Quarterly Economic Outlook : A clearer picture, unfortunately

Fortunately, the confusing array of cross-currents in the Canadian economy have cleared up a bit. Unfortunately, the economy appears headed for a slowdown and perhaps outright recession. While we do not expect a downturn to be especially deep or painful, it remains to be seen how long it could persist and what effects it may have on Bank of Canada (BoC) policy, government finances, and the Canadian dollar.

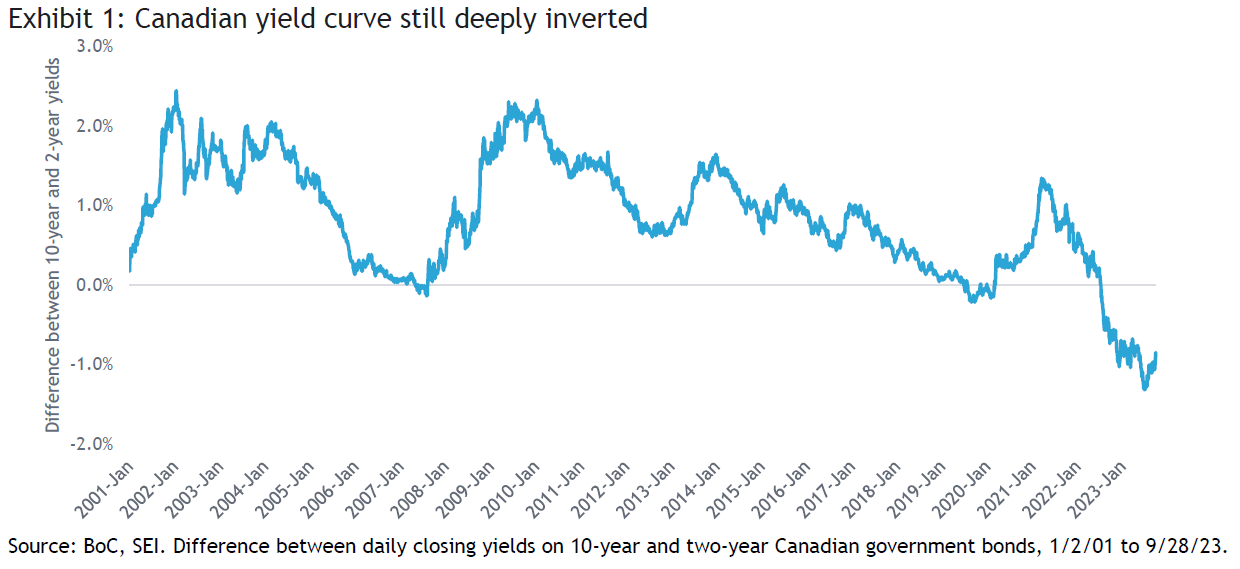

In our second-quarter outlook, we pointed to some of the cross-currents that were making it difficult to discern the likely direction of the Canadian economy. Fortunately, three additional months of data have made the outlook a bit clearer. Unfortunately, it looks like the economy could enter a challenging period in the quarters ahead. After a respite in the second quarter, the bond market (like those in many advanced economies) was challenged once again. The Canadian yield curve remained deeply inverted, as shown in Exhibit 1. While the degree of inversion eased somewhat, the difference between 10- and two-year yields is still well below historical norms. And while data limitations don’t allow us to infer much about a potential recession from this curve inversion, evidence from the U.S. indicates that a long period of inversion could correspond to a longer period of slow growth or recession. That being said, SEI expects any downturn to be relatively mild barring any negative surprises. A likely scenario in the coming year or two could be a so-called rolling recession that meaningfully impacts certain sectors and industries at any given time without dragging the overall economy into a ditch.

