Quarterly Economic Outlook : Fasten your seat belts.

The Canadian economy continues to face significant but not insurmountable challenges. While persistently high inflation remains a substantial concern, recent reports have shown improvements. With this, and following a significant Bank of Canada interest rate hiking cycle, the odds of a recession have increased. Even though SEI believes any recession is likely to be fairly moderate, investors should probably keep their seat belts fastened.

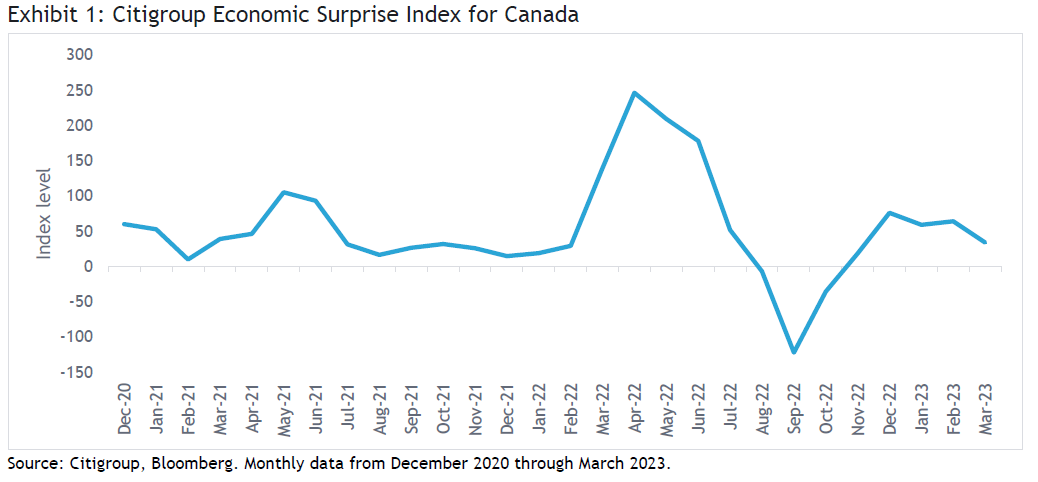

We observed at the start of 2023 that “the challenges facing Canada’s economy are significant but not insurmountable,” and that still seems to hold true at the start of the second quarter. While there are certainly challenges, there’s been some good news as well, and economic data on balance has been surprising to the upside since November 2022, as shown in Exhibit 1.

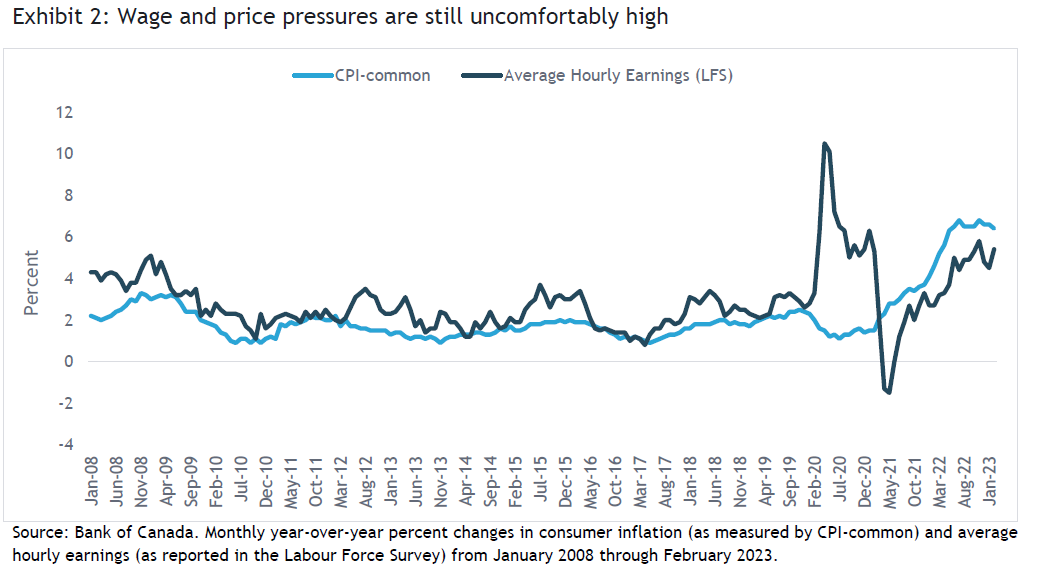

In fact, some of the challenges facing the Bank of Canada (BoC) and the domestic economy arise from what is essentially good news. The prime example, depicted in Exhibit 2, remains the challenge of still-high inflation associated with a historically low unemployment rate.

