Quarterly Economic Outlook : An interesting year ahead.

In our last outlook, we said that the fourth quarter of 2024 promised to be at least as interesting as the third quarter had been, and that certainly proved to be the case. Looking ahead to 2025, investors are surely in for an interesting year. We’ll examine some of the risks, both positive and negative, facing Canada’s economy, as well as some of the “known unknowns” investors may want to keep an eye on.

Canadian economy still marching to its own beat

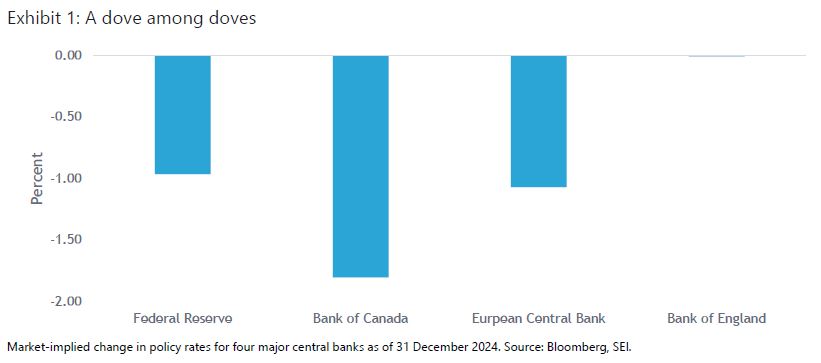

The Canadian economy continues to chart its own path in terms of economic growth, inflation and central bank policy. Relative to other advanced economies, inflation remains well behaved, giving the Bank of Canada (BOC) ample room for further interest-rate cuts. That should be supportive of economic activity, although as we noted last quarter, a widening divide between Canadian and U.S. interest rates could put downward pressure on the Canadian dollar at times.

Recent purchasing manager surveys have also shown an interesting divergence between Canada and the rest of the world. Whereas most countries were recently seeing still-healthy sentiment in services and slumping sentiment in manufacturing, the latest surveys in Canada showed the opposite. Although tempting to attribute Canada’s services downturn to constrained consumers and manufacturing strength to a weaker Canadian dollar (which makes Canadian goods cheaper for foreign buyers), the underlying causes might prove more temporary. For example, some services respondents placed blame on the postal strike, while some respondents to the manufacturing survey believed recent strength might be attributable to U.S. buyers front-running expected tariff hikes from the incoming Trump administration. Time will tell. The good news, in these reports and others, is that the Canadian economy seems likely to continue avoiding recession barring any major surprises (more on those later). It should also be noted, however, that both surveys reported some strengthening in price pressures. While we don’t expect inflation to reaccelerate dramatically in Canada, it does fit with SEI’s view that central banks’ “last mile” in the inflation fight could be a long one.

First, the bad news

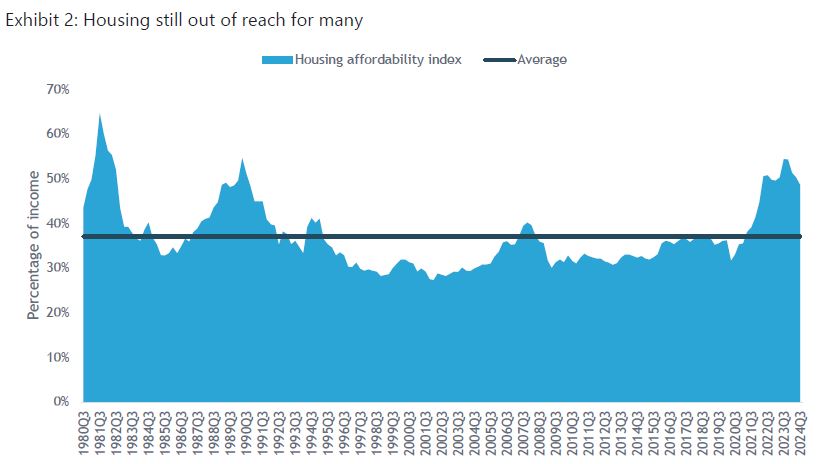

In addition to weaker sentiment in the services sector and the impacts of port- and postal-worker strikes on an already slow-growing economy, there are some clear and present risks to account for, listed roughly here in terms of potential impact. First, the federal government’s decision to markedly reduce immigration of temporary workers may cause the labour market to tighten and thus contribute to a modest reacceleration of inflation, all else equal (though it may also reduce housing-price pressures at the margin). Second, household balance sheets in aggregate are still overextended and home affordability remains at a generational low (Exhibit 2).

The Bank of Canada Housing Affordability Index provides quarterly estimates of the percentage of household income required to own a home. Data from third quarter of 1980 through third quarter of 2024. Source: Bank of Canada, SEI.

Finally—and most obvious at the moment—are the punitive tariffs rates being threatened against Canada and other trading partners by U.S. President-elect Trump. The only point of clarity thus far is that U.S. trade barriers will be higher, while the specifics of what these will look like are anyone’s guess. Businesses and consumers on both sides of the border will have to adapt as the trade battles unfold and actual U.S. trade policies become clearer. The widespread hope is that, as with the first Trump administration, tariffs are used as a negotiating tool to reconfigure trade patterns or gain immigration concessions without massively undermining the current trading system.

Now the good news

Despite these risks, the Canadian economy should enjoy some tailwinds in 2025 beyond the rebound in manufacturing sentiment. The goods-and-services-tax holiday, although only a couple months in duration, should be welcomed by consumers. Two important tweaks to mortgage regulations—increasing the price cap on insured mortgages which should reduce down payments, along with extending maturities to 30 years from 25 for first-time buyers or new construction—should provide some support to residential real estate activity. And most importantly, the progress made on inflation should allow interest rates to continue falling, which would be supportive of housing and consumers more broadly. None of these will solve Canada’s economic challenges overnight, but they point in a positive direction.

