Quarterly Economic Outlook : A two-handed look at the economy.

When it comes to the Canadian economy, businesses, consumers and investors are faced with a confusing array of cross currents right now. Economic activity and the labour market have remained on solid footing, but the manufacturing sector continues to struggle, the Bank of Canada is once again hiking rates, and there are other notable risks to the outlook. In environments like these, the timeless principles of sound portfolio design and effective diversification may prove especially useful.

Former U.S. President Harry Truman is reported to have asked for a one-armed economist so he would no longer have to listen to his advisors express their views in terms of “on the one hand, but on the other hand.” While the story may be apocryphal, the sentiment is understandable and no less applicable today, given the confusing cross-currents at work in the global and Canadian economies. These domestic cross currents persisted through the second quarter of 2023, keeping Canadian businesses, consumers and investors on edge. On the positive side, economic growth was solid even when adjusted for inflation, the labour market remained quite healthy, and there were signs that inflation may finally be easing meaningfully. However, soggy leading economic indicators, a manufacturing recession, and renewed Bank of Canada (BOC) rate hikes, alongside longstanding concerns about household debt levels and the potential for a downturn in housing activity, tempered any enthusiasm.

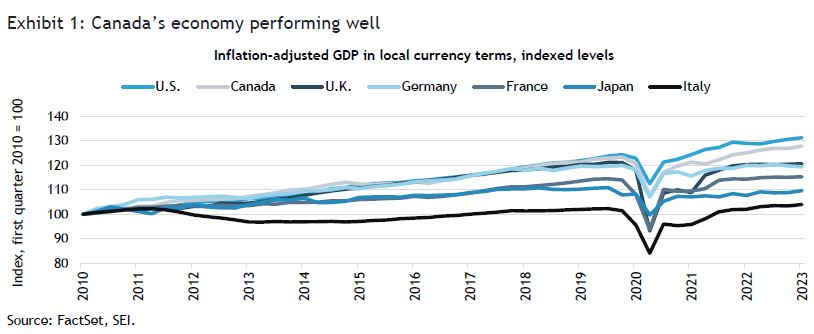

On the one hand, Canada’s economic performance remained quite solid among advanced economies, as shown in Exhibit 1.

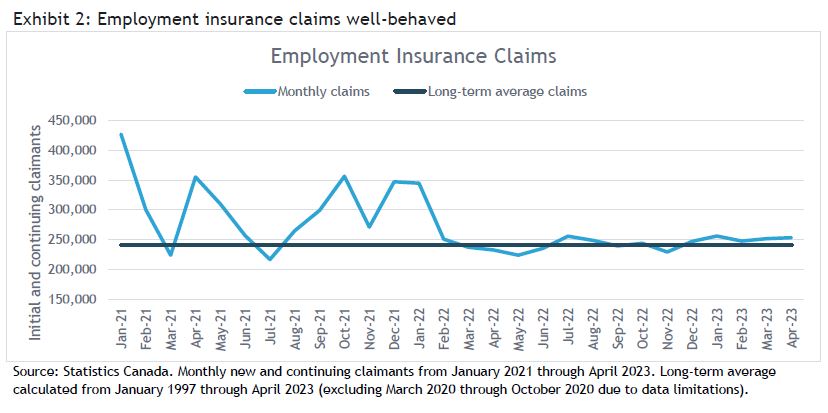

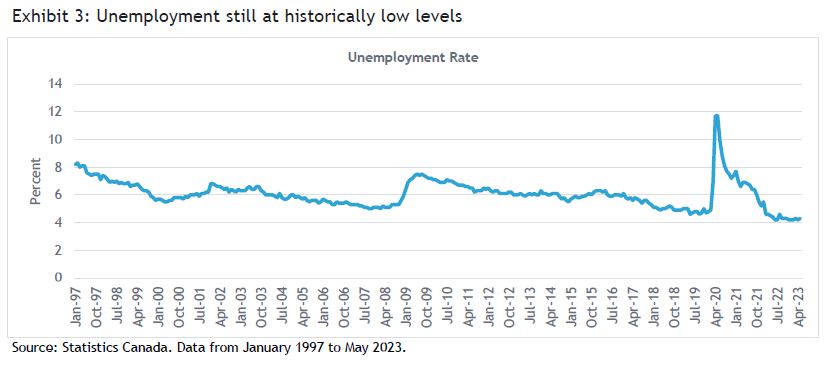

The labour market has also remained quite healthy. Exhibit 2 shows that claims for employment insurance are still well below levels seen during COVID-19 lockdowns and in line with their long-term average, while Exhibit 3 depicts an unemployment rate that is still at historic lows.

