SEI Forward.

Market review

“In like a lion” certainly held true for the first quarter of 2025 as tariff escalations, new entrants in the artificial intelligence (AI) race, stubborn inflation, and softening economic data all contributed to reversals of fortune from 2024. Recently dominant market themes, including U.S. exceptionalism, European economic stagnation, and a global soft landing, seem to have shifted considerably during the first 90 days of the year as international equity markets outperformed the U.S., Germany launched substantial stimulus measures, and U.S. interest rates fell on rising recession probabilities. Investors’ hopes for an “out like a lamb” remainder of the year appear unlikely given the continued overhang of tariff announcements and retaliations, the on again/off again peace negotiations in Europe, and mixed messages from corporate earnings and consumer behavior that reflect a “wait-and-see” approach to these uncertain times.

The Long Game

Uncertainty is one of the clear certainties of capital markets. In fact, any endeavor that involves discounting the future (such as investing) exists in the realm of uncertainty. There are times, however, when uncertainty feels more…present. I think most would agree that our current moment clearly falls into that category, and for good reason. Thus far, 2025 has delivered more than just a momentum reversal, the potential for steeper and wider applications of tariffs, and a higher probability of a U.S. recession. It has also delivered (or at least highlighted) some notable transformations affecting the global economy and capital markets.

Consider that:

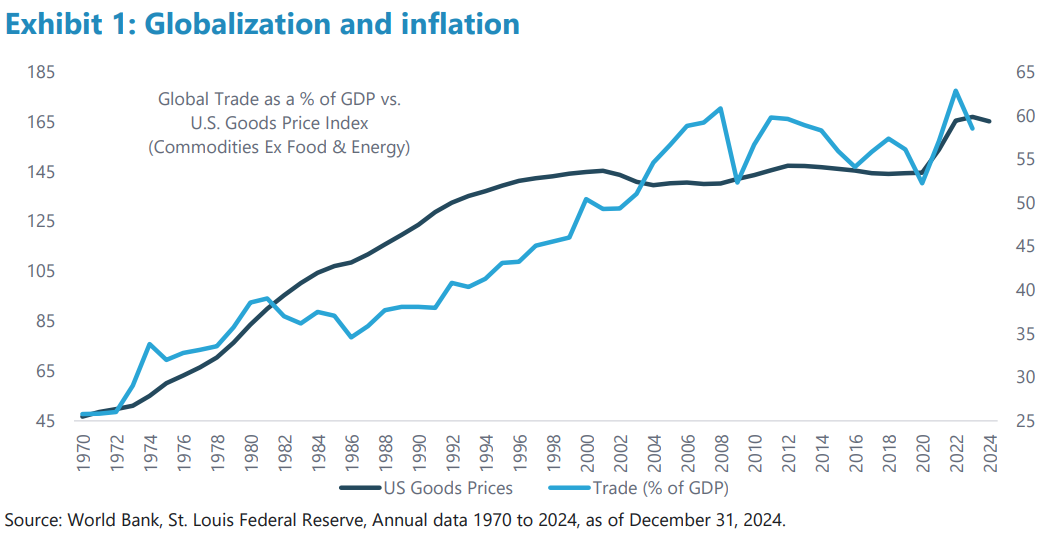

• Globalization and the idea of fully optimized supply chains are now officially things of the past.

• The European model of underinvesting in/outsourcing of defense spending is being challenged.

