U.S./China Trade Tariffs Tax Markets

The recent trade stalemate between the U.S. and China rattled investors, resulting in a modest stock-market decline. The unfavourable market reaction was understandable. Yet, as with other recent declines, we think this one will be limited in size and duration. Until we see many more negative fundamental developments—both in the U.S. and globally—our long-term outlook will remain the same.

Not so Taxing

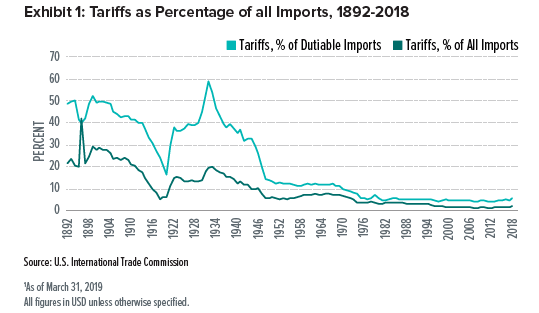

We find it hard to argue that tariffs implemented by the Trump administration have had a severely negative impact on the U.S. economy. In fact, trade duties remain historically low; we almost need a magnifying glass to see their rise as a percentage of all imports. There is no reason to believe that current tariffs will cause the U.S. economy to slow as they did in the 1930s, when levies were much higher and extended to most goods imported from far more countries, as seen in Exhibit 1. The additional 15% tariff on $200 billion of Chinese goods equates to a seemingly dramatic $30 billion tax increase. However, in the context of a $21.1 trillion U.S. economy that includes $2.9 trillion of total merchandise imports1, an extra $30 billion in taxes seems less significant.

If the U.S. applies more tariffs, American companies will likely begin to seek substitutes for the affected products. Currently, this includes mostly intermediate inputs and capital goods; last week’s round of increases affected the same items as those impacted in July 2018 and September 2018. Consumer goods have largely been left alone, which has softened the blow from tariffs for the average person.

China’s retaliation against the U.S. has already reduced demand for U.S. agricultural products, leading to fewer exports of American soybeans, corn and wheat to China. Yet this decline isn’t wholly attributable to Chinese retaliatory efforts. African swine flu has recently devastated China’s pigs and hogs, causing the country’s pig farmers to require fewer imports of American grain to feed their herds. While China’s retaliation against the U.S. in response to tariffs may impact some sectors and industries, we think it can only go so far.

A Little Less Attached

The relationship between U.S. and China began to unravel well before the Trump administration first applied tariffs. The U.S. investment in China’s electronics industry had already been sliding for years. Meanwhile, Chinese investment in the U.S. plummeted last year by over 80%—not only in response to U.S. tariffs, but also because of tighter U.S. government regulations on China’s investments amid security concerns. We view the growing divide between China and the U.S. as an ongoing existing trend rather than the start of a new development.

Investors’ biggest concern is further escalation. The Trump administration is already considering imposing another 25% tariff on the remaining $325 billion of Chinese goods. China’s merchandise-goods exports to the U.S. account for about 20% of total U.S. imports and 20% of China’s total exports. These are significant numbers. If tariffs were applied to another tranche of Chinese products, it would be a huge deal—basically doubling the amount of tariffs that have already been applied. American consumers would definitely feel it—and see it in the prices of the goods they buy.

Still, we think China stands to lose more than the U.S. if the trade situation is not resolved. The next round of tariffs would affect items such as toys, clothing and footwear—products that have low profit margins and employ millions of people in China. Doubling current tariffs would mean that most of these Chinese products would become uncompetitive virtually overnight.

Also, these types of merchandise do not necessarily need to be produced in China, which is considered a high-cost country for an emerging economy. Production could be moved over time to lower-cost Asian countries, such as Vietnam, Cambodia, Pakistan or Sri Lanka—another possible pain point for China if tariffs are applied to the rest of its U.S. exports. In our view, the overall potential loss to the Chinese economy should be enough to convince the country to stay at the negotiating table

Macro View: The U.S. Looks Fine

While a few days of market volatility have rattled Wall Street, long-term performance remains strong. As we enter the last week of May, the S&P 500 Index is valued near the upper end of its trading range over the last year at about 16x forward earnings. We expect earnings to continue rising, with year-over-year expected earnings gains in the S&P 500 Index north of 5% by the end of 2019. Such an advance would be far less significant than that of the last calendar year, but it would still be positive—and likely in line with most other regions of the world.

While U.S. equity markets recorded strong gains in early 2018, markets fell hard during the fourth quarter of that year. Analysts were therefore busy reducing earnings estimates for 2019. However, by the time first-quarter earnings started to come out, we saw unusually large upward revisions of estimates. This reversal eased expectations of an imminent bear market, as earnings tend to fall on economic weakness before such a dramatic market downturn ensues. We don’t foresee a serious earnings slump. That is only likely to happen if the U.S. enters a recession.

