Quarterly Economic Outlook: Somewhat insulated, hardly immune.

Hostilities in the Middle East have closed the critical Strait of Hormuz shipping lane causing commodities prices to spike higher.

These turbulent times are fostering volatility , uncertainty , higher inflation, and could undermine economic growth .It’s not all bad news , however . Canada is relatively well insulated, and a recession doesn’t seem imminent — yet .

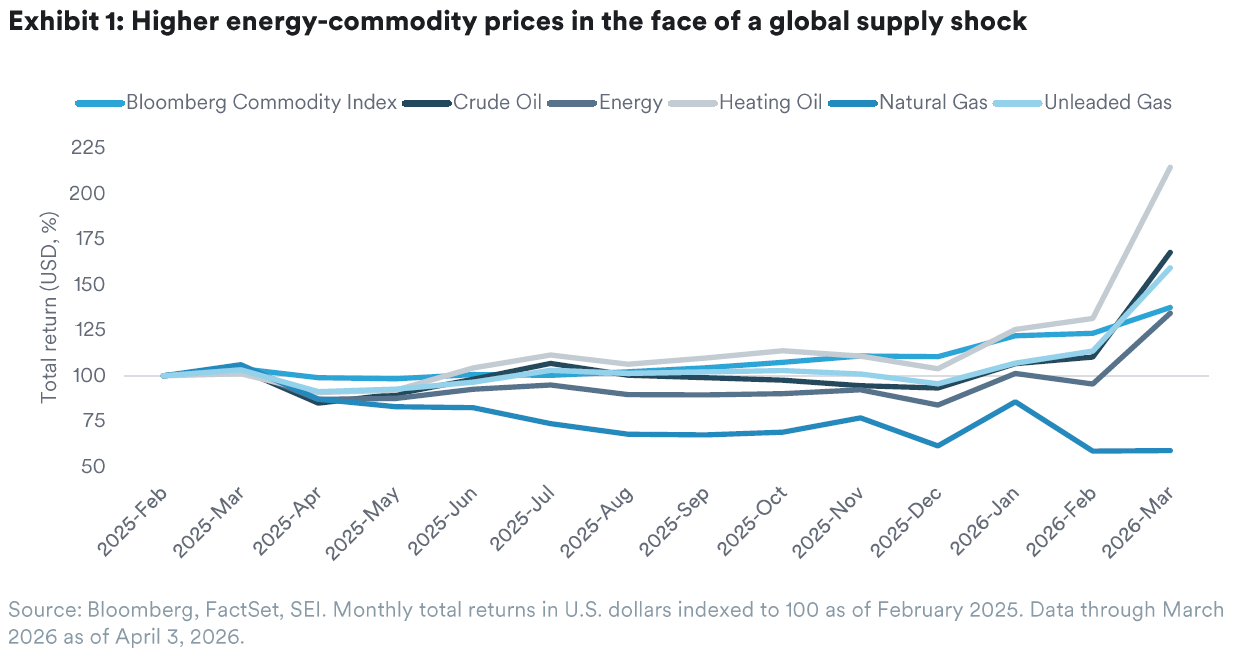

The Canadian economy was already walking a bit of a knife’s edge before the outbreak of military hostilities in the Persian Gulf, the closure of the Strait of Hormuz, and supply and price shocks in global energy commodities and derivatives (Exhibit 1).

“Uncertainty is acute”

