Quarterly Economic Outlook : More tough sledding ahead?

At the start of the fourth quarter of 2023, we were concerned about a weakening outlook for Canada in spite of some pleasant economic surprises earlier in the year. Subsequent data has largely reaffirmed those worries, and it seems likely we will encounter further weakness ahead. With inflation and inflation expectations easing, the Bank of Canada should have room to lower its interest rate target in 2024. While that would help soften the impact of a business cycle downturn, Canada’s economy could still face tough sledding ahead, and it’s not yet clear that the war on inflation is truly over.

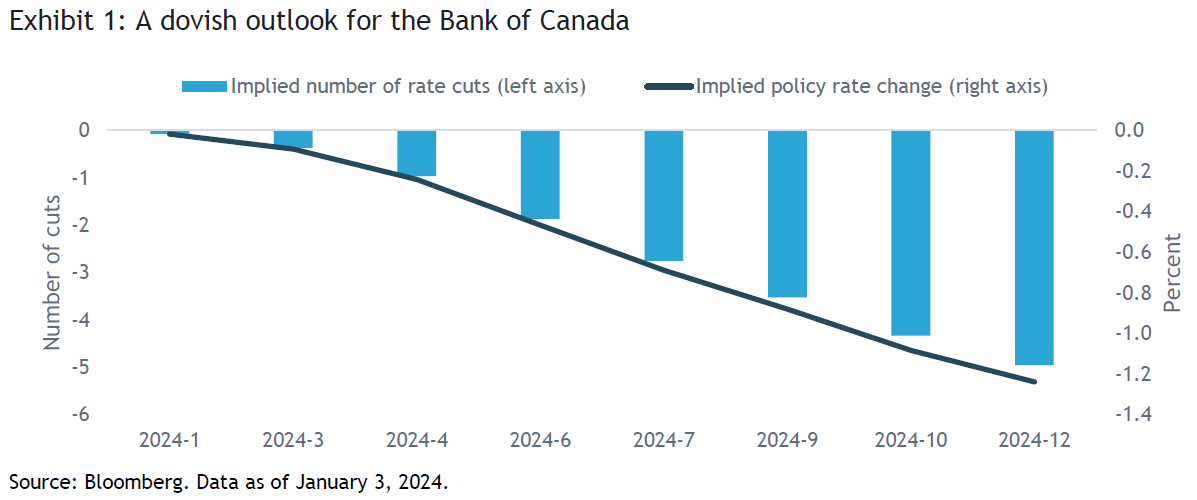

The last quarter of 2024 treated investors to yet another series of global interest rate shocks. This time, downside inflation surprises and a shift in monetary policy rhetoric—particularly by the U.S. Federal Reserve (Fed)—convinced market participants that central banks would soon start cutting their targets for short-term interest rates. The Bank of Canada (BOC) was not immune to this dynamic. As shown in Exhibit 1, the BOC is now expected to cut its policy rate five times (in 0.25% increments) in the year ahead, which would bring its policy rate to 3.8% by December 2024.

As discussed in our most recent Quarterly Economic Outlook and SEI Forward, SEI is highly skeptical of the optimism that’s been priced into rates markets for the Fed. Should that skepticism apply to the BOC as well? Let’s examine the evidence.

The struggles in Canada’s housing market are well known. After some surprising improvement earlier in 2023, both sales volumes and prices have resumed their downward trends since the middle of the year.

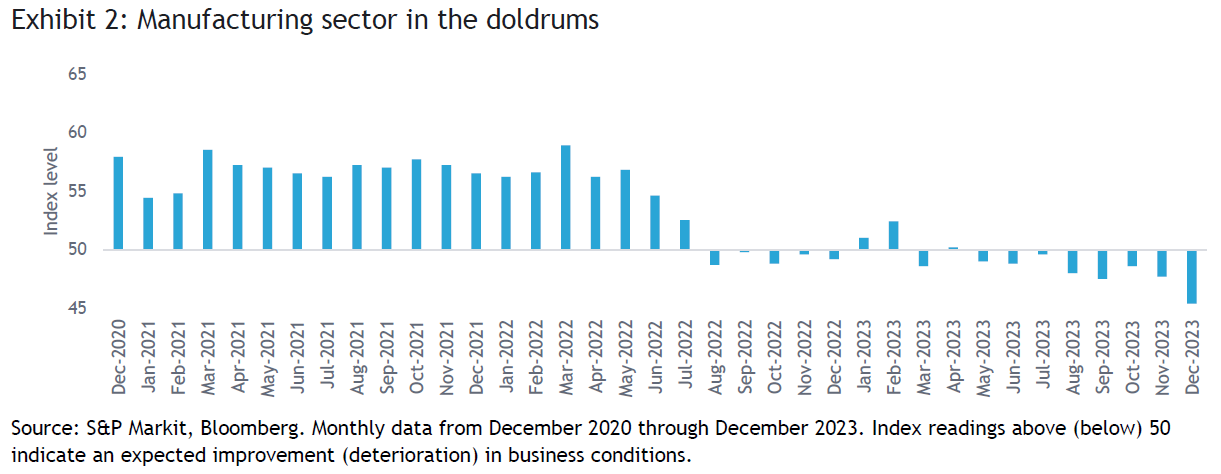

According to a range of surveys, the outlook in Canada’s manufacturing sector actually worsened recently after a string of already-negative reports (Exhibit 2). This is consistent with global manufacturing in general, as consumers have meaningfully shifted their activities from stay-at-home purchases early in the COVID era to services and experiences such as dining out and travel.

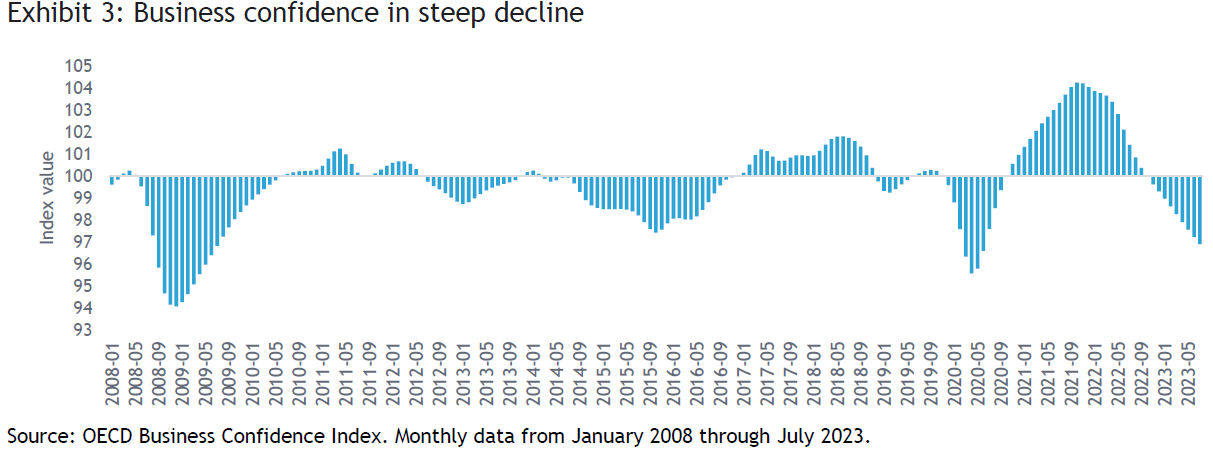

What about the broader business sector in Canada? After all, there’s far more to the Canadian economy than just manufacturing. Unfortunately, the picture here isn’t much better. Imports and exports declined in the third quarter (the latter more so than the former), indicating weaker demand conditions both at home and abroad. The BOC’s Business Outlook Survey (BOS), as well as the Organisation for Economic Cooperation and Development’s (OECD) Business Confidence Index (Exhibit 3), also paint a dour picture. (While the available OECD data runs through July 2023, the BOC survey depicts a similar decline through the third quarter of 2023.)

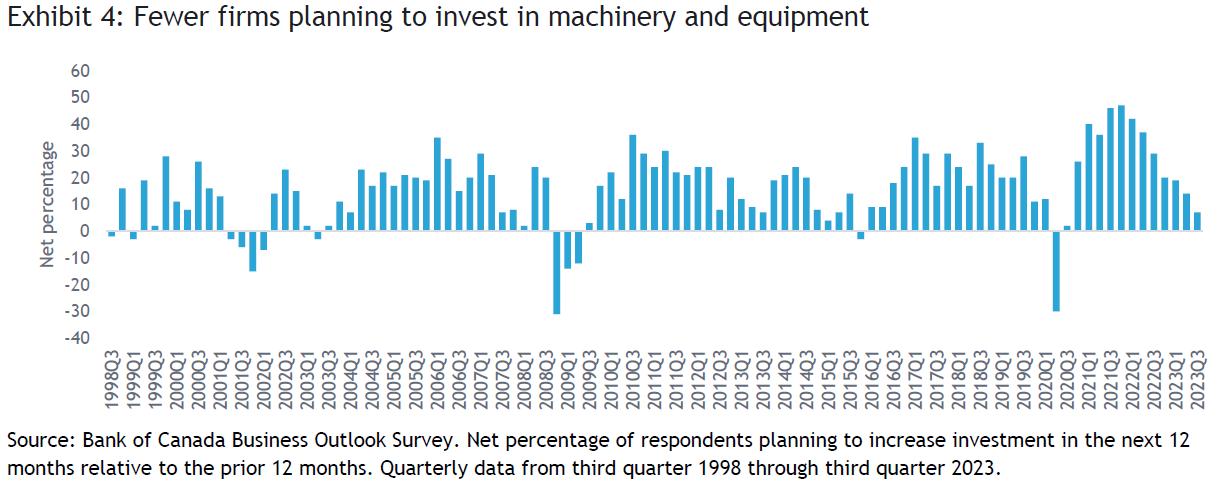

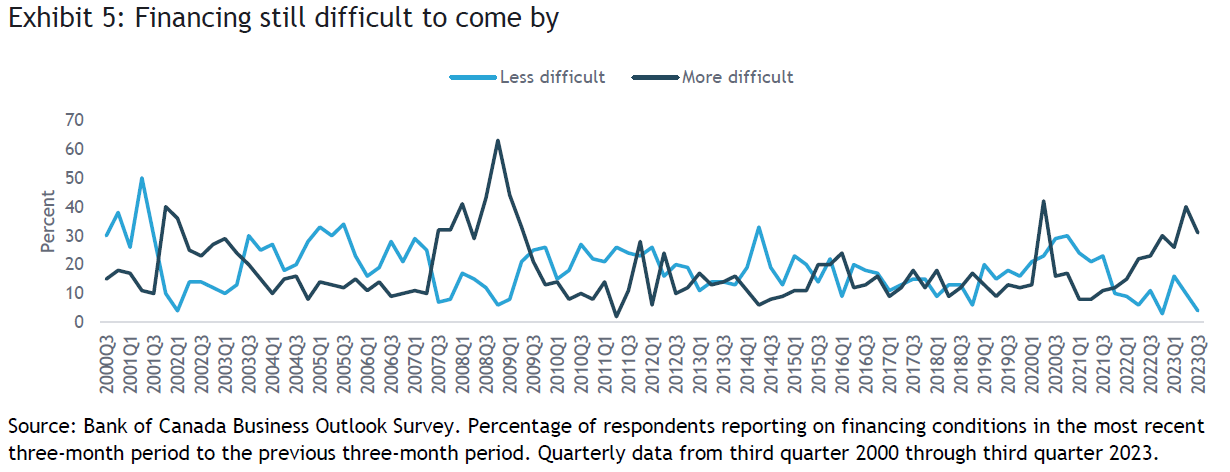

The BOC BOS survey provides additional details that are worth digging into, though readers should keep in mind that this data is as of the third quarter of 2023; fourth quarter survey results should be released later this month. On the negative side of the ledger, both hiring and investment plans (the latter shown in Exhibit 4) continue to decline, and firms are still reporting that credit is hard to come by (Exhibit 5).

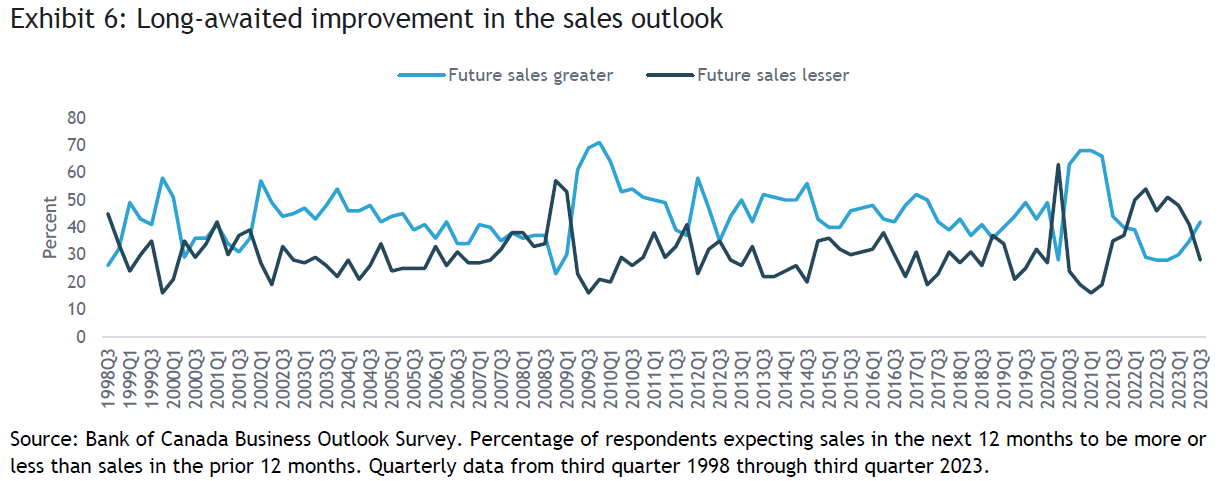

There were some hopeful signs in the BOS details, however slim. While indicators of future sales, such as bookings and inquiries, were flat on balance, the percentage of respondents expecting future sales to improve versus the previous 12 months exceeded those expecting sales to deteriorate; this was the first time that’s happened since the fourth quarter 2021 survey, as shown in Exhibit 6.

