Ownership matters: Aligning capital with mission through diverse-owned managers.

Introduction

Across the institutional investment landscape, asset owners are increasingly seeking to align portfolios more closely with their mission and values. Community foundations, endowments, and other mission-driven investors have shown interest in allocating capital to asset managers that are owned and led by individuals from historically underrepresented communities or communities they directly serve. This interest reflects both an acknowledgment of persistent inequities in capital allocation and a belief that expanding access to capital can contribute to more inclusive economic outcomes. Within this context, manager diversity—particularly ownership diversity—has emerged as a priority for many clients engaging with SEI on mission-aligned investing initiatives.

SEI’s work with community foundations and other asset owners has highlighted that achieving greater mission alignment is best understood as a portfolio-level objective rather than a standalone allocation choice. While allocations to diverse-owned managers can play a meaningful role, they are typically considered within a broader investment framework, shaped by multiple objectives. The central challenge for asset owners is translating these often overlapping objectives into a practical, investable portfolio that maintains appropriate standards around risk management, return exposure, and governance.

This paper builds on SEI’s research and practical experience in implementing diverse-owned managers in client portfolios. It outlines SEI’s approach to sourcing and evaluating diverse-owned managers, examines the key implementation challenges that asset owners commonly encounter, and explores broader considerations for embedding these priorities within an investment policy statement (IPS).

How SEI defines diverse-owned managers

As part of its Diverse-Owned Manager Program, available exclusively to institutional investors, SEI applies a clear and consistent definition of what constitutes a diverse-owned manager. For the purposes of SEI’s research, diverse managers are defined as firms that are at least 50% owned by women or minorities. This ownership-based definition is intentionally stringent and is designed to ensure that our clients’ capital is meaningfully supporting firms where ownership (and therefore long-term economic benefit and control) resides with individuals from historically underrepresented groups.

SEI’s identification of diverse-owned managers draws on multiple sources, including public databases and SEI’s internal research resources. Ownership is assessed across several categories, including Women, Black, Asian, Hispanic/Latino, and an “Other” category that includes firms owned by individuals of North African, Middle Eastern, or Native American descent. Naturally, some asset management firms could sit across multiple diverse-ownership buckets (e.g., a majority women- and Hispanic-owned firm). Exhibit 1 below highlights some of the higher-profile firms that sit solely within one of these categories.

The size of the diverse manager opportunity set

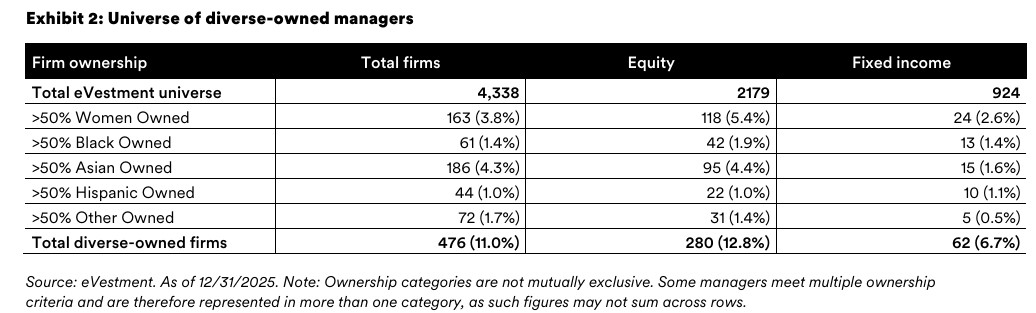

One of the key challenges of identifying and investing in diverse-owned managers is the relatively small size of the available universe. As of December 31, 2025, the global eVestment universe comprised approximately 4,338 firms. Of these, only 476 firms (approximately 11% of the total universe) met SEI’s definition of being more than 50% owned by women or minorities. While this number is relatively small, it reflects structural characteristics of the asset‑management industry, where many firms are publicly listed or owned by large insurance companies or banking groups, resulting in ownership that is typically widely dispersed or institutionally controlled.

When disaggregating these metrics by asset class, the universe of diverse-owned managers narrows even further. Across the eVestment database, diverse-owned managers represent only 11% of all managers, yet account for a disproportionately smaller share of total assets under management (AUM), reflecting their generally smaller scale. Representation by asset class varies, with diverse-owned firms comprising around 12.8% of equity managers and just 6.7% of fixed-income managers in the eVestment universe. Within individual ownership categories, representation is smaller still, with firms that are more than 50% Black-owned comprising approximately 1.4% of the total universe, and firms that are more than 50% women-owned comprising just under 4%.

These figures highlight an important reality for asset owners: While interest in allocating capital to diverse-owned managers is growing, the investable universe remains limited, particularly when combined with other portfolio constraints, such as asset class, geography, style, liquidity, and vehicle structure.