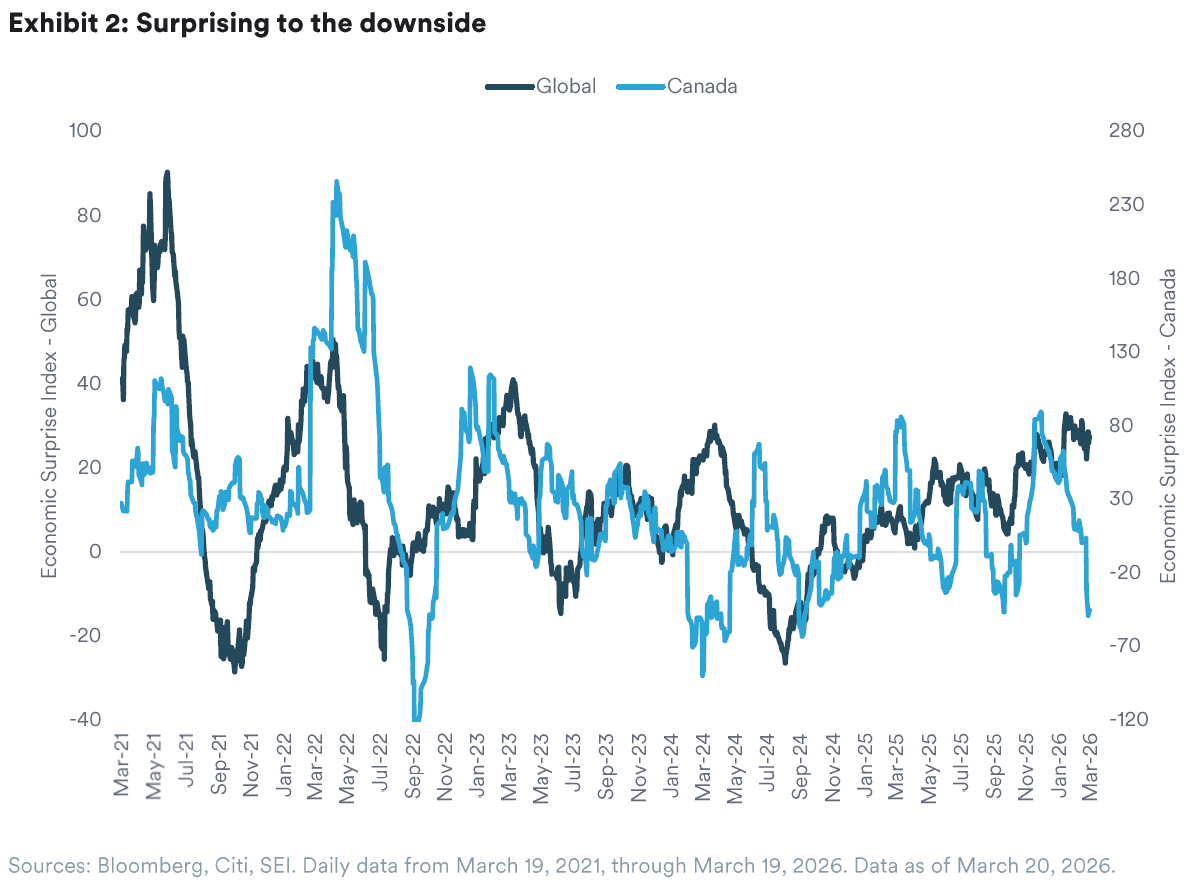

Real economic activity contracted in the fourth quarter of 2025, and economic growth was looking extremely sluggish at the start of 2026. It is important to note that shrinking business inventories were a key driver of fourth-quarter weakness and that domestic demand actually looked healthy. However, a lack of inventory rebuilding may have reflected an absence of business confidence, while labour markets have been showing signs of weakness. Overall, Canadian economic data has consistently surprised to the downside despite a strengthening global picture (Exhibit 2).

As things stood before the end of February, the Bank of Canada (BOC) had the luxury of holding its overnight interest rate target steady in the hope that growth would start to pick up after its latest easing cycle, a view that was reflected in market pricing of expected BOC interest rate policy. The U.S. Supreme Court’s ruling against the Trump Administration’s “Liberation Day” tariffs under The International Emergency Economic Powers Act (IEEPA) also offered a glimmer of hope, although the administration was busy finding other legal rationales for its tariffs and mid-year renegotiation of the Canada-U.S.-Mexico Agreement is still looming.

As a major energy producer and net exporter, Canada (like much of the western hemisphere) is far better insulated against the Strait of Hormuz shock than countries in Asia, Africa, and Europe. The same is true for the human and infrastructure damages arising from the conflict. However, given that crude oil and several related commodities tend to be subject to the Law of One Price, Canadian businesses and consumers are already being forced to deal with higher gasoline and other prices (natural gas price are a welcome exception for now). These higher prices will certainly start to feed into headline inflation in the months ahead and, if supply shortages persist, those pressures could reverse some of the progress made in core inflation measures (which exclude more-volatile energy and food prices). The risk of stagflation—higher inflation against a backdrop of weak or stalling growth—puts the BOC and many other central banks in a very difficult position.

