Quarterly Economic Outlook: Canada: Through the worst of it ?

For North America’s national soccer teams, the World Cup has sadly come and gone. That’s too bad, not least because “Canada is through!” would have made for a catchy and somewhat - controversial title.

In recent years, there have been stretches where observers worried that the Canadian economy was indeed “through” in the negative sense of the word (recession), due to its household -debt overhang, high unemployment, real estate worries and trade wars. While the “econo” bears finally got their technical recession (sort of), thanks to negative and flat economic growth in the fourth quarter of 2025 and first quarter of 2026, respectively, it looks to us like the Canadian economy is actually through the worst o f its post -COVID - era difficulties.

Challenges remain, and SEI is not calling for a rapid acceleration of growth, but we do expect steady improvements in numerous economic measures by 2027 if not sooner.

The recession that was…or was it?

There is widespread agreement that the Canadian economy has struggled in recent years and quarters — the most recent string of quarterly gross domestic product ( GDP ) data confirmed it. However, those reports , especially the first quarter of 2026 , were not quite as bad as headlines suggested. Business investment remain ed weak (outside of inventory additions), but consumers proved resilient and manufacturing continued to show positive momentum. While net exports detracted, this was due to strong imports rather than a sudden decline in trade activity. Finally, a modest population decline across both quarters contributed to the weak GDP prints, while per capita growth remained positive — an encouraging sign that argues against the economy having fallen (or falling) into recession.

Better days ahead

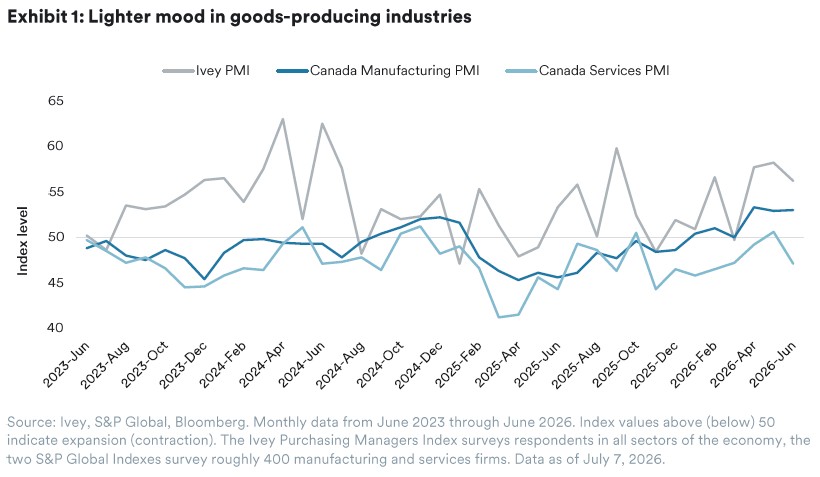

Although services sentiment turned down in June, survey respondents in other industries indicated that business activity has continued to pick up, especially in goods-producing areas of the economy, as shown in Exhibit 1.

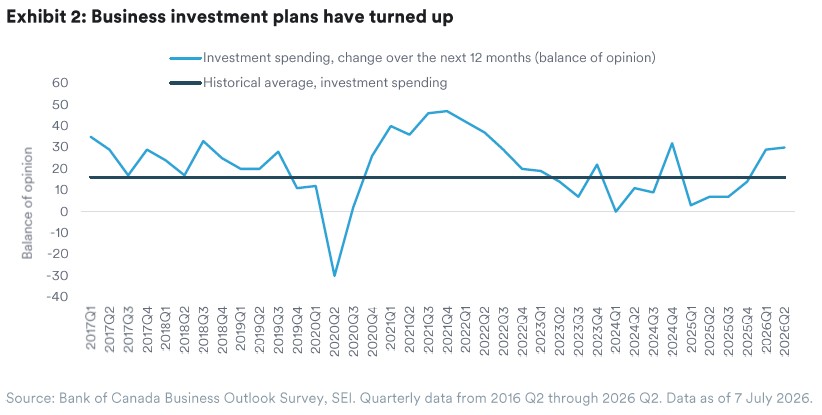

Low levels of business investment have been a challenge for the Canadian economy for several years. Encouragingly, the Bank of Canada’s (BOC) most recent Business Outlook Survey (BOS), conducted in May 2026, found that the number of businesses planning to increase investment has continued to pick up and is now running well above its long-term average, as shown in Exhibit 2.

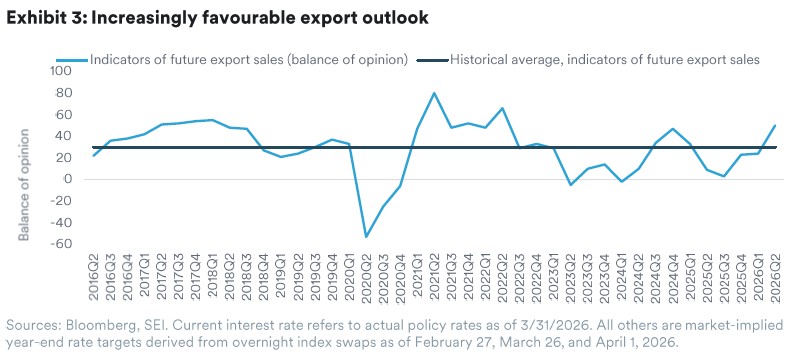

The BOS also found that respondents had an increasingly favourable outlook for exports. As we’ve noted previously, growing exports can help a country reduce domestic debt levels over time which is particularly relevant to Canada right now. The BOS was conducted in May, when the Strait of Hormuz situation was much cloudier and energy prices were much higher, so we won’t be surprised to see some volatility in these areas in future BOS surveys. That said, these indicators coincide with a notable global upturn in manufacturing activity and outlooks, so this does not appear to be a narrow, energy-only story. Furthermore, the commodity shortages caused by the Strait of Hormuz closure will require replenishment of above-ground supplies. As a result, we do not expect sharply lower energy prices (which have rebounded recently on renewed frictions between Iran and the U.S.) to undermine these dynamics significantly.