SEI’s research focus: Public equity and public fixed income

SEI’s research into diverse-owned managers has focused primarily on public equity and public fixed-income strategies, where data availability, transparency, and portfolio scalability are generally more robust. This focus reflects both client priorities and practical considerations around implementation. Public markets offer greater scope to construct diversified portfolios, manage liquidity, and integrate diverse managers alongside existing exposures.

Within these asset classes, SEI has built a dedicated research effort to identify, evaluate, and monitor diverse-owned managers that may be suitable for client portfolios. As of December 31, 2025, SEI has reviewed all managers within this universe and conducted meetings with over 100 diverse-owned managers across public equity and fixed-income strategies. We conducted meetings with managers that met SEI’s investment criteria and operated within the asset classes in scope of the research. Firms that did not meet these criteria, or in certain cases where the manager was found to have ceased operations, did not advance. This breadth of research provides a foundation for engagement, comparison, and potential inclusion in client portfolios, while still representing a relatively small subset of the broader manager universe.

How the research process differs for diverse-owned managers

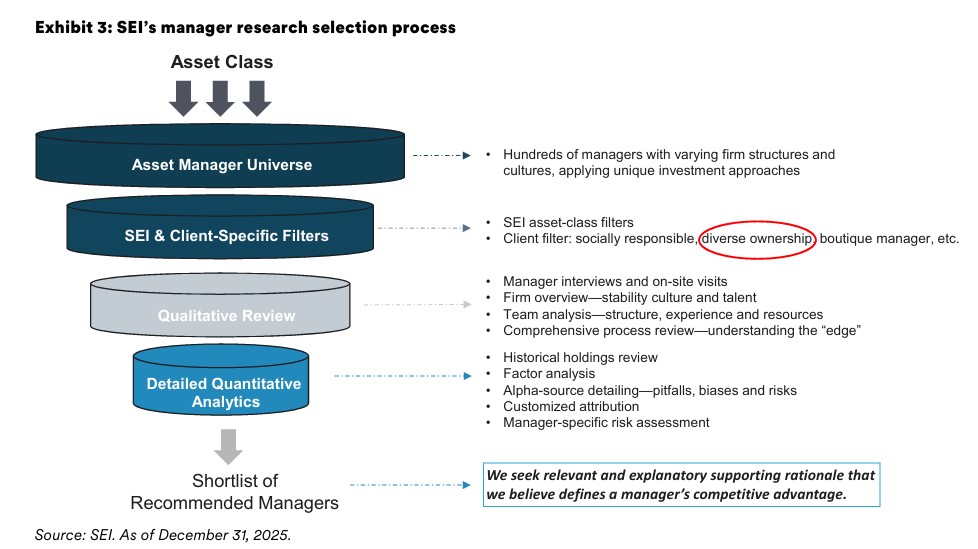

SEI’s core manager research framework remains consistent regardless of ownership structure, emphasizing investment philosophy, process, people, risk management, and sources of return. However, when conducting research specifically focused on diverse-owned managers, SEI applies additional layers of due diligence around each firm’s ownership structure, as highlighted in Exhibit 3.

The first step in the research process is the introduction of an explicit ownership screen, which assesses ownership percentages, voting control, and alignment with SEI’s more than 50% threshold, as discussed earlier. This step significantly narrows the opportunity set. However, the identification process does not rely solely on external databases. SEI also leverages our manager research platform to identify additional diverse-owned managers that may not be captured by third-party data providers, including instances where ownership information is not populated in commercial databases.

Secondly, SEI places greater emphasis on the long-term stability of ownership. This includes evaluating how ownership may evolve over time, succession planning, and the potential for dilution through external funding or changes in control. For mission-aligned investors, durability of ownership is critical to ensuring that capital continues to support intended outcomes. Through meetings with managers, SEI discovered cases where firms that had initially passed the diverse-ownership screen had planned changes in ownership that would lead them to no longer fit our definition of diverse-owned. This underscores both the importance of ongoing monitoring and the limitations of relying solely on quantitative screens to identify diverse owned managers.

Finally, SEI evaluates the extent to which diverse owners are actively involved in the business. Ownership alone may not be sufficient if those owners do not play meaningful roles in investment decision-making, governance, and firm leadership. As a result, SEI’s qualitative due diligence places additional focus on governance structures, leadership responsibilities, and incentive alignment. In some cases, firms have passed the initial diverse-ownership screen, only for our due diligence to uncover that the firms’ owners have no involvement in the business. We have found that in some instances this organizational setup may not align with a given client’s goal in allocating to diverse-owned managers, and consequently, any resulting implementation decisions are guided by the client’s preferences.

Asset-class-specific challenges

The challenges associated with identifying and implementing diverse owned managers can vary significantly by asset class and the type of manager diversity sought by a client. In asset classes such as U.S. public equity or U.S. core fixed income, SEI has identified a viable set of managers that meet both ownership and investment criteria. Even in these areas, however, successive quantitative and qualitative screens often reduce the shortlist to a very small number of viable candidates.