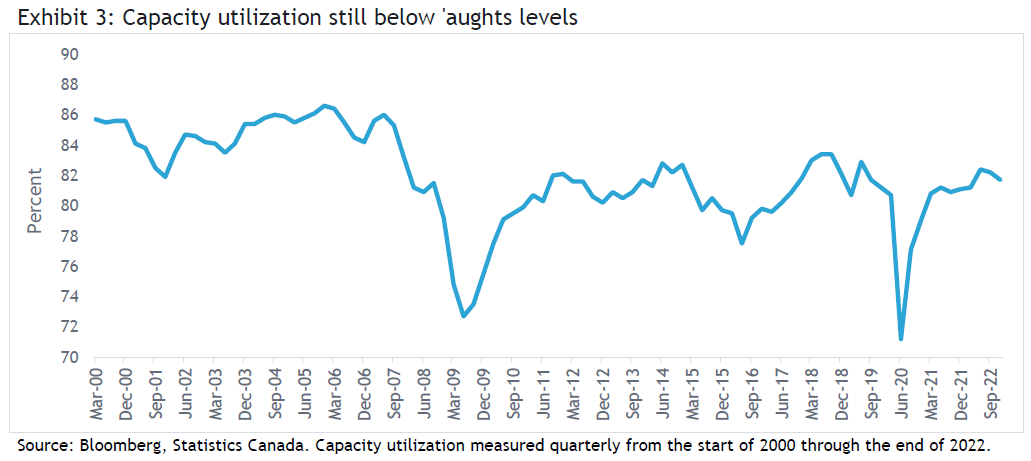

Another key challenge is productivity growth, a critically important tool in the fight to lower inflation. Unfortunately, productivity has actually been falling since the second half of 2020 and is flat relative to where it was at the end of 2018. While lagging productivity can be a normal feature of tightening labour markets, it’s not clear from the latest gross domestic product (GDP) report that business investment is going to be sufficient to meet the challenge. Perhaps this isn’t surprising given that capacity utilization, as shown in Exhibit 3, is still several percentage points below the level that prevailed before the global financial crisis of 2008 and 2009.

Finally, we also noted in January that “If the BoC is able to get inflation under some semblance of control, and if economists’ projections of a shallow, two-quarter recession prove accurate, we may hear plenty of talk about a ‘technical’ or ‘rolling’ recession in 2023 or early 2024 without much in the way of serious or lasting economic damage. That’s the hope anyways.” That remains the hope as we enter the second quarter, and we have yet to see clear-cut indications of a recession taking hold (first-quarter GDP will not be reported until the end of May).

While inflation is still uncomfortably high on a year-over-year basis, month-over-month readings are a bit more encouraging, and producer price pressures, though volatile, have been easing. Of course, how recently announced production cuts from the Organization of the Petroleum Exporting Countries plus Russia (OPEC+) impact this remains to be seen.

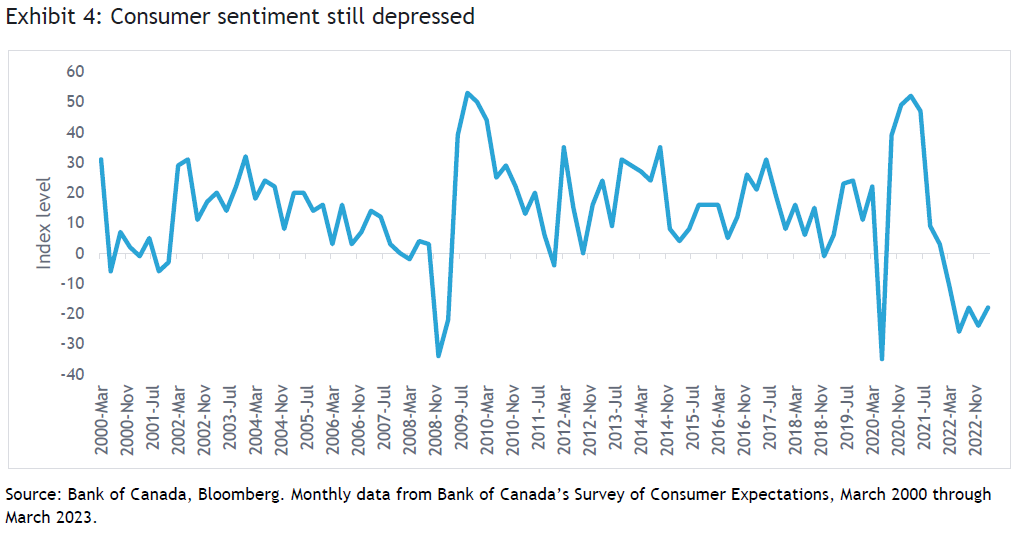

Business and consumer sentiment reports have been quite mixed. Household sentiment is still largely depressed, as seen in Exhibit 4, although this isn’t squared easily with healthy consumer activity of recent months and quarters. There’s no denying that 2022 was a very difficult year for the housing market, but recent trends in sales and permits have shown improvement while construction starts are still above pre-COVID-19 levels despite worries about high mortgage balances adjusting to higher interest rates. At least one bank CEO believes that mortgage support measures should prove sustainable and effective.1 Of course, we don’t yet know how the recent banking system paroxysms in the U.S. will impact Canadian banks, but it’s something economic and market observers will be keeping a close eye on. As for business sentiment, it has seemed weakest among manufacturers of late, although full-year views of sales activity and hiring plans are still relatively optimistic, according to S&P Global.2

Facing all of these cross-currents and uncertainties, the BoC remained on hold in March after raising 0.25% at its January meeting. Like many advanced-economy central banks, the BoC has promised to maintain higher rate target for as long as needed to get inflation to more acceptable levels. However—and this is the case for many developed market central banks—markets aren’t completely buying it. Rate markets are currently pricing in a BoC interest rate-cutting cycle from the middle of 2023 through the end of 2024. Given that U.S. Federal Reserve (Fed) finds itself in a similar situation, the loonie has been largely range-bound against the U.S. dollar since late 2022.

Of course, Canada’s outlook will also be influenced by the global economic environment, where additional cross currents and uncertainties are very much at play. Investors should keep their seat belts fastened.

Index definitions

The Citigroup Economic Surprise Index measures the degree to which economic data is beating or missing estimates. The CPI-common is a measure of core inflation that tracks common price changes across categories in the CPI basket. It uses a statistical procedure called a factor model to detect these common variations, which helps filter out price movements that might be caused by factors specific to certain components.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock. All data as of 3/31/2023 and in U.S. dollar terms unless otherwise noted.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.