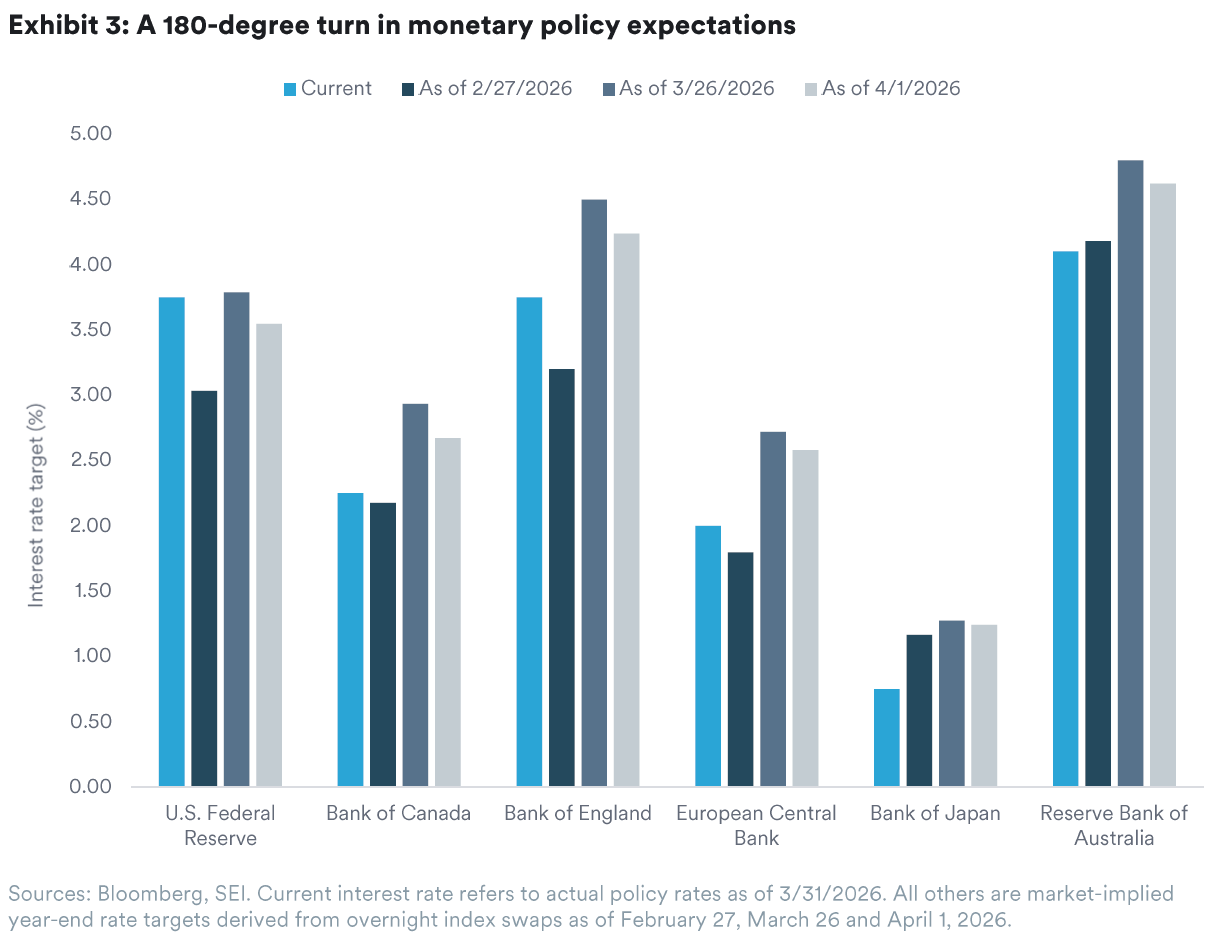

At the BOC’s most recent post-policy-meeting press conference on March 18, Governor Tiff Macklem was quite explicit about the greater level of uncertainty now facing the BOC’s Governing Council. He noted that, although higher energy prices would mean higher export income, consumers were already being squeezed by higher energy prices, financial conditions had tightened, and “transportation bottlenecks caused by the effective closure of the Strait of Hormuz could also impact supplies of other commodities, such as fertilizer… Uncertainty is acute. Trade and geopolitical uncertainties remain, and the conflict in the Middle East has broadened the range of possible outcomes.” The BOC has already penciled in higher inflation and slower growth, and we will be watching its next Monetary Policy Report update in late April to see how its forecasts evolve. For now, markets are betting that the BOC, like a number of its peers, will be forced to tighten monetary policy in 2026 (Exhibit 3).