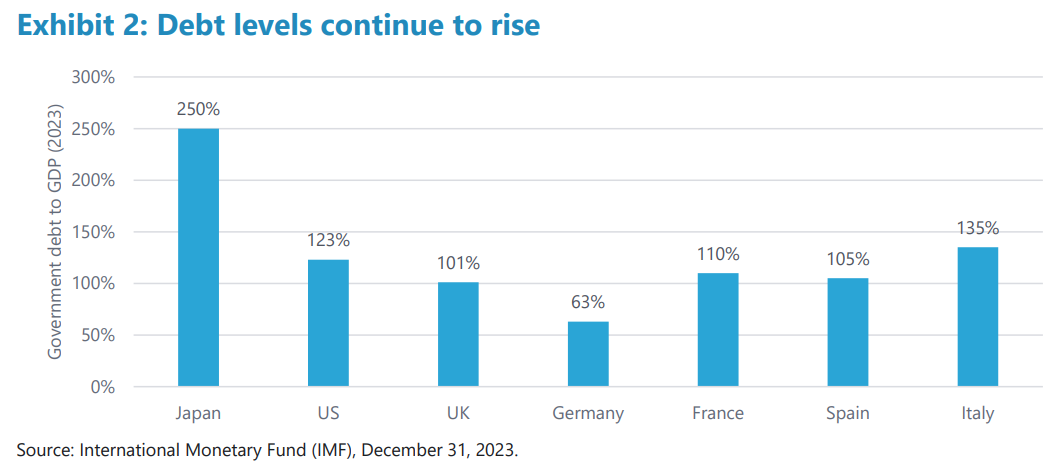

• The unsustainability of U.S. spending and debt growth has been, at the very least, acknowledged.

In short, global alignments and individual country approaches to commerce, defense, and debt are shifting from the models of the past. In response, investors are rightly asking; “How do we adapt?”

The answer here may be unsatisfyingly simple: Play the “long game,” which involves maintaining a globally diversified portfolio at an appropriate risk level that is robust to multiple economic environments. From a practical standpoint, this means:

1) Avoid home-country bias. This is particularly true in the U.S. given the already substantial capital weighting in global indexes. Investors should also include emerging markets, both equity and debt, given demographic profiles, growth differentials, and typically better debt dynamics.

2) Inflation sensitivity should be a strategic holding. Many of the dynamics currently in flux across the globe are inherently inflationary. Maintaining strategic exposure in some form to inflation sensitive assets is a key component of a diversified portfolio.

3) Consider actively managed implementations. We continue to hold a skeptical view on defaulting to passive exposures in every asset class. Somewhat controversially given recent history, we even apply this perspective to U.S. large-cap stocks (where we note that the concentration risk present in passive exposures remains among the highest in history). Active equity management, particularly in factor portfolios, can be an effective strategy to diversify away the heightened idiosyncratic risk of passive implementations.

Our strategic recommendation to maintain diversified active exposures, including to value, quality and momentum strategies, remains intact.

The short game

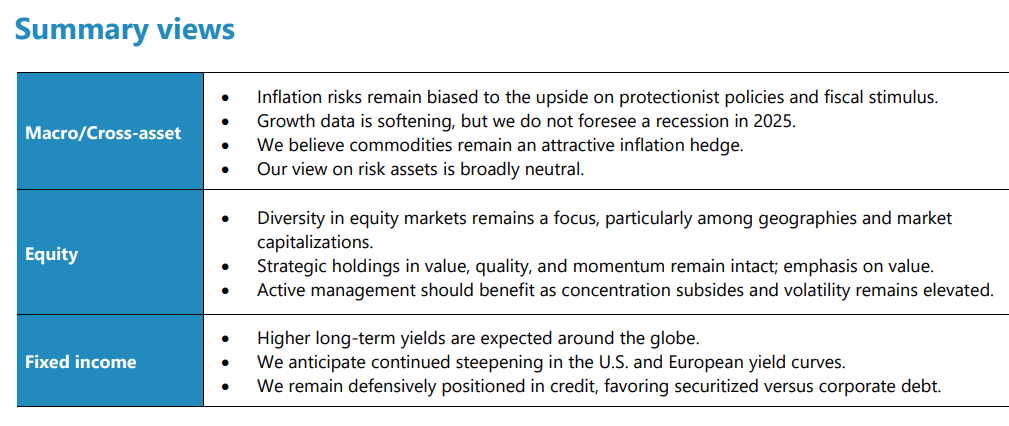

More tactically, our expectations for a broadening of equity market performance have certainly played out from a geographic perspective. Markets have moved substantially in response to global stimulus measures in Europe and the DeepSeek surprise in China, so while there are no more true bargains to be had, we continue to favor broad global exposures. Corporate earnings guidance has been understandably mixed given the political overhangs, but we expect the outlook to improve with some additional clarity and as more market-favorable developments (such as deregulation in the U.S.) begin to progress. Our tactical leaning into value remains in place, as we expect value stocks to continue to benefit from market dynamics, including stubborn inflation, higher interest rates, and a reassessment of the AI landscape. From a sector perspective, we generally favor sectors such as financials, industrials, and consumer staples.

