Canadian equities: 2023 outlook.

A favourable environment for Canadian equities

Slowing economic growth, stubbornly high inflation, and rapidly rising interest rates have put a damper on stock prices and indicate a recession may be on the horizon. Yet domestic equities enjoy a relatively favourable environment when compared to foreign markets. Canadian stocks should benefit from high energy prices, attractive equity valuations, and above-average inflation sensitivity. Additionally, active management may help investors profit during these volatile times.

High energy prices help stocks

Crude oil prices exceeded US$120 a barrel in June, representing a high point for the current economic cycle. In the third quarter, prices remained range bound between US$80 to US$90 a barrel most of the time. Although prices recently slipped to around US$70, there appears to be limited downside from here. While oil markets briefly rose above US$70 a barrel in 2018, the last time prices consistently exceeded these levels was 2014.

A number of macroeconomic developments have contributed to elevated oil prices. Russian oil has been sanctioned for much of the year and supply has been cut. The recently announced US$60 a barrel cap on oil, may help marginally improve supply, but ultimately this is probably more of a symbolic development than a market-moving one. The Organization of the Petroleum Exporting Countries (OPEC) theoretically has spare capacity to help offset the reduced supply of Russian oil. However, to date, OPEC producers have remained fairly disciplined and have not brought significant supply increases online. Finally, there is a global push for increased Environmental, Social and Governance (ESG) based investing. Given this, many major oil companies have focused shareholder returns on dividends and share buyback programs, rather than investing cash flows in exploration, production and development initiatives that would increase future production. This lack of investment was particularly notable during the COVID-19 lockdowns and has certainly contributed to higher prices as the world reopens following the pandemic.

The energy sector represents about 19% of the S&P/TSX Composite Index—only the financials sector is larger. By comparison, energy represents just 5%-6% of the S&P 500 Index and the MSCI ACWI Index (which measure U.S. and global stocks, respectively). As our research indicates, Canadian energy companies have been using their substantial free cash flows to aggressively buy back shares, reduce debt, and pay dividends setting up a favourable environment for domestic equities relative to foreign equities.

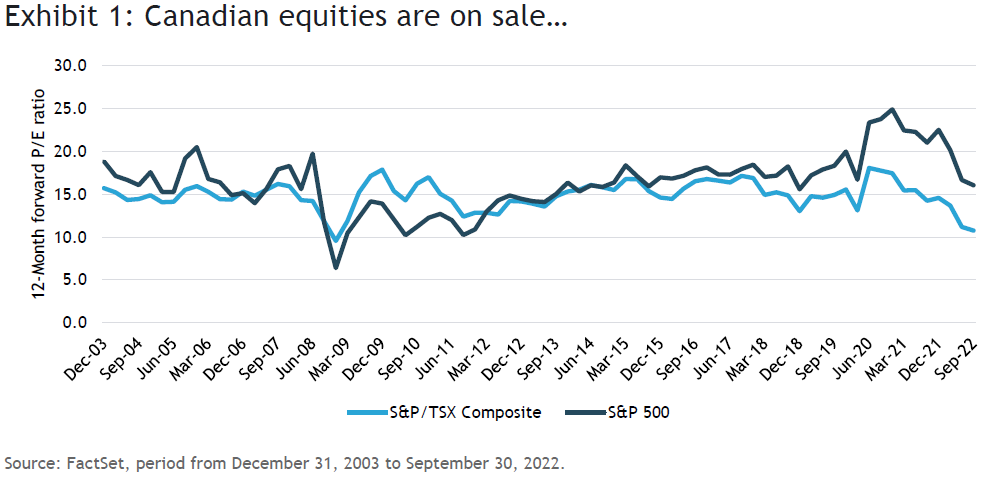

Canadian stocks are inexpensive and have inflation sensitivity

The S&P/TSX Composite Index is trading at its lowest forward price-to-earnings (P/E) ratio in two decades. In fact, the only time in the past twenty years that Canadian stocks have been this inexpensive was during the financial crisis in 2008. Canadian stocks aren’t just attractively valued on a historical basis, they are also considerably less expensive than U.S. equities (as measured by the S&P 500 Index).

