SEI’s Alpha Sources: An Overview

Evaluating potential alpha sources—that is, drivers of excess returns relative to a benchmark—is a key aspect of our investment process. We continuously study characteristics that are historically associated with excess risk-adjusted returns, which we call factors, along with common investor decision-making biases that tend to foster and give rise to opportunities presented in the overall market. This research allows us to identify desired alpha sources across our equity, fixed-income and alternative investment portfolios. It also informs a framework from which we can assess prospective managers and the efficacy of their respective investment processes. We place investment managers in a given portfolio based on our view of their ability to provide persistent exposure to a specific alpha source or alpha sources.

Our alpha-source framework continues to evolve over time, reflecting the ever-changing nature of global markets. The terminology can therefore be expected to change periodically, as the value of our effort is not in naming specific alpha sources, but rather in recognizing that sources of return can and will vary over time.

Our alpha sources fall into two broad categories:

Systematic alpha sources

- Arise from the collective irrational behaviour of market participants, which causes security prices to deviate from their intrinsic or fair values

- Can be accessed systematically through two different investment approaches:

- Traditional active management, which employs qualitative and quantitative analysis of fundamentals and factors (characteristics historically associated with excess risk-adjusted returns)—seeking to provide exposure to both systematic and idiosyncratic alpha sources

- Factor investing, which employs quantitative rules-based portfolio construction—seeking to provide systematic exposure to known market inefficiencies. Factor investing typically comes with lower costs than fully-active strategies

Idiosyncratic alpha sources

- Generated by unique insights that traditional active managers can garner through research and analysis

- Cannot be systematically replicated

Our alpha-source framework

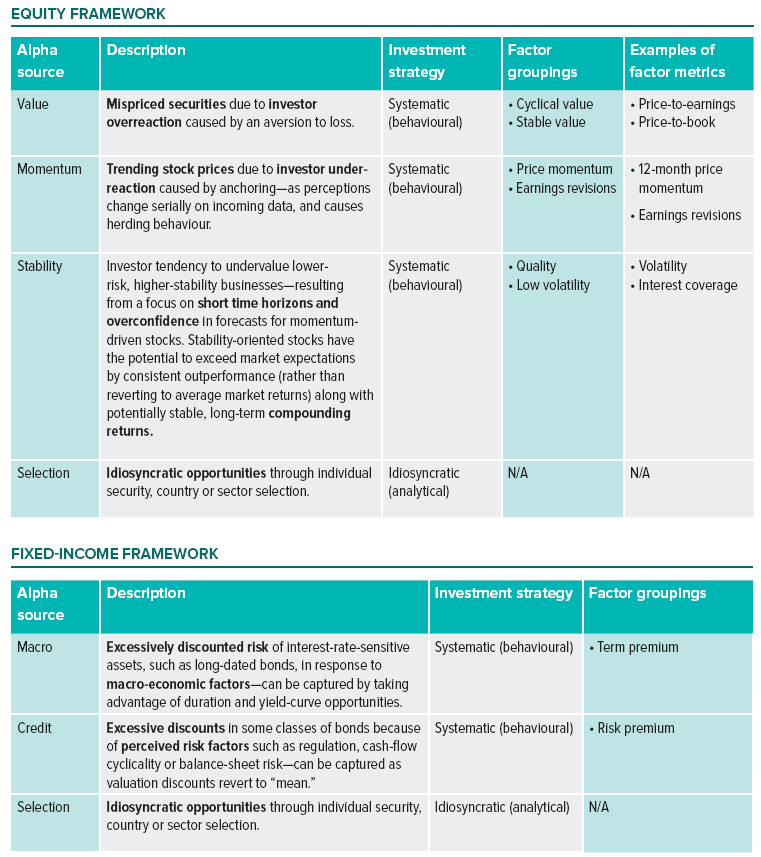

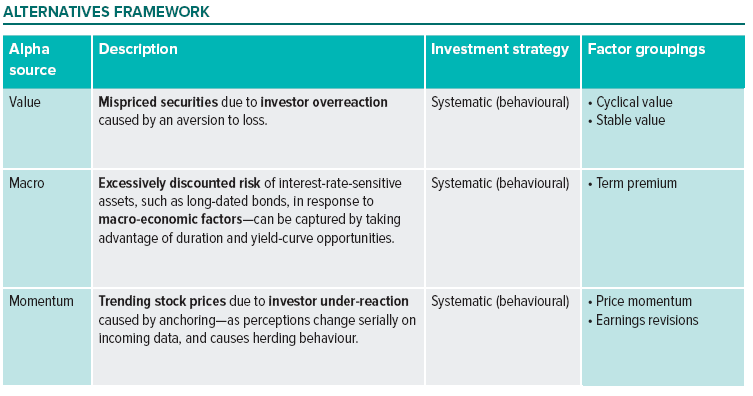

We further categorize alpha sources by “factor groupings”—which we employ as proxies to measure and potentially capture underlying drivers of return. The charts below include examples of these factor groupings.

It is worth noting that our long-term, strategic baseline allocation is to cheaper, higher quality/lower risk securities with positive momentum/improving fundamentals. While we think of this as our “neutral” position, it is not “style neutral.” Generally speaking, even though our starting point for portfolio construction is an equal allocation to each alpha source, portfolio managers determine the actual allocations to reflect expected risk contributions and local market nuances for each individual portfolio.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.