When faced with rising inflation and rates, investors should diversify.

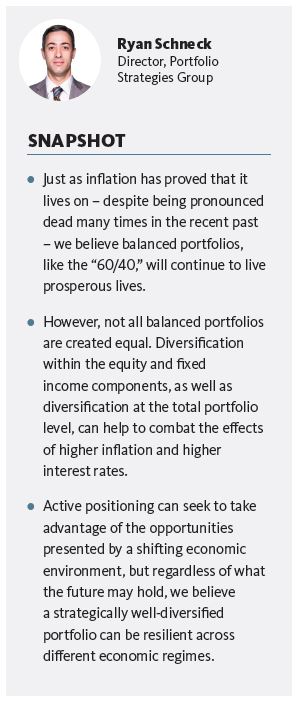

The economic environment of the current era has generally been characterised by healthy economic growth and well-behaved inflation. Viewing the economic environment through this lens, as depicted in Exhibit 1, illustrates that the economic backdrop has been favourable for the traditional balanced portfolio, such as the ubiquitous “60/40.” But the investing landscape is changing. What does this mean for equities, fixed income, and balanced portfolios going forward?

In early 2020, the COVID-19 pandemic upended financial markets and crushed global growth, inflation and risk assets. Thanks to unprecedented levels of globally coordinated fiscal and monetary policy, along with the rapid development of vaccines, financial markets quickly rebounded. Many equity markets made new highs and growth was exceptionally strong.

While these were welcomed developments, a spike in inflation to multi-decade highs has not been as positive. Many central banks—most notably the U.S. Federal Reserve (Fed)—initially considered high inflation to be transitory. More recently, however, the Fed has eliminated its use of the word transitory to describe inflation. With high inflation will likely come higher rates—in fact the Fed, Bank of England, Bank of Canada and many emerging-markets central banks have already begun to raise rates, while other central banks may soon follow.

These developments suggest that the economic environment may be shifting away from the upper-left-hand quadrant of Exhibit 1, i.e. a higher growth and lower inflation regime, toward the upper-right quadrant, representing a higher growth and higher inflation economic regime. While no one can say with certainty which type of economic environment will prevail, we believe the global economy is at a turning point. Investors may feel helpless as these regimes change, but we believe diversification can help their portfolios be prepared for whatever the future may hold, including a higher inflation and higher interest rate environment.

Diversification at every level: Equity

With central bank mandates to maintain stable inflation, interest rates and inflation are highly correlated. While the effects of higher inflation and interest rates are often considered more impactful for fixed-income markets, there are important implications for equity markets as well. The changing investment landscape may continue to create more volatility in equity markets, as we have seen thus far in 2022. While we remain positive on the overall direction of risky assets, we believe that continued changes in equity market leadership are likely. In fact, higher rates and inflation could fuel a continuation of the rotation that started in late 2020. This is when we first saw meaningful reversals in many long-standing trends—including the relative performance of U.S. versus global stocks, emerging versus developed markets, small cap versus large cap, value versus growth, and inflation-sensitive assets versus traditional stocks and bonds, to name a few.

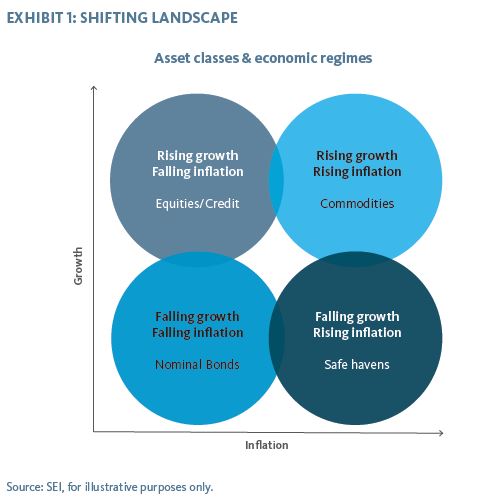

One area that we would highlight as potentially being most impacted is the distinction between expensive and more attractively priced stocks. A simple and common way of making this comparison is through value and growth indexes. Exhibit 2 (left panel) shows that the valuation gap between value and growth stocks remains very wide, globally, despite some of the market rotation that has already occurred. There are still pockets of very expensive stocks that were exacerbated by the COVID-19 crisis and the bidding up of so-called stay-at-home stocks. Because of the two-steps-forward, one-step-back nature of the recovery, due to the delta and omicron variants of the virus, we believe the rotation was interrupted and still has a long way to go before relative valuations are normalised. Rising interest rates could well be the catalyst causing expensive stocks to rerate and reprice. Indeed, as shown in the right panel of Exhibit 2, the fortunes of growth stocks are significantly more tied to the fortunes of the bond market, as compared to value stocks. Growth stocks are much more correlated to Treasurys than value stocks, which could have important relative performance implications going forward.