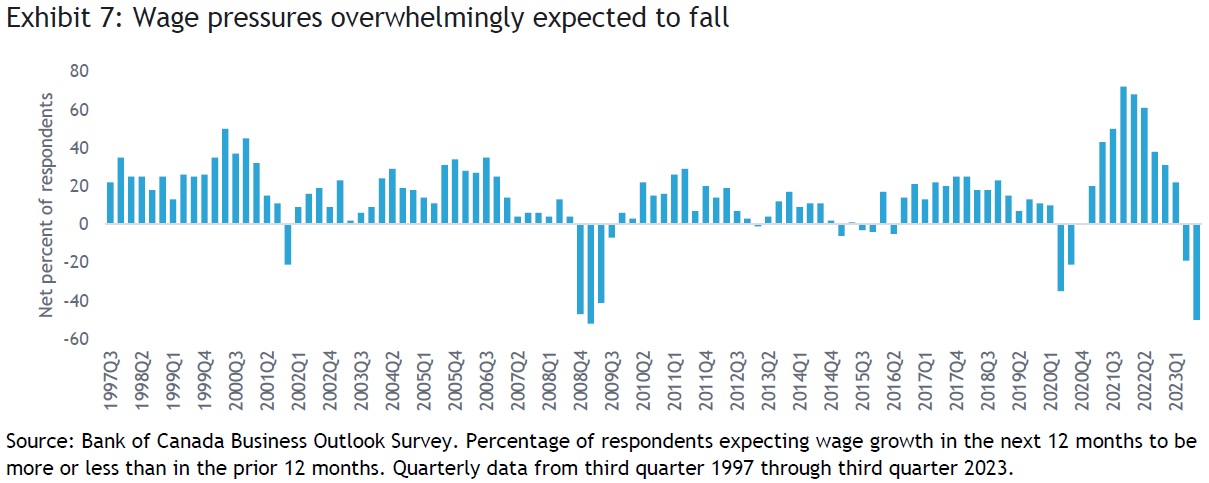

And while respondents reported ongoing labour shortages, an increasing percentage expected wage pressures to subside, as shown in Exhibit 7. Of course, it wouldn’t be ideal for the overall economy if the labour market loosens up too much, but an easing of wage demands (along with falling input costs expected by an overwhelming proportion of respondents) would mean less downward pressure on profit margins and less upward pressure on inflation, all else equal. The inflation aspect will be especially important when it comes to future BOC decisions regarding monetary policy.

When considering this data, it’s important for investors to keep a couple of things in mind. First, economic reality rarely conforms to the picture painted by various survey data, whether from businesses or households. And second, Canada is a relatively open economy—meaning its trade with the rest of the world accounts for a significant portion of its gross domestic product—especially compared to the U.S. As a result, Canada’s economic performance will continue to depend heavily on what happens outside its borders.

That latter fact will remain an important consideration for the BOC as well. Although we have seen early signs of labour market loosening in Canada, this is just one of many factors influencing domestic inflation trends, and the BOC will have to remain attentive to the larger picture. In a recent report, economists from the BOC’s Financial Markets Department estimated that the likelihood of inflation returning to the Bank’s one-percent-to-three-percent target in 2024 had increased meaningfully over the course of 2023; however, they were careful to point out that their modelling still implied a 25% chance that inflation would exceed this range, well above the historical probability of 8%.1 Thus, it’s still too early to say whether the BOC will cut interest rates to the extent that markets are currently implying.

Despite all of this uncertainty, it’s still natural for investors to wonder how the current business cycle might ultimately play out. If a recession does unfold in 2024, will it be particularly deep or persistent? And what might that mean for a portfolio? As of December 2023, economists at Oxford Economics were predicting a downturn to last from the third quarter of 2023 through the second quarter of 2024. But they also expected a fairly healthy rebound in the second half of this year, led by recoveries in consumer purchases, business investment and residential investment.2 Of course, no forecaster has a crystal ball, and the mixed views coming out of business surveys, as well as the well-known overhang of household debt in Canada, call for a reasonable degree of caution. As such, we continue to believe that investors are likely to be best served by having a well-diversified portfolio designed to help them meet their financial objectives whatever the economic and market winds might throw at them.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.