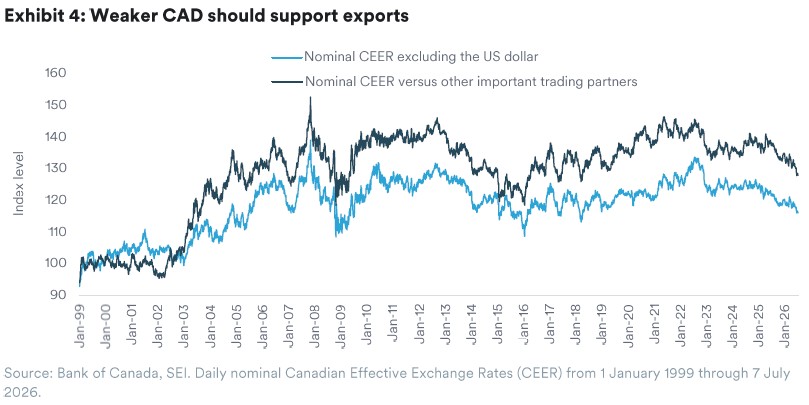

The Canadian dollar has been under pressure in recent years due to the low-growth, relatively low-interest rate domestic environment compared to the rest of the world. While most currencies have weakened against the U.S. dollar recently, the loonie has been weakening against a broad range of other currencies as well, as shown in Exhibit 4. This reduces import purchasing power and the spending power of Canadian tourists, but there are some beneficial trade-offs when it comes to trade. A weaker CAD against a backdrop of improving export prospects should be a powerful combination in support of both domestic growth and income.

Other considerations that support our optimistic outlook for Canada include relatively tame core inflation measures that are likely to remain within the BOC’s desired range of one-to-three percent, a lower risk of tightening monetary policy as a result (compared to economies where inflation is running persistently above targets and threatening to rise further), and a solid pipeline of national government expenditures focused on infrastructure, military investment, and greater energy and trade resilience.

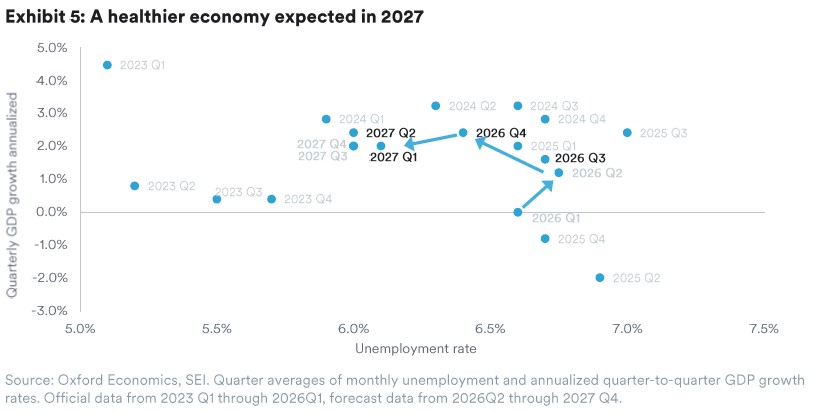

A healthier economy in 2027?

The dynamics we’ve outlined put us in agreement with numerous other forecasters who are projecting a stronger economic environment in Canada in the next year-and-a-half. Exhibit 5, which includes GDP and unemployment rate estimates from Oxford Economics, depicts how this more favourable environment could unfold as we move through the rest of 2026 and 2027. If unemployment holds steady or falls further, the trajectory will likely look even better

Risks to the outlook

Of course, a stronger economy is not guaranteed. Risks to our outlook include negative surprises on trade, inflation, interest rates, the AI buildout, and geopolitics. Among those, the status of the Canada-United States-Mexico Agreement (CUSMA) is a clear and present risk. The U.S. recently denied Canada’s formal request for a 16-year renewal which triggers a series of annual reviews and potential annual renegotiations until the agreement sunsets in 2036. This essentially kicks the can down the road with an overall effective U.S. tariff rate in the single digits—not ideal for Canada (or Mexico), but far from a worst-case outcome. That doesn’t rule out future trade frictions with a sometimes-mercurial U.S. administration, and it’s important to remember that CUSMA’s Article 34.6 allows any of the three countries to withdraw unilaterally six months after providing written notice. But for now, CUSMA looks set to continue in something like its current form for the next decade or so which, though imperfect, provides at least a measure of stability on the trade front.

The upshot for investors

As we like to remind investors, financial market behavior doesn’t neatly follow economic cycles—something that Canadian markets’ solid performance over recent years confirms. However, an improved domestic growth environment (and a strong external-growth environment) should lend further support to corporate performance within Canada, possibly with a lower degree of bond market volatility than in a number of other countries. A diversified global portfolio should benefit (albeit with periodic volatility) from exposure to the global AI buildout, as well as older-economy sectors that stand to benefit from it, industries that may benefit from eventual AI-driven productivity enhancements, undervalued areas that stand apart from the AI-investment wave, and, where relevant, exporters and non-currency-hedged positions that should benefit from a weaker loonie.

Glossary and index definitions

For financial term and index definitions, please see: https://www.seic.com/ent/imu-communications-financial-glossary

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.