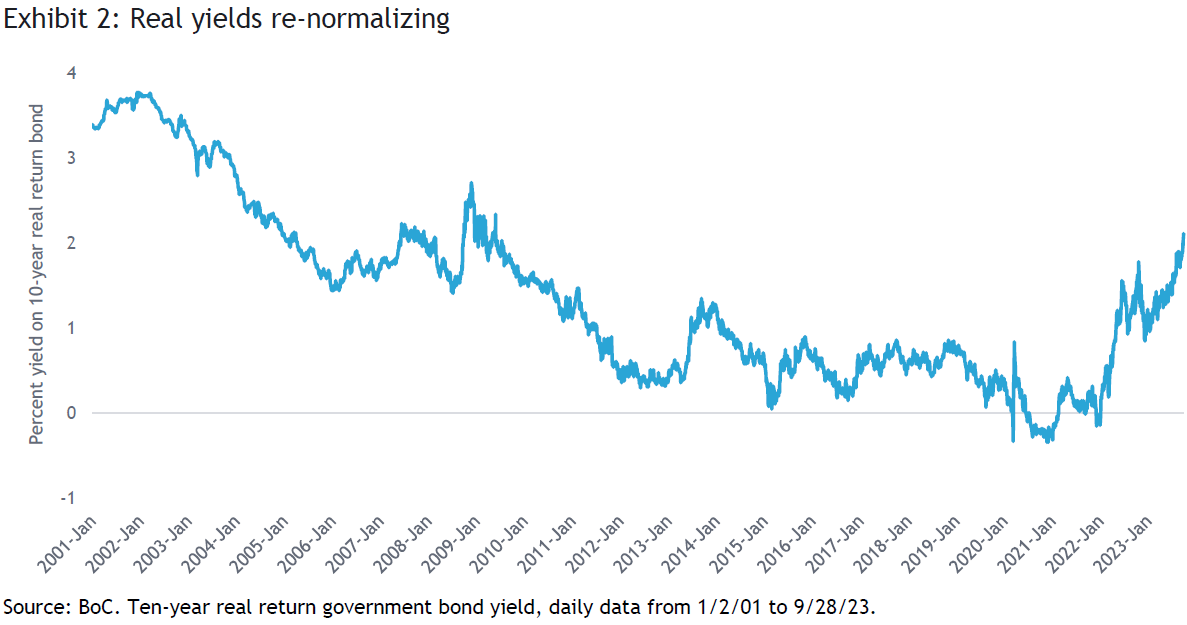

Interestingly, the bond market selloff this quarter involved a “bear steepening,” where the yield curve shifts upwards and longer-term yields rise more than shorter-term yields. This reflected markets and central banks coming around to our view that inflation would likely prove more stubborn than expected and, therefore, interest rates would need to stay higher for longer. Another notable feature of third-quarter bond market performance was the continued rise in real yields, which reflect the expected after-inflation yield demanded by investors. As Exhibit 2 shows, the 10-year Canadian real yield has now returned to levels that haven’t been seen since the global financial crisis of 2008-2009.

With bond yields rising globally (and by definition, valuations falling), many observers are concerned about the return of “bond vigilantes” disciplining profligate central governments by demanding higher and higher yields. We’ve certainly seen increasing strike activity by workers in many countries and sectors; why not a buyers’ strike in bond markets?

Canada certainly isn’t immune to worries about government deficits and debt levels. While the Trudeau government is now seeking to reduce government spending by just over $14 billion in the next five years, the bulk of those cuts are likely to take effect in the later years. This, along with challenging demographics and global supply-chain reconfiguration, could keep inflation from returning to the BoC’s longstanding target of 2% any time soon, barring a more-severe-than-expected recession.

