Bond Markets: The Other Half of a Diversified Portfolio in Tough Times

Global financial markets are moving quickly. While much of the world’s focus has been on equities, fixed-income and commodities markets have been just as volatile in 2020. As always, we caution investors to not put too much credence in short-term market gyrations. Focusing on long-term goals is often the best way to avoid rash decisions that can turn out poorly in the end.

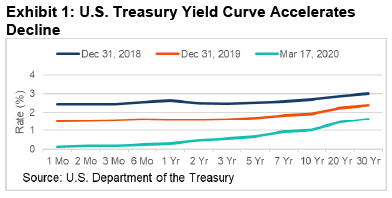

U.S. Treasurys Hit All-Time Low Yields

On March 9, the entire U.S. Treasury yield curve fell below 1.0%— all the way out to 30 years—as investors piled into U.S. Treasurys (yields and prices move inversely). This represented all-time lows for yields on all but the shortest maturities. The move was largely driven by investor risk reduction as it corresponded to the worst day for U.S. equities at that point since the most acute phase of the global financial crisis in October 2008.

Moves like this are a mixed bag for investors and consumers. First, much milder bond-market losses have helped soften equity losses in investment strategies that are diversified across asset classes, reinforcing SEI’s mantra of prudent portfolio diversification (compare, for example, year-to-date performance through mid-March on the Bloomberg Barclays Global Aggregate Index to the MSCI ACWI Index).

Lower yields can also result in falling consumer lending rates on everything from revolving credit to auto loans and mortgages. But the fly in the ointment is that lower yields also tend to signal a muted inflation outlook.

Our base case is for a period of weak inflation pressures rather than a deflationary spiral. The Treasury Inflation-Protected Securities (TIPS) market reflects this view as the 10-year implied inflation rate tumbled to 0.9% on March 13, well below the Federal Reserve’s (Fed) preferred 2% inflation target1.

1 The Fed’s preferred measure of inflation is the price index for personal consumption expenditures (PCE).

Central Banks

Central bank activity has been led by the Fed, which executed two surprise rate cuts—on March 2 and again on March 15—lowering the fed funds rate to near zero. The Fed also formally restarted quantitative easing (QE), with a plan to purchase $700 billion in Treasurys and mortgage-backed securities, as well as a range of other measures to ensure short-term funding markets remained stable.

The Bank of Canada (BoC) immediately followed the Fed’s first off-cycle cut with similar action at the conclusion of its meeting, also on March 2. The Royal Bank of Australia enacted a 0.25% cut on March 3 and the Bank of England did a surprise 0.50% cut on March 11. The European Central Bank refrained from cutting rates further into negative territory at its scheduled monetary policy meeting on March 12, but unveiled a program to extend low-cost loans to banks and announced plans to recommence purchasing eurozone bonds in another QE program. We expect an ongoing coordinated response from central banks moving forward.

Rate cuts may potentially be helpful longer term to alleviate disinflationary pressure, but they are unlikely to provide meaningful market support in the short term as they don’t immediately alleviate demand destruction, supply chain disruptions, or eliminate COVID-19.

Investment-Grade Credit

Credit spreads versus Treasurys have widened, but this is more a result of the “risk off” buying frenzy in the Treasury markets than widespread degradation of investment-grade credits. Markets have been challenged, but somewhat orderly, and we are not seeing much forced or panic selling. Still, essentially all non-Treasury spread sectors have underperformed, and these are areas where active managers like ourselves have been traditionally overweight.

The potential for downgrades, as opposed to outright defaults, appears to be more of a concern for investment-grade credit. Downgrade risk is certainly higher in some segments than others, namely BBB rated issuers and particularly within energy.

In our view, however, this has not translated into opportunities. There was no new issuance in the investment-grade corporate market during the second week of March. We are generally comfortable with the issues we hold and we do not believe we have seen complete capitulation in credit, which would represent a buying opportunity to potentially add risk. To the extent that performance has lagged, it has generally been a case of a modest underweight to duration when yields fell dramatically.

High-Yield

By most measures, high-yield bonds had held up fairly well, only falling about 2% year-to-date through March 6 (according to the ICE BofA High Yield Constrained Index). But as was the case for essentially all risk assets, losses in high-yield bonds accelerated dramatically on March 9.

Liquidity—which is generally lower for high yield than investment grade—has deteriorated, but not to the point where it has caused real issues. There has been no new issuance this month and quotes are wide. Many high-yield funds, SEI’s included, appear to have cash to cover rising outflows. Exchange-traded funds (ETFs) and credit default swaps (CDX) have also been a source of funding for outflows, limiting the need to sell actual bonds. While these are all signs of stress, high-yield markets are still orderly and manageable. Outflows would really have to ramp up for SEI or our sub-advisors to become forced sellers.

High-yield market performance has varied widely by sector, with energy suffering from reduced oil demand and a fierce battle for market share between Saudi Arabia and Russia, at the expense of prices.

2 “Oil Price Impact on Global Credit.” March 9, 2020. Morgan Stanley: Global Credit Strategy.