Watch out for wild cards

In addition to the policy risks emanating from the U.S., domestic politics are clearly in turmoil. With his recent resignation, Prime Minister Trudeau joins the list of incumbent casualties around the world. Unfortunately, it now appears the Canadian federal government will be less than fully functional as the Trump administration takes office. That said, the 44th Parliament has had a long run by historic standards, as has the Liberal Party leader, so perhaps a change of the guard was in order. The Canadian electorate certainly seems to think so, as we pointed out last quarter. Similar to trade relations with the U.S., much remains to be seen with domestic politics and policies. The Conservative Party still looks poised to assume power. However, based on historical timeframes, that might not happen until spring or even summer of 2025. Suffice to say, when it is finally formed, the new government will have its work cut out for it.

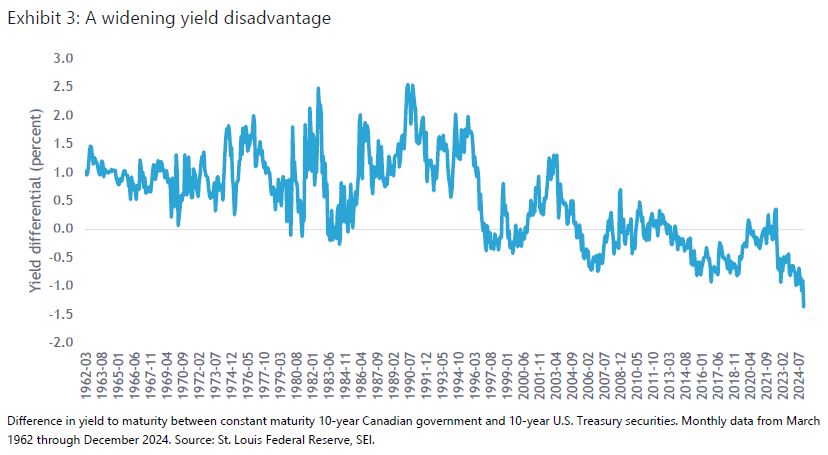

Foreign-exchange volatility is another area of concern. The U.S. dollar rallied sharply in the fourth quarter against a wide range of currencies, including the Canadian dollar. Developments on the domestic and U.S. fronts could cause exchange-rate volatility in either direction. For now, the widening interest rate differential between Canada and the U.S. shown in Exhibit 3 (something we touched on last quarter) could keep the loonie under pressure.

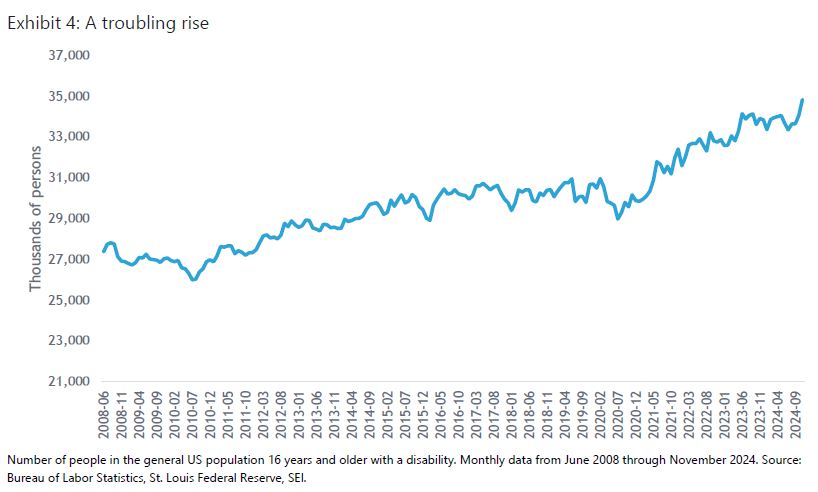

Finally, public health risks are an issue that’s probably flying under most investors’ radars. While we’re all dealing with pandemic exhaustion to varying degrees thanks to COVID-19, we should keep an eye on avian influenza (“bird flu”) and the current H5N1 strain. Related to this risk, it’s interesting (and a bit troubling) to note that, in many countries, disability rates have increased in recent years. For example, in Canada, disability rates increased by a statistically significant extent across all age groups between 2017 and 2022,2 and in the U.S., disability numbers have climbed steadily in recent years, approaching 35 million individuals at the end of 2024 (Exhibit 4). If there’s a silver lining to these data, it’s that that a higher percentage of disabled individuals have been able to join the workforces in some countries. But if disabilities are truly rising, that could add to the challenge of slow-or-no productivity growth (another theme we’ve touched on in recent quarters).

The increasing-disability phenomenon isn’t limited to North America, and it is reported to have multiple causes. However, the after-effects of COVID-19 infections are believed to be a contributing factor, and a recent study estimated that the cumulative number of people worldwide who’ve suffered with “long COVID,” or lingering health effects following acute infection, is around 400 million.3 Taken by itself, this is a challenge that societies will continue to manage with varying degrees of success. But it would become far more worrisome in a pandemic caused by certain strains of avian influenza. Thus far, reported symptoms of individuals infected with H5N1 have ranged from mild to severe, and public health institutions have not identified any cases of human-to-human transmission, which is reassuring. But this is one of those low-probability, high-impact events that, should it come to pass, could cause significant market volatility and economic disruptions.

Advice to investors

The world is as interesting as ever, and there is a raft of challenges facing businesses, consumers, politicians, policymakers, and public health officials. By comparison, an investor’s job is pretty simple. Be sure your portfolio is suited to your financial objectives and provides ample diversification of risks, and stick with it.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.