Is there any good news?

Are there any silver linings for Canadian investors to grasp onto? We see a few but they come with some important qualifications. As already mentioned, while gross domestic product (GDP) contracted in the fourth quarter, domestic demand looked solid enough. However, recent consumer and service-sector sentiment surveys have been notably lacklustre. Fortunately, sentiment surveys are rarely an accurate guide to future activity.

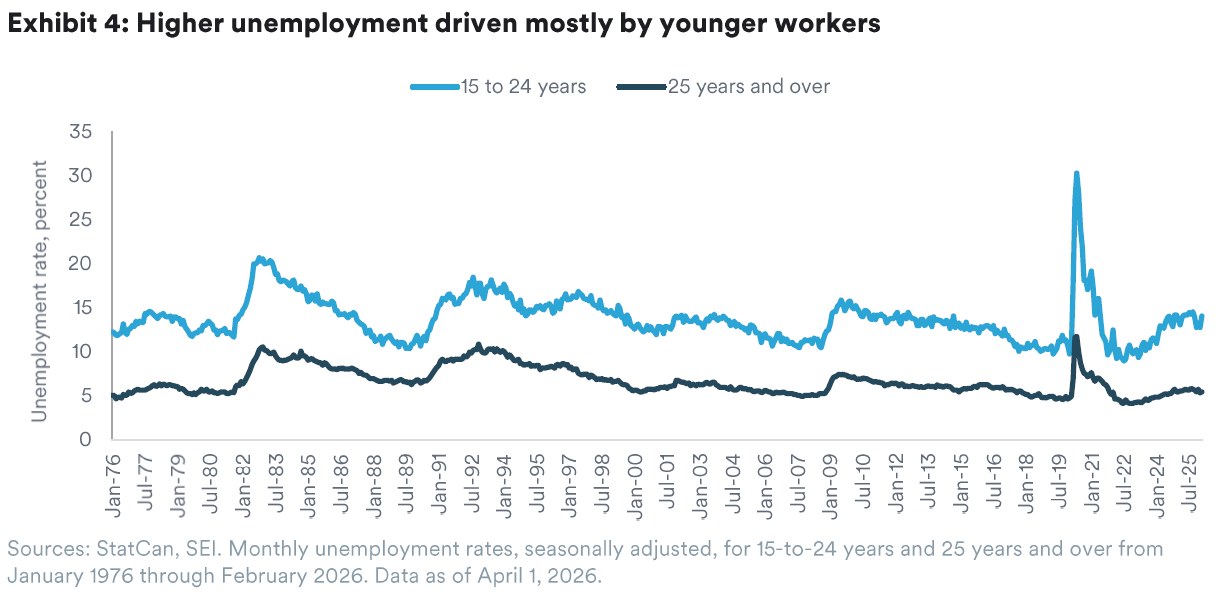

Turning to the labour market, higher unemployment has been driven almost entirely by workers in the 15-to-24-year-old cohort (Exhibit 4), and the spread between youth and ages-25-and-older unemployment sat at the 98th percentile of its historic distribution in February. While high youth unemployment isn’t good, it isn’t necessarily a sign of an impending recession either; although it’s hard to make a well-grounded recession-probability call in normal times, much less amidst the fog of war and global supply chain stress. The bottom line is that it’s encouraging to see unemployment among adult workers remaining below its long-term average.