Unsurprisingly, leisure has also fared poorly in a world of COVID-19-related quarantines and travel bans.

Conversely, telecommunications and healthcare (which are two larger high-yield sectors) along with bank loans (which are above bonds in the capital structure, and typically BB rated floating-rate instruments) have fared much better. This dynamic may persist for a bit.

High-yield spreads over comparable U.S. Treasurys have moved considerably wider this year, some of which is deserved—particularly in the case of energy, where default risk has certainly risen. In other sectors, the spread widening has been more a case of “guilt by association.” We continue to cautiously look for opportunities, keeping in mind the lower levels of liquidity in high-yield markets and the potential for significant outflows if investors begin to panic.

There may be more “fallen angel” opportunities than usual if we see a number of downgrades of BBB rated securities; this occurs when bonds issued with investment-grade credit ratings are re-assessed with below-investment-grade ratings. Our managers have indicated that they are looking to add risk, particularly in beaten up areas, when it makes sense. Overall, we have not made any significant positioning changes to our high-yield portfolios.

Emerging-Markets Debt

The debt markets in developing regions have not been functioning as well as U.S. debt markets; still, losses have been fairly manageable. We’ve seen minimal issuance in primary markets and light trading in secondary markets with wide bid-offers. Energy has become of ever-increasing importance as approximately 40% of sovereign emerging-market issues are from net-oil exporting nations2.

Performance has been somewhat challenged in the selloff as we had a market beta of approximately 1.1. We remain underweight U.S. dollar-denominated assets, although at levels much closer to neutral than before, which detracted. Positions correlated to oil prices were relatively mixed. Although we’ve avoided major positioning changes, we have leaned into high-quality local interest-rate duration while reducing currency beta.

Commodities

Most commodities are highly correlated with economic growth, so it’s no surprise they have slumped as COVID-19 threatened global growth prospects. Oil prices have declined by more than most commodities as Saudi

Arabia and Russia have engaged in a battle for market share. Crude-oil prices plunged dramatically from March 6 to March 9 and having seemingly settled in the high-$20’s-to-low-$30’s range per barrel for now.

In our view, this level is unsustainable. We believe Saudi Arabia and Russia need prices around $70 and $50, respectively, to break even in fiscal terms. Meanwhile, higher-cost U.S. shale producers will probably not be able to sustain themselves for a prolonged period with prices this low.

While none of the major oil producers can really live with this price level long term, they can continue to pump over the short term. With the increasing importance of the energy sector across fixed-income markets, low oil prices could remain an issue for a while.

The Canadian Market

Our managers believe the Canadian dollar could decline against the U.S. dollar given the economy’s vulnerability to a demand-side shock.\

If economic growth remains sub-par, we would expect corporate spreads to move wider still. We’ve reduced corporate allocations given the increased risk to earnings combined with their high debt levels and stretched valuations.

The market has priced in fewer interest-rate cuts in Canada than in the United States, so there’s scope for more dovish surprises from the BoC. The drop in Western Canada Select prices, while slightly more resilient than Brent, spells further problems.

We also anticipate BoC rate cuts will result in a steeper yield curve as short-term rates decline faster than long-term rates.

SEI’s View

Fast-moving developments in global financial markets tend to be dominated by a focus on equities. We think the moves in fixed-income and commodities markets this year have been just as worthy of attention as the stock-market selloff.

While certainly not a cure-all, lower rates should help companies and consumers navigate the economic rough patch that will follow the widespread COVID-19 containment measures that have started to be implemented.

Two important points stand out: we urge investors, even in a market environment as turbulent as this, to keep a fixed focus on long-term goals and the plans developed to achieve them. Additionally, the different performance pattern produced by bonds at a time when stocks and commodities have tumbled should be taken as a sign that thoughtful portfolio diversification truly functions precisely as intended when investors need it work.

Glossary

Beta: Quantitative measure of the Fund's volatility relative to the benchmark used. A beta above 1 indicates the Fund is more volatile than the overall market, while a beta below 1 indicates a Fund is less volatile.

Duration: Duration is a measure of a security’s price sensitivity to changes in interest rates. Specifically, duration measures the potential change in value of a bond that would result from a 1% change in interest rates. The shorter the duration of a bond, the less its price will potentially change as interest rates go up or down; conversely, the longer the duration of a bond, the more its price will potentially change.

Index Definitions

The Bloomberg Barclays Global Aggregate Index is an unmanaged market-capitalization-weighted benchmark, tracks the performance of investment-grade fixed-income securities denominated in 13 currencies. The Index reflects reinvestment of all distributions and changes in market prices.

The ICE BofA U.S. High Yield Constrained Index tracks the performance of below-investment-grade, U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market, capping exposure to individual issuers at 2%.

The MSCI ACWI Index is a market-capitalization-weighted index composed of over 2,000 companies, representing the market structure of 48 developed- and emerging-market countries in North and South America, Europe, Africa and the Pacific Rim. The Index is calculated with net dividends reinvested in U.S. dollars.

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.