This bodes well for broader, more diversified equity portfolios, especially relative to portfolios that have become concentrated in large technology stocks, over-valued stay-at-home stocks, growth stocks, or the expensive areas of the market that we believe are particularly vulnerable to rising interest rates. In contrast, we believe SEI’s actively managed equity portfolios are well positioned for the environment ahead. More generally, active management should fare well versus market-cap-weighted, passive indexes that have become top-heavy in some of the aforementioned problem areas.

Diversification at every level: Fixed Income

Fixed income is probably the area that investors are most concerned about when it comes to the prospect of higher inflation and interest rates. This makes perfect sense given the inverse relationship between interest rates and bond prices. However, the rule of thumb stemming from this, perhaps simply stated as “rates up, bonds down,” is an over-simplification and may cause some misconceptions. First, we have to remind ourselves that “bonds down” only refers to bond prices, and the price return component of a bond’s total return is, over time, the smaller and less significant component of return. In fact, as we’ve shown in a previous paper (Rising Rates and Bond Markets: Keep Calm and Clip On – August 2021), during the bull market for bonds over the last 20 years—widely considered to be a golden age for bonds, driven by a secular down-trend in interest rates—only one-tenth of the total annualised return was price return (Bloomberg Barclays Global Aggregate Bond Index, 12/31/2001 to 6/30/2021). As shown in our paper, the coupon return is by far the more significant contributor to total returns over the medium-to-long-term, and coupons should actually benefit from rising rates over time.

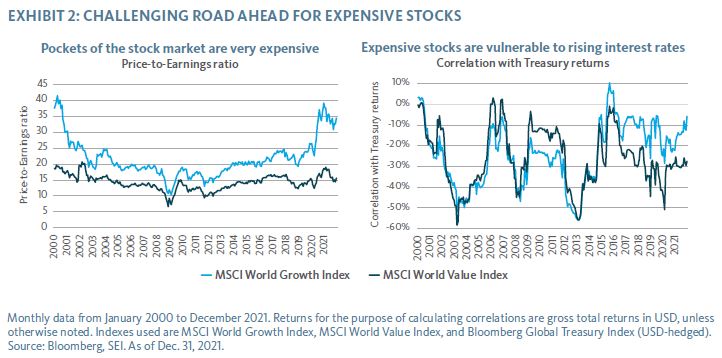

Second, bonds are not a monolith. Investors sometimes paint the entire bond market with the same brush, especially when it comes to the spectre of rising interest rates; however, there are many different areas and sectors of the fixed-income markets. For example, floating-rate debt would obviously not be nearly as impacted by a rising rate environment, and not subject to the “rates up, bonds down” principle. The breadth and diversity of fixed-income markets is good news for investors who remain concerned about the shorter-term challenges posed by higher inflation and interest rates. To demonstrate this, we looked at periods of rising inflation and interest rates over the past 20-plus years (data beginning in 1998) and examined the performance of different fixed income portfolios ranging from very basic and relatively undiversified to more fully-diversified.

The analysis in Exhibit 3 shows the benefit of additional layers of diversification—starting from a portfolio of investment-grade corporate and government bonds, then successively adding real-return bonds, high-yield bonds, and floating-rate debt. A fairly clear pattern emerges—during periods of rising rates and inflation, increased diversification improves performance, both in terms of historical absolute returns and risk-adjusted returns.

If we are indeed headed for a higher interest rate and higher inflation environment, diversification remains a fundamental principle of portfolio construction that can help, even in the world of fixed income where rising rates and inflation can be a significant headwind. You cannot paint all fixed income with the same brush:

- Inflation-sensitive bonds, typically referred to as real-return bonds, often do better when inflation rises.

- High-yield bonds can offer excellent diversification as they have higher coupon payments and less interest rate sensitivity (compared to investment-grade bonds).

- Loans are another attractive diversifier—their coupon rates float and will move higher as interest rates rise.