In other asset classes, the challenges are more pronounced. Emerging-market debt (EMD) is a notable example. SEI’s research indicates that there is currently no comparable EMD strategy managed by a diverse-owned firm that closely replicates the exposure of SEI’s existing EMD strategies. This reflects structural barriers, regional concentration of expertise, and limited firm formation in certain markets. As a result, asset owners seeking diverse-ownership exposure in EMD may face trade-offs between mission alignment and maintaining desired portfolio characteristics.

Portfolio construction and implementation trade-offs

Implementing a portfolio with a meaningful allocation to diverse-owned managers often involves a set of trade-offs that must be carefully considered and explicitly discussed with clients. One of the most common challenges is limited manager availability, which can constrain diversification and increase concentration risk.

Fees are another important consideration. Diverse-owned managers, particularly smaller or boutique firms, may not benefit from the same economies of scale as larger asset managers. As a result, management fees may be higher, especially for active strategies or segregated mandates. In addition, the availability of pooled vehicles can be limited, with some managers only offering separate accounts with higher minimum investment thresholds. However, SEI’s implementation framework can enable clients to access certain strategies in select asset classes below stated minimums, helping to mitigate these constraints.

From a risk perspective, portfolios that emphasize diverse-owned managers may exhibit higher tracking error or volatility in certain asset classes, particularly in public equity strategies. This reflects the more limited availability of diverse-owned strategies across distinct investment styles, which can reduce flexibility in portfolio construction. In particular, a narrower opportunity set may limit the ability to combine managers with complementary style tilts to moderate risk, which constrains the ability to build well-diversified portfolios.

Finally (as discussed earlier with our EMD example), there may be asset classes or strategies where no suitable diverse-owned alternative exists, requiring clients to balance mission alignment against the desire to maintain exposure to certain return drivers.

Drafting an IPS for mission-aligned portfolios

For many asset owners, the IPS serves as the critical bridge between mission-driven intent and real-world portfolio implementation. Investors seeking to align portfolios with their mission typically view mission alignment across multiple dimensions, of which investing in diverse-owned managers is but one. Other dimensions may include exclusionary screens, positive environmental, social, and governance (ESG) tilts, thematic strategies, stewardship priorities, or place-based and community investing objectives.

From an implementation standpoint, these dimensions can, at times, compete or conflict. For example, applying strict exclusions while also seeking concentrated exposure to diverse-owned managers within a limited asset class can significantly reduce the investable universe. Similarly, allocating capital to higher-fee or less-liquid strategies in pursuit of one objective may limit one’s flexibility to pursue others

When drafting or revising an IPS, SEI encourages asset owners to explicitly acknowledge these trade-offs. This includes articulating:

• The relative priority of different mission-alignment objectives

• The degree of flexibility across asset classes and vehicles

• Acceptable ranges for tracking error, returns, fees, and concentration

• Where capital is likely to have the greatest mission impact

By clearly defining priorities, an IPS can provide practical guidance on how to allocate capital across competing objectives rather than treating each objective in isolation. This clarity supports better decision-making, sets realistic expectations, and reduces the risk of unintended consequences during implementation.

It is important to note that a well-constructed IPS does not need to resolve every trade-off in advance. Instead, it should establish a framework that allows for informed judgment as opportunities evolve, supported by ongoing monitoring and review.

Looking ahead

SEI views investing in diverse-owned managers as an evolving area of research rather than a static solution. The firm will continue to expand and refine its research efforts, engage with managers, and monitor changes in ownership, strategy, and capacity over time.

For clients interested in better aligning their portfolios with their mission—whether through increased exposure to diverse owned managers, place-based investing strategies, or other approaches—SEI welcomes ongoing dialogue. SEI can work with clients to clarify objectives, assess trade-offs, and design portfolios that thoughtfully balance mission alignment with fiduciary responsibility. Clients are encouraged to reach out to SEI for additional information and to explore how these considerations can be integrated into their investment programs.

GLOSSARY AND INDEX DEFINITIONS

An investment policy statement is an agreement that lays out guidelines for managing an investor’s portfolio, including background, objectives, restrictions, and responsibilities.

Portfolio tilts represent adjustments to a portfolio in order to emphasize given securities’ characteristics, including alpha sources (value, momentum, and quality) or environmental, social, and governance (ESG) criteria.

For additional financial term and index definitions, please see: https://www.seic.com/ent/imu-communications-financial-glossary

IMPORTANT INFORMATION

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice and is intended for educational purposes only. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. The reader should consult with their financial professional for more information.

ESG and Sustainability are not uniformly defined across the industry. Environmental, social and governance (ESG) guidelines may cause a manager to make or avoid certain investment decisions when it may be disadvantageous to do so. This means that these investments may underperform other similar investments that do not consider ESG guidelines when making investment decisions.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction.

Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information in Canada is provided by SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company (SEI), and the Manager of the SEI Funds in Canada.

In the UK and the EEA this information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document has not been registered as a prospectus with the Monetary Authority of Singapore.

This information is made available in Latin America, the Middle East and Australia FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This email and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.