The Shape of the Recovery: V, W or L? Looking Beyond the Letters

Major economic setbacks can trigger a complex re-ordering of entire industries. Our current predicament has gone even further, forcing society to function under siege-like conditions with consequences for every corner of the economy.

It’s challenging to make accurate economic calls even under more normal circumstances. Add in the direct and knock-on impacts of lockdowns, the range of potential paths that the COVID-19 outbreak could take, and the countless combinations of business and policy responses under each of these scenarios, and it is truly anyone’s guess what the future holds.

Why, then, do we try to distill these setbacks into simple shapes? Because humans—and financial markets—don’t like uncertainty. Despite that, guessing whether a recession and the ensuing recovery will look like a U, V or W provides minimal benefit to long-term investors. Focusing on the underlying fundamentals and economics, we believe, is more useful for framing investment decisions.

Searching for Clues

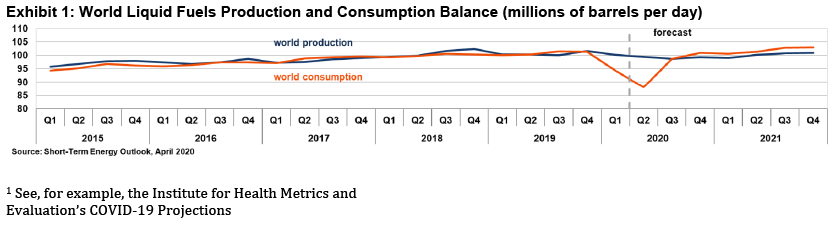

What do markets themselves suggest about the road ahead? A glance at the path of oil prices over the last few months certainly doesn’t project confidence for a strong rebound. The West Texas Intermediate oil price turned negative—a first—as its May 2020 contract neared expiration, and the June contract slid to between $10 and $20 per barrel at the end of April.

Low (and negative) prices imply that storage capacity has gotten full as demand plummeted during lockdown. The U.S. Energy Information Administration’s (EIA) April 2020 Short-Term Energy Outlook estimated “that the 2020 build could add 1.6 billion barrels to global inventories, which would fill them at or near their estimated full storage capacity levels.”

The EIA doesn’t see demand begin to cut into inventories until fourth-quarter 2020, and that assumes global consumption returns close to its long-term level starting in the third quarter (see Exhibit 1).

Interest rates also reflect considerable economic uncertainty. After falling sharply in late February and early March, long-term U.S. Treasury rates bounced into the second half of March. They have inched lower again in recent weeks. Long-term rates generally decline as economic conditions soften, so a flattening yield curve—anchored near zero on the short end—suggests there’s still great uncertainty about the economic road ahead.

Contagion Contingencies

Projections for the spread and fallout from COVID-19 have been subject to revision in recent weeks.1 First, they declined as the public adhered to social distancing and lockdown measures at a greater-than-expected rate. Then, as epidemiological models moved through their peaks and the narrative rolled on to the timing of re-opening society, policies were forced to follow—loosening restrictions and pushing projections back upward.

The fluidity of COVID-19 forecasts is compounded by their wide potential ranges of outcomes. It’s completely in keeping with honest statistical modeling to offer a base case along with low and high projections, but such a wide range limits their utility for health-system planning purposes, let alone forecasts about the economy and financial markets.

SEI’s View

We spent much of February, March and April preaching patience and moderation in the face of steep selloffs and historic volatility. We contended that the decline was too fast and that it would likely be followed by a substantial rebound.

We think moderation is warranted again, albeit in the other direction. The rebound (notably driven by the same mega-cap technology firms that led the bull market) could eventually yield to another pullback, especially given the widespread uncertainty and shortage of concrete positive developments.

We expect the re-opening of the global economy to proceed cautiously and unevenly within and across countries. Many major developed-market countries still need to establish enhanced testing to track and isolate the outbreak before returning to broader re-opening. It will take time before this accrues to a meaningful increase in economic activity.

Many emerging markets are still seeing increased infection rates, so we’re far from a return to normal conditions. Moreover, there’s a possibility we may return to lockdown later this year if COVID-19 cases appear set to spike again.

Our investment managers are thinking in terms of years, rather than months, before the corporate earnings environment recovers from below-trend economic activity to more normal conditions. We believe there will be plenty of opportunities for skilled managers to capitalize on and that investors will be rewarded for their patience and moderation through shorter-term advances and declines.

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.