Diversification at every level: Total Portfolio

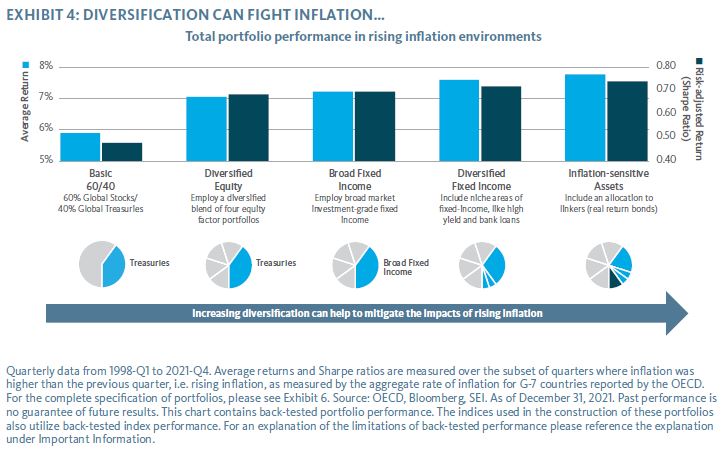

We can now evaluate how different total portfolios, with varying degrees of diversification, might cope with a higher inflation and rates environment. Taking a similar approach as our analysis of fixed-income portfolios, we focus on periods of the last 20-plus years (data beginning in 1998) where inflation or interest rates were on the rise.

Starting from a very basic, relatively undiversified “60/40” portfolio, we build toward a fully diversified portfolio—a generic representation of a portfolio that SEI would advocate for investors—as shown from left-to-right in Exhibit 4. We first move away from a market-cap-weighted equity portfolio, broadening the equity exposure to an equal-weighted blend of four factor portfolios: Quality (focus on profitability characteristics), momentum (stocks exhibiting positive price or earnings momentum), value (attractively priced stocks), and low-volatility stocks. This equal-weighted blend serves as a rudimentary proxy for active management and the general philosophy with which SEI approaches actively managed equity. Second, we expand fixed income across a broad investment-grade portfolio; third, we further diversify into niche areas of fixed income; fourth, and finally, we include inflation-sensitive assets.

Exhibit 4 shows a clear pattern of improvement in portfolio performance—a testament to the power of diversification to help deliver a better experience during rising inflation environments, in terms of historical average returns and risk-adjusted returns.

If history is any guide, a basic 60/40 balanced portfolio would be expected to underperform a truly diversified portfolio when inflation is on the rise. History suggests that properly diversified equity and fixed-income exposures, along with inflation-sensitive assets, can provide the best opportunity for gains, while also improving the expected risk-adjusted return.

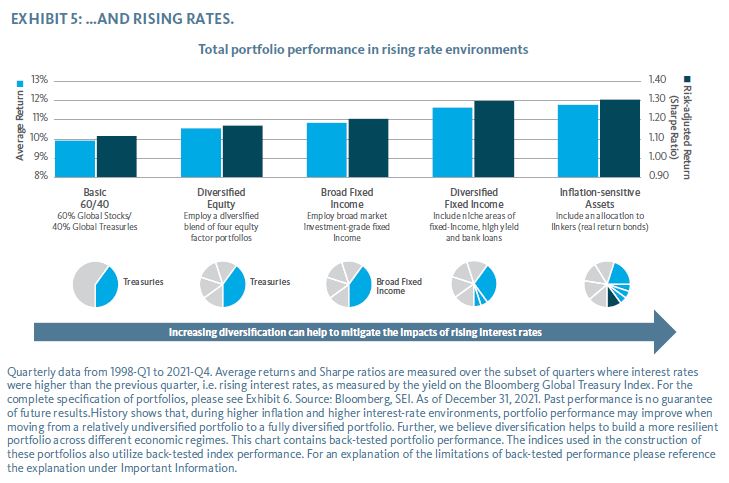

Next, in Exhibit 5, we’ll use the same framework of analysis, but focus on periods of rising interest rates. Again, we see a similar pattern during rising interest-rate environments—a significantly improved experience, in terms of historical absolute returns and risk-adjusted returns.