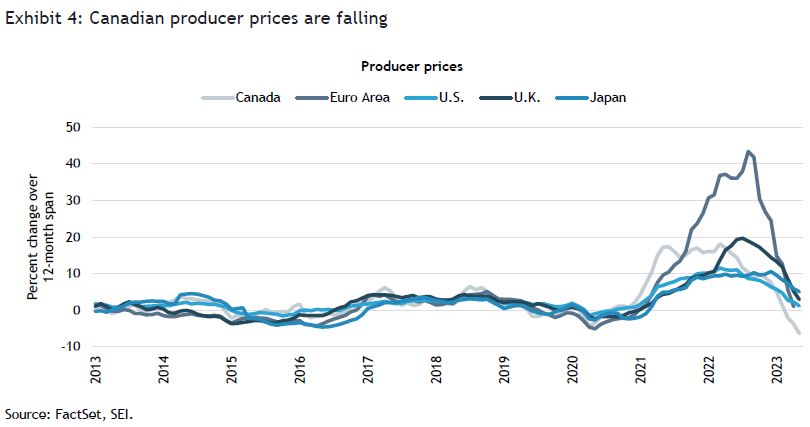

Finally, as shown in Exhibit 4, Canada has made some of the furthest progress against inflation among advanced economies, at least for the kinds of industrial or “factory gate” materials captured in producer price indexes.

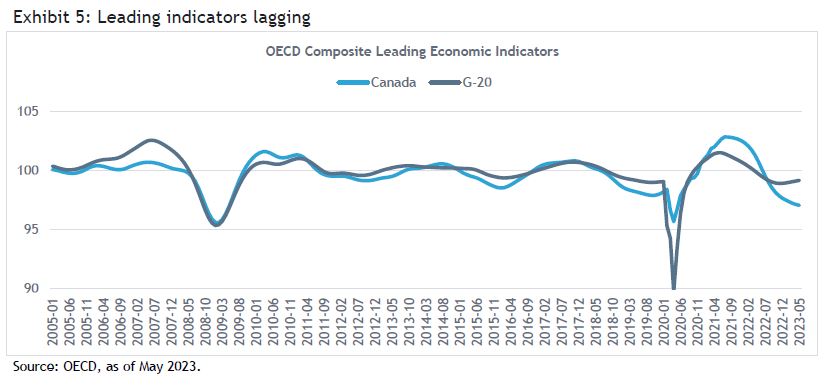

On the other hand (sorry Harry!), Canada’s manufacturing sector (like many around the world) has continued to struggle, with the S&P Global Canada Manufacturing PMI® reporting subdued demand and further declines in output and new orders in June.1 Leading economic indicators are suggesting there may be further trouble ahead for the Canadian economy, as shown in Exhibit 5.

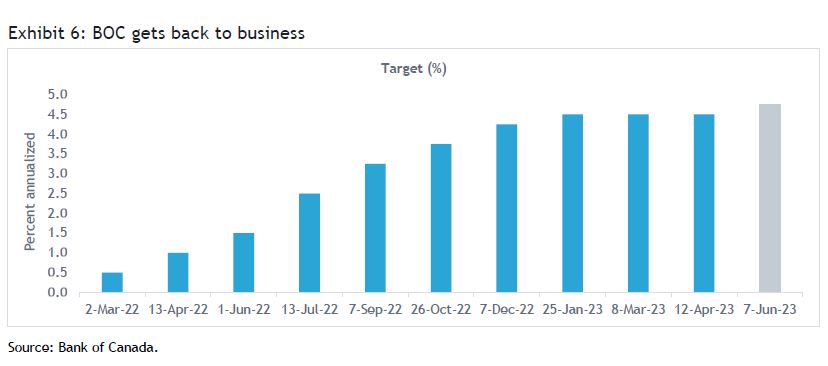

And while falling producer prices illustrated in Exhibit 4 may bode well for the broader inflation picture eventually, demographic and wage pressures could help keep a floor under inflation pressures in more services-oriented areas of the economy. Meanwhile, prices for crude goods such as commodities may be finding a bottom at current levels. With lingering concerns around the inflation outlook, the BOC resumed its rate-hiking cycle after a several-month pause (Exhibit 6).

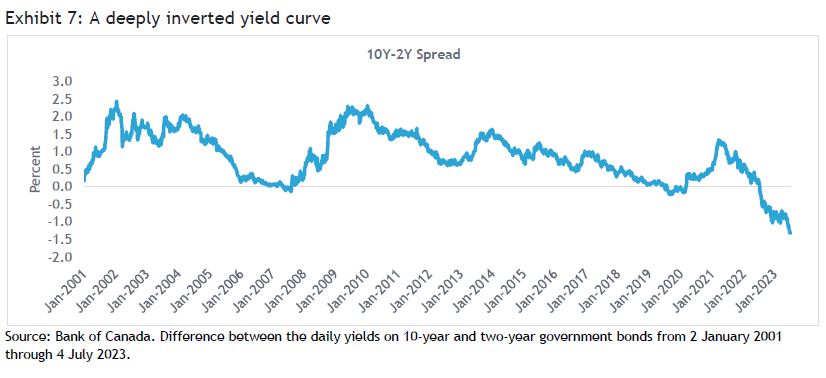

This has led to an even more dramatic inversion of the yield curve, as shown in Exhibit 7, which many economists view as a harbinger of recession.

The recession question is obviously the one that’s causing anxiety for businesses, consumers and investors. While prevailing consensus seems to be that a recession might start in the back half of this year or in 2024, it’s not clear how deep (or shallow) or how prolonged (or short-lived) a downturn might be.

For investors, the name of the game hasn’t changed despite the cloudy economic outlook—ensure your portfolio provides an appropriate level of expected risk for your financial objectives and use diversification to your advantage.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock. All data as of 6/30/2023 and in U.S. dollar terms unless otherwise noted.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.