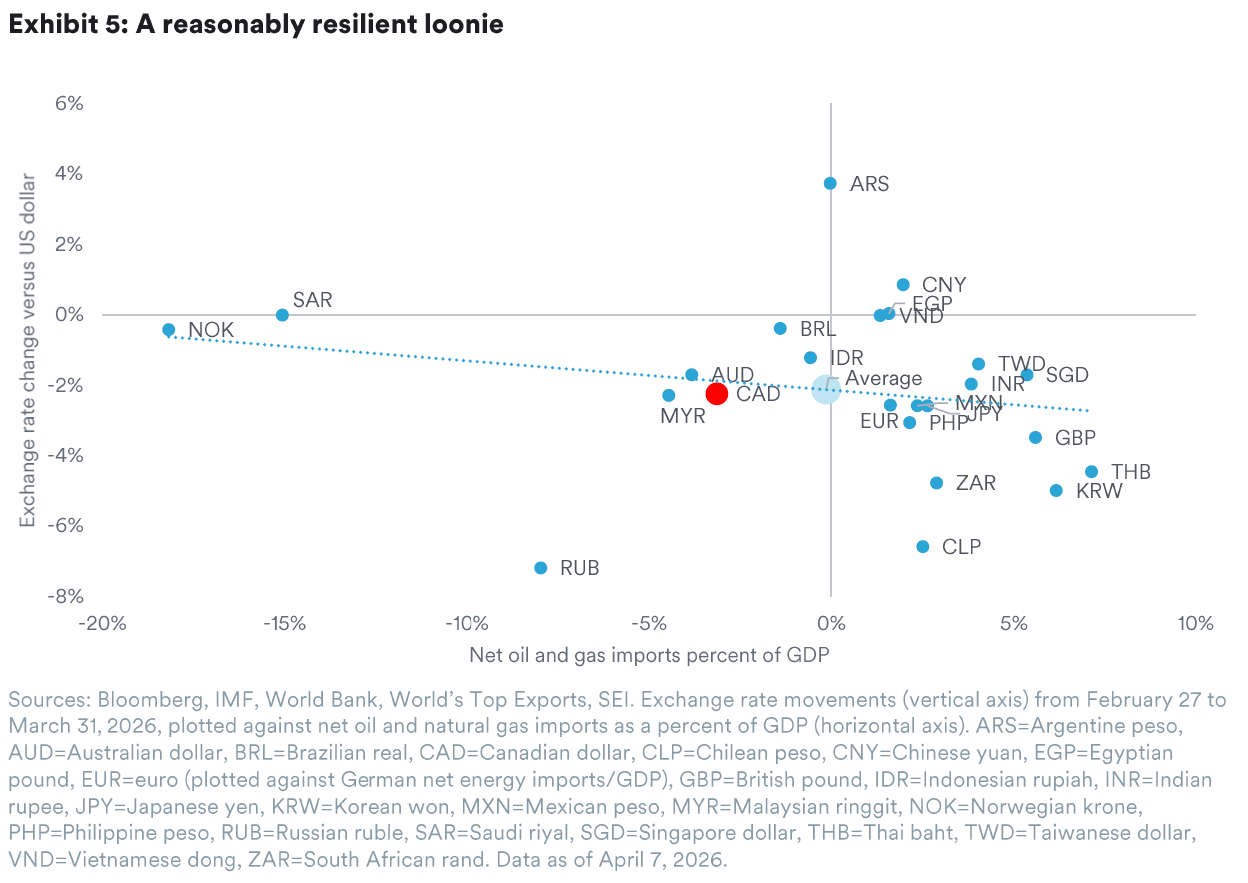

Finally, the Canadian dollar has held up reasonably well since the onset of Persian Gulf hostilities. As shown in Exhibit 5, currency movements against the U.S. dollar have largely reflected the vulnerabilities of net energy importers, and Canada is relatively insulated in this regard.