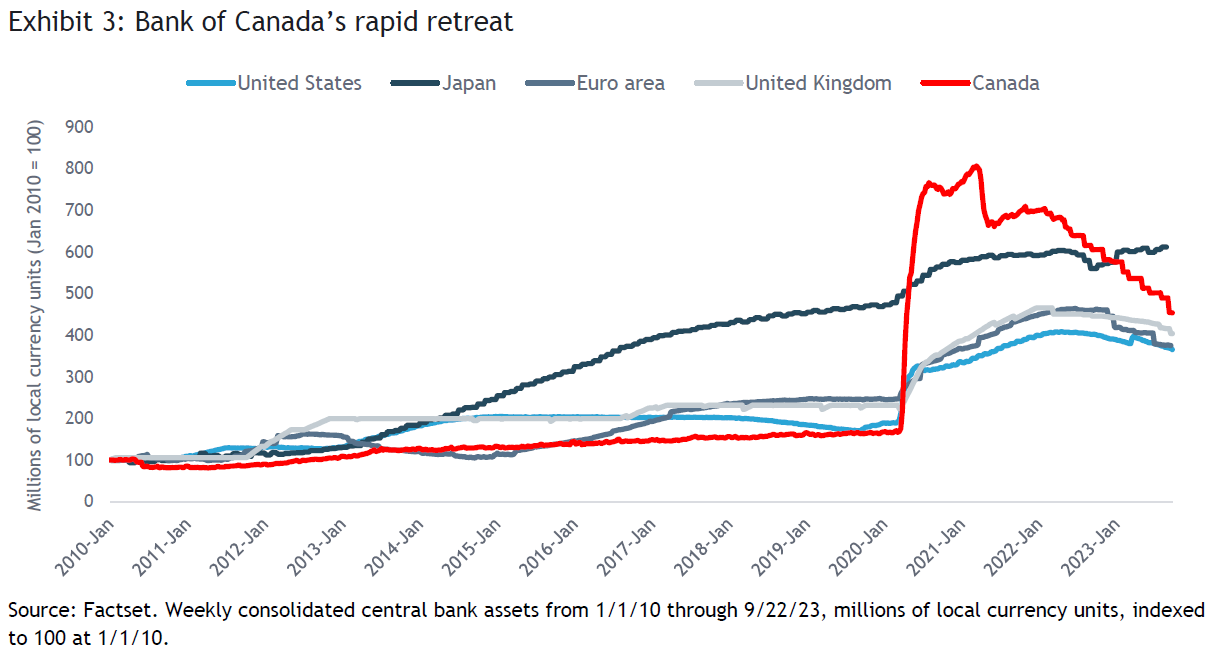

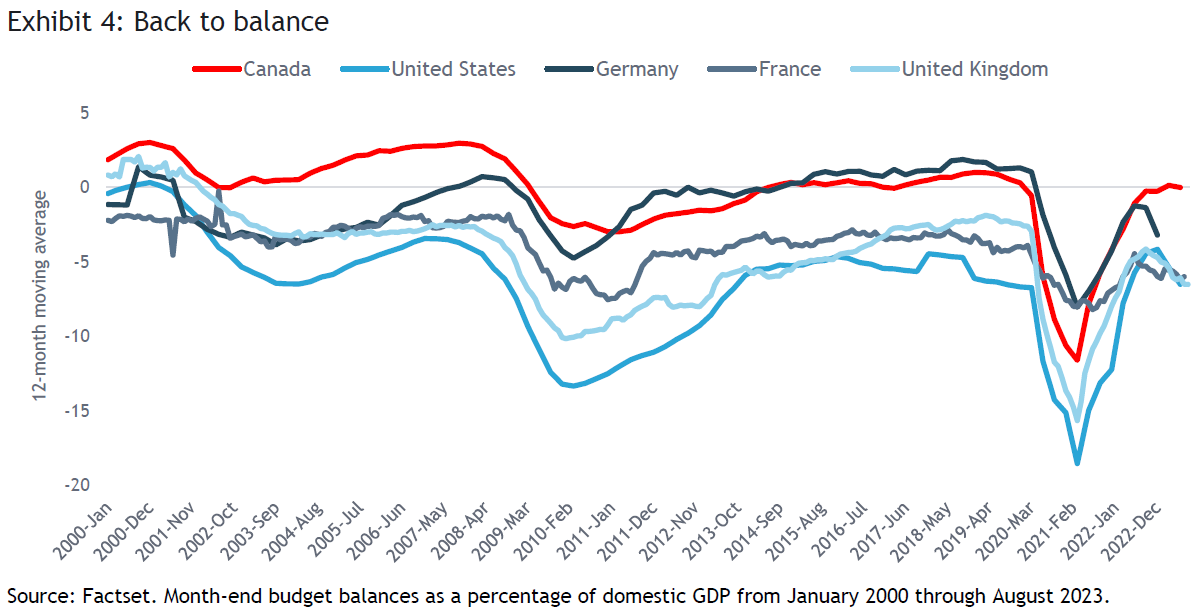

Despite these worries, it’s interesting to note that on both the fiscal and monetary fronts, Canada appears to have made more progress than many of its fellow G7 members. Exhibit 3 shows how quickly the BoC has retreated from its initial foray (spurred by COVID-19) into quantitative easing (the purchasing of government bonds by a central bank in an effort to lower interest rates), while Exhibit 4 shows that Canada’s central government budget position is actually much closer to balance than many of its G7 counterparts.