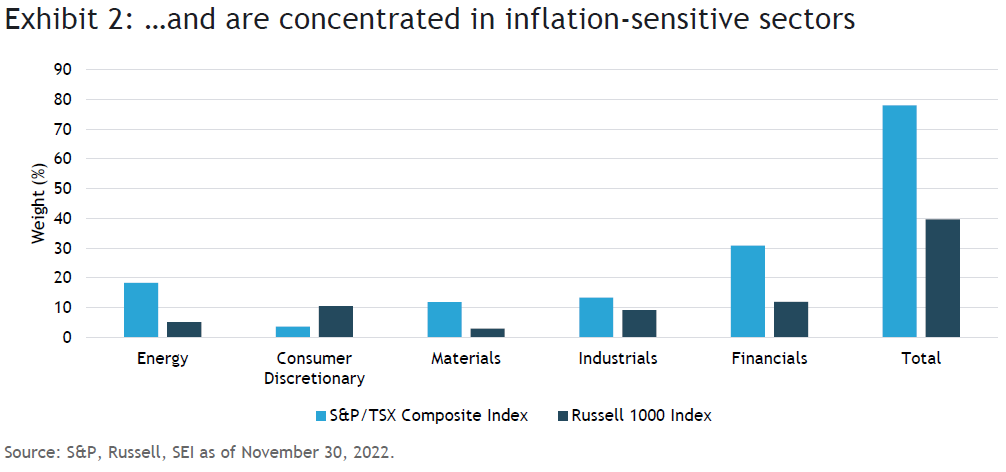

Not only are Canadian equities attractively valued, they are concentrated in sectors that exhibit a higher degree of positive sensitivity to inflation. Our research generally indicates the sectors with positive correlation to higher inflation are energy, consumer discretionary, materials, industrials, and financials. As indicated in Exhibit 2, these sectors comprise about 78% of the S&P/TSX Composite Index. By contrast, these sectors make up nearly 40% of the Russell 1000 Index, which measures U.S. large companies.

Active management has thrived amid volatility

In late 2021, global equity markets entered a fairly sustained period of increased volatility that resulted in significantly increased dispersion among the performance of individual stocks. Companies were once again being rewarded for strong fundamentals—high flying growth stocks, many of which had no earnings (and some that were actively losing money), saw their values tumble. Investors rotated away from the “stay-at-home” growth stocks that soared during COVID-19 lockdowns and into a wider range of more cyclical and value-oriented names that stood to benefit from a continued economic reopening. As Exhibit 3 shows, the S&P/TSX Composite Index is poised to possibly finish 2022 in the fourth quartile (bottom 25% of the peer universe based on returns)—the last time that happened in a calendar year was 2015. Outperformance by actively managed portfolio may be a trend that could continue for some time.

SEI fund themes

SEI’s investment philosophy is based on constructing portfolios that provide access to factors that have the potential to generate alpha—returns in excess of the benchmark—over the course of a full market cycle. As it typically does, the Canadian Equity Fund maintains positive positioning within SEI’s three primary alpha sources of value, momentum, and quality. In the current market, we continue to have a small bias towards value as stock dispersions remain attractive.

The Fund is also invested in some fundamental themes. While we hold a modestly underweight to the energy sector, the more interesting story is the underlying positioning. We continue to overweight the exploration and production (E&P) and integrated oil sub-sectors, versus an underweight to energy storage and transportation. This underlying positioning provides more exposure to energy prices and should benefit from the current elevated prices.

The Canadian Equity Fund is also underweight financials—notably banking. While banks tend to benefit from higher interest rates as their net interest margins improve, there is significant concern regarding how higher interest rates will affect the mortgage holdings. Mortgage rates are dramatically higher than a year ago, and the market for both new mortgage originations and refinancing has appeared to cool. Further, the sizable benchmark weight (21%) in these banking names that tend to have strong positive correlation with each other gives our managers pause from allocating too much of the portfolio to these positions.

We believe these themes are set to continue in 2023.

Glossary of alpha sources

Alpha source: Alpha source is a term used by SEI as part of our internal classification system to categorize and evaluate investment managers in order to build diversified fund portfolios. An alpha source is the investment approach taken by an active investment manager in an effort to generate excess returns. Another way to define an alpha source is that it is the inefficiency that an active investment manager seeks to exploit in order to add value.

Momentum: A trend-following investment strategy that is based on acquiring assets with recent improvement in their price, earnings, or other relevant fundamentals.

Quality: A long-term buy and hold strategy that is based on acquiring assets with superior and stable profitability with high barriers of entry.

Security selection: An investment strategy that employs research and judgement to uncover individual opportunities that have been mispriced by other financial market participants.

Value: A mean-reverting investment strategy that is based on acquiring assets at a discount to their fair valuation.

Glossary of financial terms

Price to earnings (P/E) ratio: Equal to market capitalization divided by after-tax earnings. The higher the P/E ratio, the more the market is willing to pay for each dollar of annual earnings.

Glossary of indexes

The MSCI ACWI Index is a market capitalization weighted index composed of over 2,000 companies, and is representative of the market structure of 48 developed and emerging market countries in North and South America, Europe, Africa, and the Pacific Rim. The index is calculated with net dividends reinvested in U.S. dollars.

The Russell 1000 Index includes 1000 of the largest U.S. equity securities based on market cap and current index membership; it is used to measure the activity of the U.S. large-cap equity market.

The S&P 500 Index is a capitalization-weighted index made up of 500 widely held large-cap U.S. stocks.

The S&P/TSX Composite Index is a capitalization-weighted equity index that tracks the performance of the largest companies listed on Canada's primary stock exchange, the Toronto Stock Exchange (TSX).

Important information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the investment fund manager and portfolio manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice. Sources include Bloomberg, FactSet, MorningStar and BlackRock.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.