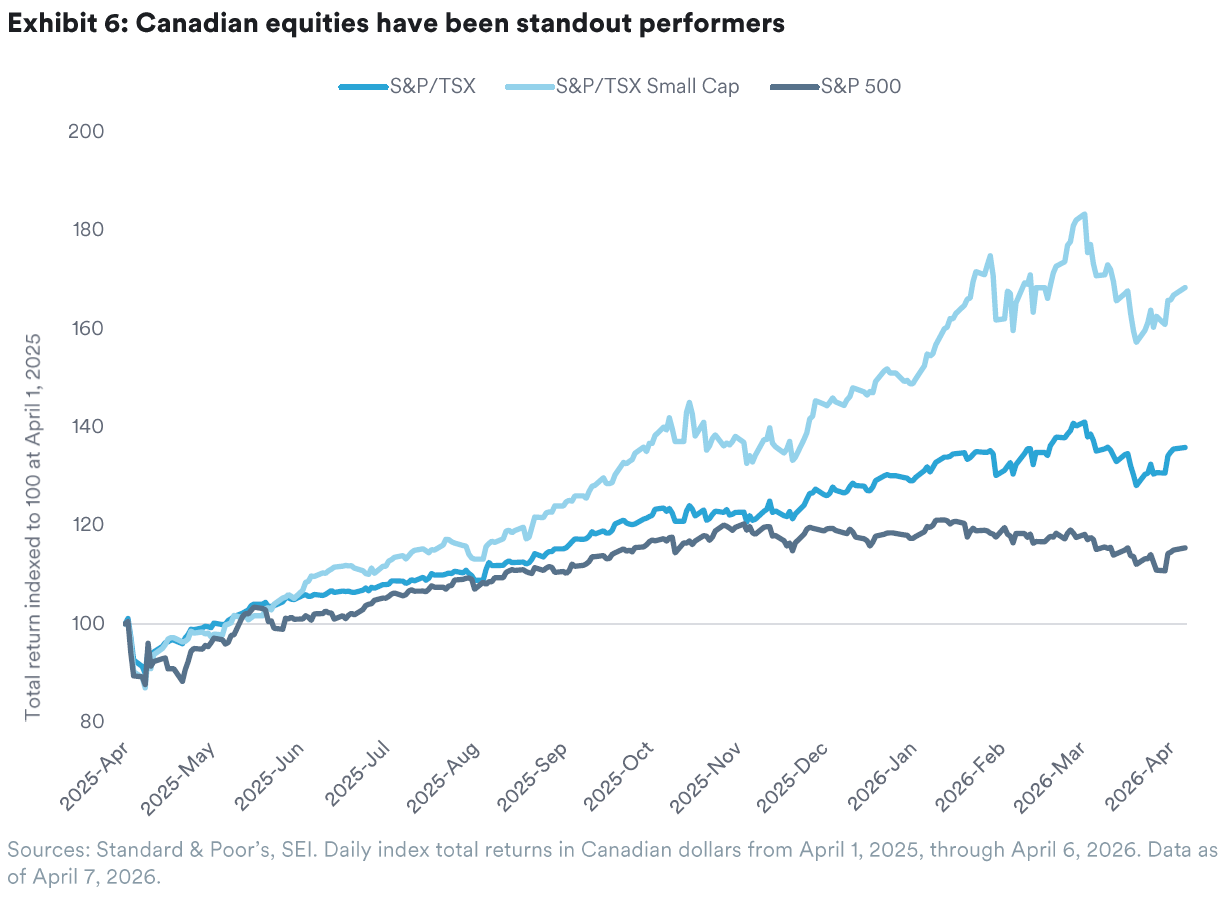

Canadian equities have held up even better than the loonie. As shown in Exhibit 6, the S&P/TSX Composite and TSX Small Cap indexes have outperformed U.S. large caps (as measured by the S&P 500 Index) since the “Liberation Day” shock roughly one year ago. The prevalence of metals, mining, and energy within Canadian markets has been a clear positive for investors’ portfolios.

Where to go from here?

As challenging as the economic, inflation, and interest rate outlooks may seem, it’s not all bad news. Unfortunately, Canadian investors and policymakers will, like their counterparts around the world, have to take a wait-and-see approach to the current upheavals caused by the Iran-Israel-U.S. conflict. It has certainly raised the risk of higher inflation and slower growth in the near term. But there are still a wide range of vastly differing outcomes in sight, and it’s impossible to place a probability on any of them with a high degree of confidence.

While emotional reactions to geopolitical events can be understandably difficult to control, holding a diversified portfolio that is well-suited to one’s objectives and circumstances is still well within every investor’s control. For now, the best advice we can offer is to buckle up—2026 could be another interesting year in a very interesting decade.

Glossary and index definitions

For financial term and index definitions, please see: https://www.seic.com/ent/imu-communications-financial-glossary

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.