Within fixed-income markets, we remain negative on long-term interest rates both in the U.S. and in Europe. German stimulus measures are potentially just the beginning of a reset across the continent related to spending priorities. However, while Germany has room to increase spending on defense and infrastructure given its modest debt-to-gross-domestic product ratio, the remainder of Europe is in a much more precarious situation. This prospect for additional stimulus broadly across the continent in addition to the already stubborn inflationary readings, continues to give us confidence that the path of least resistance for longer-term global interest rates is higher.

The budget game

Speaking of rising debt levels, it is worth mentioning that, at least in the U.S., reigning in government spending has entered the conversation. While there are legitimate debates to be had in terms of the approach being taken, the fact that the unsustainable current path of debt growth is being taken seriously is a huge positive. This effort will be a long and bumpy road but a worthwhile journey, nonetheless.

Finally, credit spreads are reflecting the general downturn in risk assets and have widened out into quarter-end from historically tight levels. While we are not forecasting a recession, we remain cautious on credit and prefer securitized sectors relative to corporate credit.

Commodities remain a tactical overweight as we prefer more inflation sensitivity in 2025 give the high potential for price disruptions from tariff implementations across the commodity complex, as well as the ongoing central-bank demand for precious metals.

Indexes

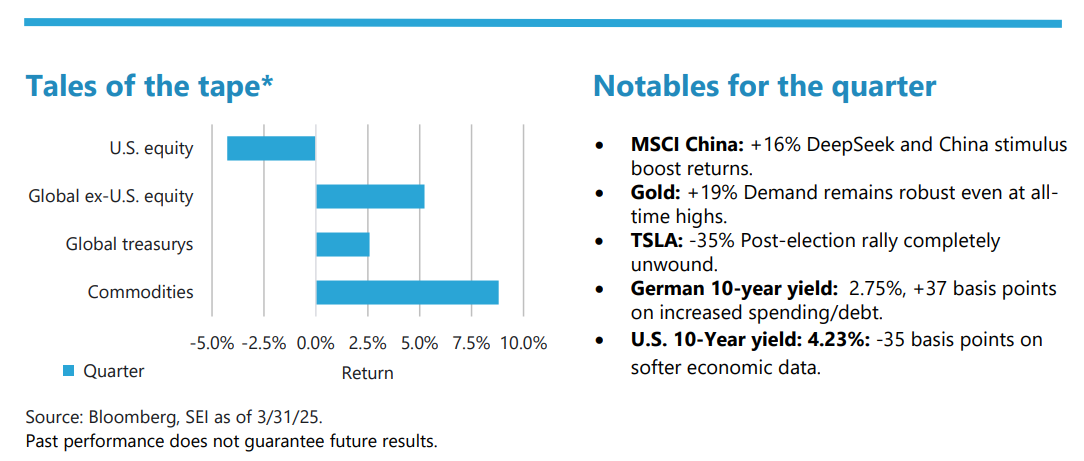

*Tales of the tape: U.S. equity: S&P 500 Index; Global ex-U.S. equity: MSCI ACWI ex-U.S. Index; Global Treasurys: Bloomberg Global Treasury Index; Commodities: Bloomberg Commodity Index.

Indexes definitions

The Bloomberg Commodity Index comprises futures contracts and tracks the performance of a fully collateralized investment in the index. This combines the returns of the index with the returns on cash collateral invested in 13-week (three-month) U.S. Treasury bills.

The Bloomberg Global Treasury Index tracks fixed-rate, local currency government debt of investment grade countries, including both developed and emerging markets.

The MSCI ACWI ex USA Index tracks the performance of both developed-market and emerging market countries, excluding the United States.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

Glossary

A basis point equals .01%.

Momentum is a trend-following investment strategy that is based on acquiring assets with recent improvement in their price, earnings, or other relevant fundamentals.

Quality comprises a long-term buy-and-hold strategy that is based on acquiring shares of companies with strong and stable profitability with high barriers of entry (factors that can prevent or impede newcomers into a market or industry sector, thereby limiting competition).

Risk assets, such as equities, commodities, high-yield bonds, real estate, and currencies, carry a degree of risk and generally are subject to significant price volatility.

Value is an investment strategy that is based on acquiring assets at a discount to their fair valuations. Mean reversion is a theory that prices and returns eventually move back towards their historical average.

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, Morningstar, Bank of Canada, Federal Reserve, Statistics Canada and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.