We also don’t foresee the U.S. Federal Reserve (Fed) inducing a recession anytime soon. The inflation-adjusted federal-funds rate is still much lower than at other points when recession hit. During the last economic cycle, the real (inflation-adjusted) rate was over 3% before recession occurred. Before that, in 2001, it reached well over 4%. Going back even further, in 1991, the real federal-funds rate surpassed 6%. As long as inflation remains near the Fed’s 2% target, the central bank has little incentive to engage in additional rate hikes. We expect the Federal Reserve to refrain from raising interest rates for the rest of this year and perhaps into 2020, depending on what happens with the trade negotiations with China.

We previously thought an acceleration of U.S. gross domestic product growth in the second half of 2019 may convince the Fed to raise rates. With the current uncertainty, we now expect the Fed will continue to hold rates steady even if U.S. economic growth accelerates.

Europe and the U.K. Look OK

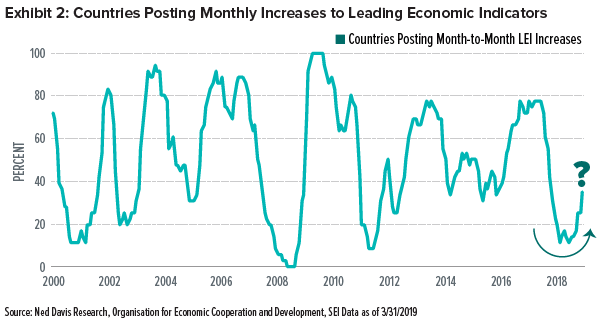

Two-fifths of the 37 economies surveyed by the Organisation for Economic Co-operation and Development reported month-over-month increases in March in its index of leading economic indicators, as shown in Exhibit 2.

It remains to be seen how the current global stock-price pullback will impact future readings, but economic conditions in these countries have definitely been improving. Europe in particular has seen notable gains. The economies of both the U.K. and eurozone have seen positive shifts, with the data surprising on the upside since the start of 2019 despite slow growth and Brexit uncertainty.

The U.S. economy has also finally shifted to the upside in recent weeks. This was welcome news after the Citigroup Economic Surprise Index—which measures whether economic reports meet projections—fell in March to the lowest point since 2013.

Currency Questions

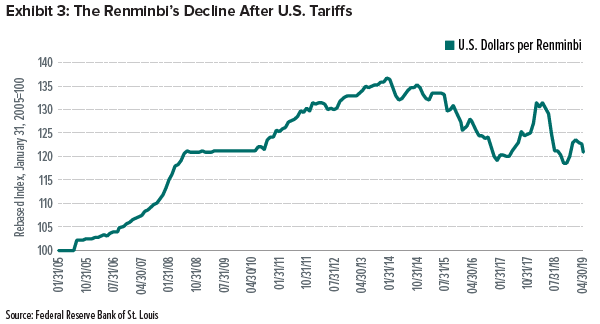

It should not be surprising that the Chinese renminbi (yuan) has declined against the U.S. dollar in the aftermath of the latest tariff increases. The currency fell by nearly 10% after the initial round of tariffs last year, when the U.S. applied a 10% tariff on $200 billion of Chinese goods, which basically offset any negative impact on Chinese exporters as highlighted in Exhibit 3.

Whether the renminbi will decline further is a good question. We don’t expect it to be a one-for-one match against future tariffs, but it’s reasonable to expect a decline of between 5% and 10%.

The U.S. dollar tends to rise in such periods of economic and policy uncertainty, but our outlook on America’s currency is mixed right now. It has yet to return to its peak achieved at the end of 2016, having only made begrudging gains in value on a trade-weighted basis. Neither is it showing signs of soaring higher, as it did in 2014. And we don’t expect it to. There are counter-pressures on the U.S. dollar that reduce the chances of such gains, even in this uncertain period.

A rising U.S. dollar could weigh on profit margins and revenues of multinational companies based in the U.S. We haven’t seen much downward pressure on profit margins thus far, since productivity improvements have offset the impact of rising wage and interest costs.

What’s Next?

As investors fret about whether trade talks will go from bad to worse, we expect further price corrections in the near term. With the underlying strength and resiliency of the U.S. economy, however, along with the Fed maintaining rates and signs of improved global growth, we are confident that the downside in risk assets will be short-lived.

If anything, this situation only reinforces our mantra of “buying on the dip.” U.S. equity prices have been resetting since the S&P 500 Index recovered from its 25% Christmas Eve bottom. We believe this should permit fundamentals to once again drive U.S. stock prices to higher levels later in the year.

Index Definitions

The S&P 500 Index is an unmanaged, market-weighted index that consists of 500 of the largest publicly-traded U.S. companies and is considered representative of the broad U.S. stock market.

Glossary of Financial Terms

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately available funds (balances at the Federal Reserve) to another depository institution overnight in the U.S.

Forward earnings: Forward earnings are an estimate of a next period’s earnings of a company, usually to completion of the current fiscal year and sometimes of the following fiscal year.

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health such as amount of debt, level of profitability, cash-flow, inventory size, etc.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affiliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations.