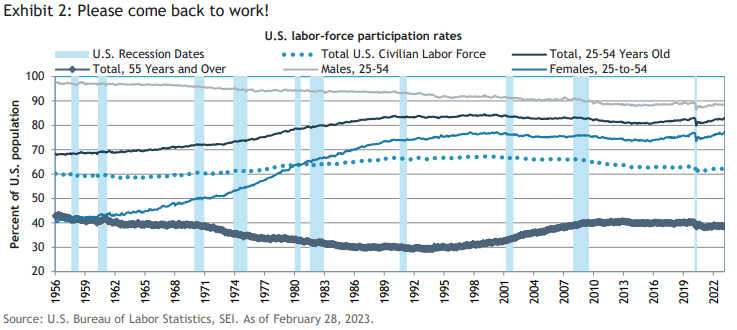

In the U.S., the retirement of the baby boomers alone has resulted in a 1.8% drop in the labor force. Most of those retirees will never come back. The pandemic sped up the boomers’ exit from the workforce, but it also caused some in younger cohorts to drop out, at least temporarily, owing to a reluctance to engage in public-facing occupations or deal with longer-running health issues. Quality-of-life considerations have also come into play. Exhibit 2 shows the trends in U.S. labor-force participation over time.

Perhaps even more important than the inevitable retirement of the boomers is the steady withdrawal of prime-aged males from the workforce. This has been a long-term trend dating to the 1960s, but it picked up pace in the 1990s as globalization caused the hollowing out of Middle America and the ushering in of the social dysfunction that plagues many areas to this day. A sobering statistic: Men without a college degree born in 1991 and 1992 have participation rates currently that are six percentage points lower than that of workers born in the late 1960s with the same educational level when they were at the same age during the 1990s.1

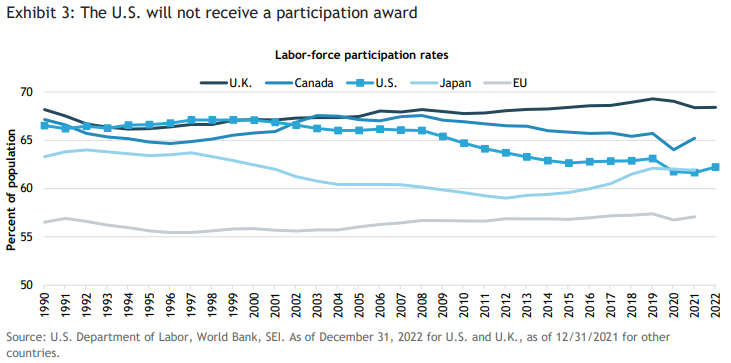

Exhibit 3 compares labor-force participation rates on an international basis. The U.S. has sustained the sharpest decline since the early 2000s, followed by Canada. The U.K. actually has recorded an increasing trend since the 1990s, as has labor-force participation in the EU and the euro area. This is partially the result of strong labor flows sparked by the expansion of the EU into central and Eastern Europe following the collapse of the Soviet Union. This permitted the unimpeded flow of migrants from the newly liberated eastern European countries westward. Japan also has registered a particularly sharp rise in participation in recent years because more women have entered the labor force at a time when the country’s population (the denominator of the laborforce participation rate) is contracting.

COVID-19 put downward pressure on participation rates everywhere, but most countries are now reverting to pre-pandemic trends and levels. This should alleviate some of the pressure on labor markets in the short term, especially if there is an economic recession that reduces the demand for labor. However, this is likely to be just a cyclical phenomenon. We’re calling it “transitory disinflation.”

Aging (un)gracefully

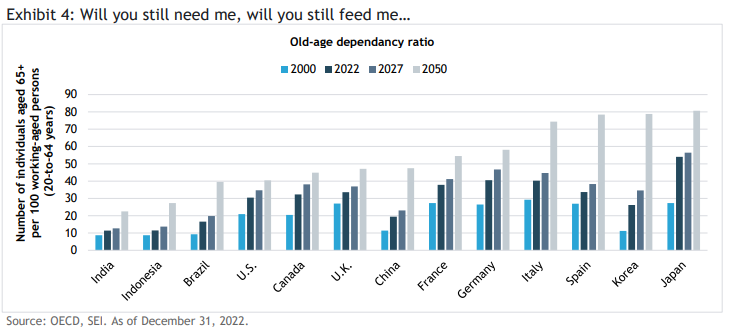

In the longer run, over the next several decades, many countries will see a structural decline in their prime-age populations. The result will be a shrinking supply of workers to support an aging population. Exhibit 4 tracks the dismal trend in the old-age dependency ratio for several major developed and developing countries. This ratio measures the number of individuals aged 65 and over per 100 people of working age, defined as persons 20 to 64 years old.

India and Indonesia have relatively young populations and low dependency ratios, currently amounting to a little over 10 individuals aged 65-plus per 100 working-aged persons. But even those two developing countries will likely see more than a doubling of the ratio by 2050. Other countries are in much worse shape already. Japan, of course, is already an old country. Its total population is contracting and the dependency ratio has hit 54%; by 2050, the ratio is expected to exceed 80 per 100 workingaged persons. They will require a significant number of immigrants and robots to handle all those elderly people. Italy, Spain, and Korea will not be too far away from Japan at that point. Indeed, Italy’s ratio is already at 40, the same level as Germany (without the latter’s economic and financial strength).

Among developed countries, the U.S. currently has a modest advantage versus Canada and the U.K. and an even larger one versus its European counterparts. This advantage will become even more significant in the decades ahead. By 2050, the U.S. old-age dependency ratio is projected to climb to 40. That is high enough to cause fiscal problems, but it doesn’t compare to the challenges facing Europe and the big economies of East Asia. That includes China. Its population is now aging rapidly. In 27 years, it will likely be supporting 57 elderly persons for every 100 working aged individuals. By comparison, the ratio today is estimated at just 19%.

The developed countries, of course, are better positioned to handle the fiscal and economic strains that lay ahead than those still in the developing stage. The level of social cohesion is also an important consideration. Asia may be better in this regard. France is already undergoing a nationwide series of strikes over the pension issue. President Macron’s efforts to raise the retirement age from 62 to 64 by 2030 have sparked the most extensive industrial action since the “yellow vests” protests in 2018. Mr. Macron recently survived a vote of no confidence sparked by his reforms.

The French experience highlights the fact that the demographic time bomb is already ticking, and governments need to address the problem sooner rather than later. In the U.S., the Congressional Budget Office projects the assets for the combined Old Age, Survivors Insurance, and Disability Insurance trust funds will be insufficient to cover the shortfall between projected revenues and spending as early as 2033. For the Medicare Hospital Insurance (Part A) trust fund, the net balance of the fund is expected to turn negative in 2028. Unfortunately, both political parties are unwilling to address the problem seriously. President Biden’s proposal to raise the Medicare surtax to 5% on individuals earning over $400,000 will not suffice after a few years. Of course, even this measure has little chance of being passed through a divided Congress, relying as it does solely on tax increases unaccompanied by benefit and eligibility reforms.

In the absence of substantive reforms, these mandatory spending programs will need to be covered out of general federal government revenue transfers and steep increases in Social Security and Medicare payroll taxes. Draconian cuts in old-age benefits are simply a non-starter, given the political power of the Baby Boomer generation and the devastating economic impact it would have on aggregate demand.

Fuel remains to fire up inflation

History tells us economic conditions are always cyclical and, as such, the labor pains that are helping push inflation will ease. The question is when. Obviously, central bankers and politicians are wishing for a swift end to elevated inflation; however, despite quantitative tightening (the selling of assets by central banks) and a dramatic rate-hiking cycle that is likely nearing an end, labor pains may persist until an economic recession fully takes root. Still, even the bitter pill of a recession won’t alleviate all pressure from the labor market, as population aging can’t be reversed by economic distress. At SEI, while we believe that a recession is likely, we expect it will be relatively shallow and brief. Unfortunately, at least some labor pains may outlive a recession.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL. SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755- 1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorized and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.