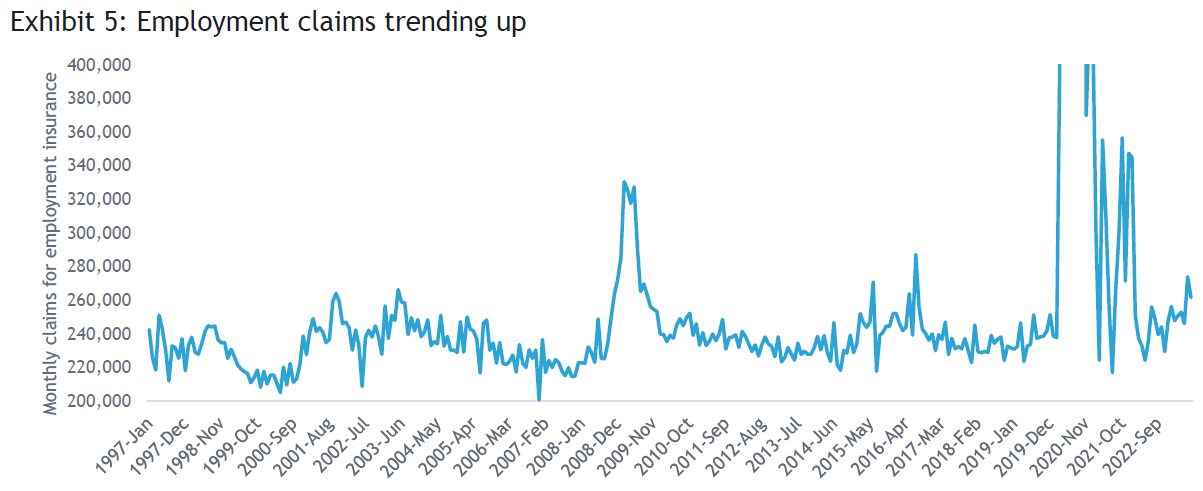

Whether these trends can continue remains to be seen. Housing and manufacturing activity is still in the doldrums, leading economic indicators are still depressed, and there appear to be some early signs of labour-market deterioration, as shown in Exhibit 5. Depending on the depth and duration of any economic slowdown or downturn, both the BoC and the Canadian government might need to pause or even reverse course.

Source: Statistics Canada. Monthly new and continuing claimants from January 1997 through July 2023. No data from March 2020 through September 2020 due to COVID-19 impacts. The vertical y-axis was shortened in order to make recent trend more visible. October 2020 claims were 1.6 million, December 2020 426,000, and January 2021 427,000.

However, if the rebound in commodity prices causes inflation to reaccelerate (See, for example, SEI Chief Market Strategist Jim Solloway’s July 2023 commentary, “Commodities set to keep inflation hot.”), or if the labour market manages to remain tight, that could constrain the BoC’s ability to cut interest rates. And with household balance sheets still extended, there is not a lot of room for private sector credit expansion to support the economy. Therefore, any downturn could bring central government finances under pressure once again.

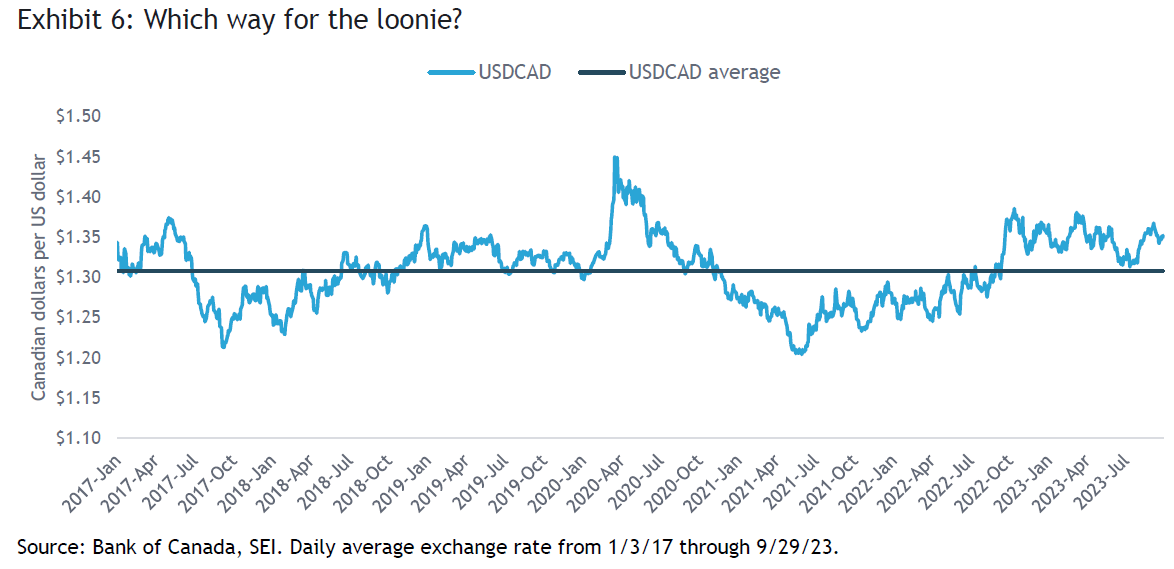

With this outlook, some of the strongest cross-currents in the quarters ahead might relate to the Canadian dollar. For example, tighter fiscal and monetary policies, as well as close ties to a still-strong U.S. economy, should be supportive, while a deeper-than-expected downturn and/or renewed deterioration of the government’s finances (holding all else outside the country equal) could pressure the loonie. At the same time, if energy commodity prices remain elevated, that could be favourable for the currency given Canada’s position as a net exporter of such goods.

For investors, SEI believes that diversification remains key. Although nothing is guaranteed in financial markets, in an environment of higher interest rates and bond yields, long-term returns on riskier assets should be higher as well; and hopefully this will prove true for inflation-adjusted returns on diversified portfolios. It’s why investors assume the risk of investing after all.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.