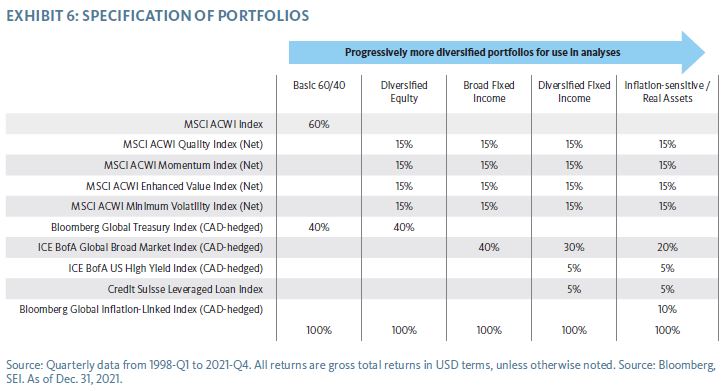

As laid out in Exhibit 6, these analyses made use of generic, global index data for the purpose of drawing some basic, but fundamental, conclusions. We chose indexes such that they provide a rough approximation of how we approach diversification and the type of well-diversified portfolios that SEI brings to bear.

Our Views and Positioning

We have demonstrated that, empirically, a properly diversified portfolio is expected to outperform a portfolio with more basic diversification. Strategic allocations are generally the most significant determinant of portfolio returns, but SEI’s investment process also includes identifying opportunities across capital markets to help enhance returns and manage risk.

We believe that the recovery from the COVID-19 crisis and its associated themes—improved economic growth, gradually higher interest rates, elevated inflation, and changes in market leadership—will continue. Fiscal responses to the pandemic have been extraordinary and significantly more coordinated than they were during the global financial crisis. Despite geopolitical uncertainty and the potential for tightening measures, the global economy is still likely to grow faster than the more-sluggish pace of recent times. This could mean ongoing upward pressure on interest rates and inflation and, at times, higher volatility. This type of market environment should favour strategic portfolio diversification, including inflation-sensitive assets, and active management, including pro-cyclical positioning within equities and other risk assets.

We believe the very-expensive areas of equity markets, as well as companies with suspect profitability characteristics, are particularly vulnerable in this reflationary environment. Many of our equity strategies have moderated exposure to expensive mega-cap stocks in favour of more attractively priced and cyclical areas that stand to benefit from the economic recovery and normalisation of historically wide valuation differentials. Generally, this includes reduced exposure to select technology and consumer discretionary stocks, especially those that appear overvalued and have lost momentum, while adding exposure to more attractive opportunities in sectors like financials, industrials, and energy.

Within emerging markets, stock selection favours semiconductors, which should benefit from strong demand, over internet-related stocks. We are approaching China with caution— reducing or avoiding exposure, particularly in the real estate sector.

Similar to equities, high-yield bonds should be supported by a recovering economy, including a default rate that is anticipated to continue falling in 2022. We also find industrials attractive in this space, and maintain a significant allocation to bank loans, which helps to reduce overall interest-rate sensitivity. Canadian fixed income strategies continue to favour corporate bonds over provincial bonds. We believe credit-sensitive assets have the potential to outperform. Within corporate credit, we have reduced positions in higher-duration sectors, which limits sensitivity to interest rates.

Diversification is key

Despite our expectation that interest rates could gradually drift higher, bonds and other portfolio hedges remain an incredibly valuable part of the total portfolio—playing a crucial role in diversification and managing the overall risk of the portfolio. Even if we assume that fixed-income returns will be lower than they have been, investment-grade bonds remain one of the few genuinely diversifying asset classes in most portfolios.

Regardless of the economic outlook, diversification remains fundamental to constructing portfolios that can be resilient across different economic regimes, including a higher inflation and higher interest-rate environment. It is always difficult to time major regime shifts in growth, inflation and rates—that is one of the reasons we believe clients should maintain proper diversification. If you are already invested in one of our well-diversified portfolios, we believe you are well positioned for this phase of the markets and beyond. If you are not invested in a well-diversified portfolio, there is never a bad time to remedy that. As always, it is important to take your goals and risk tolerance into account when making investment decisions.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the investment fund manager and portfolio manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources may include Bloomberg, FactSet, MorningStar and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

In regards to back-tested performance in Exhibits 4 and 5: Portfolio results shown do not represent the results of actual trading but were achieved by means of the retroactive application of a model designed with the benefit of hindsight. Models assume that portfolios are rebalanced quarterly and all cash distributions are reinvested. Performance does not reflect the deduction of fees.

Hypothetical portfolios also contain back-tested index performance. Back-tested index performance, which is hypothetical and not actual performance, subjects the hypothetical portfolio to further inherent limitations because it reflects application of an index methodology in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns. Past performance is no guarantee of future results.