Deglobalization: Opportunities in China.

Developed nations are increasingly interested in bringing jobs and manufacturing capabilities back to domestic shores. Given that nearly 30% of the world’s manufactured goods are produced in China1, a global homecoming could have a detrimental effect on the country’s economic growth. Add in the threat of geopolitics hindering the global supply chain, many investors are questioning the value of investing in China. At SEI, we see more than a billion reasons to invest there.

Deglobalization has already begun to lead to a less connected world. Rising nationalism, global supply-chain disruption stemming from the COVID-19 pandemic, and geopolitical tensions have caused many consumers to look for locally sourced goods and services. Investors, it seems, have been no different. At SEI, we have been increasingly asked about the merits of investing outside of developed markets―particularly in China.

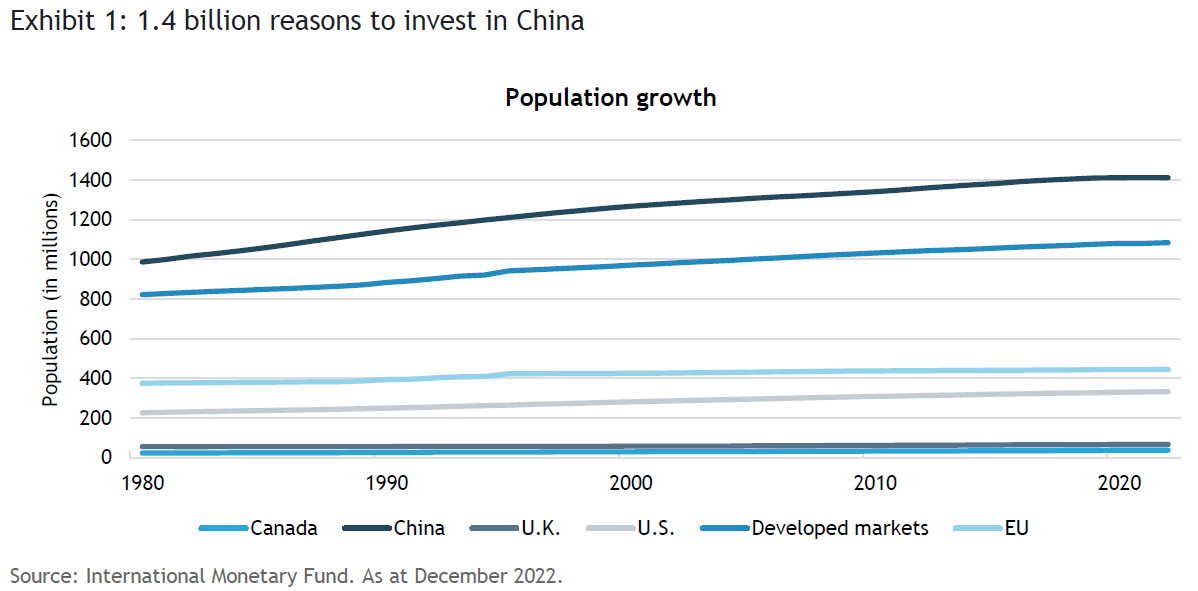

Notwithstanding recent challenges brought by the COVID-19 pandemic and slowing economic growth, China is a different story. We continue to view China as a burgeoning economic powerhouse with significance to the rest of the world2. What makes China unique? In part, it has 1.4 billion people looking to put their money to work. Even though the population is slowly declining, 1.4 billion people is greater than all developed markets combined (Exhibit 1).

Nearly 1.4 billion people spending money

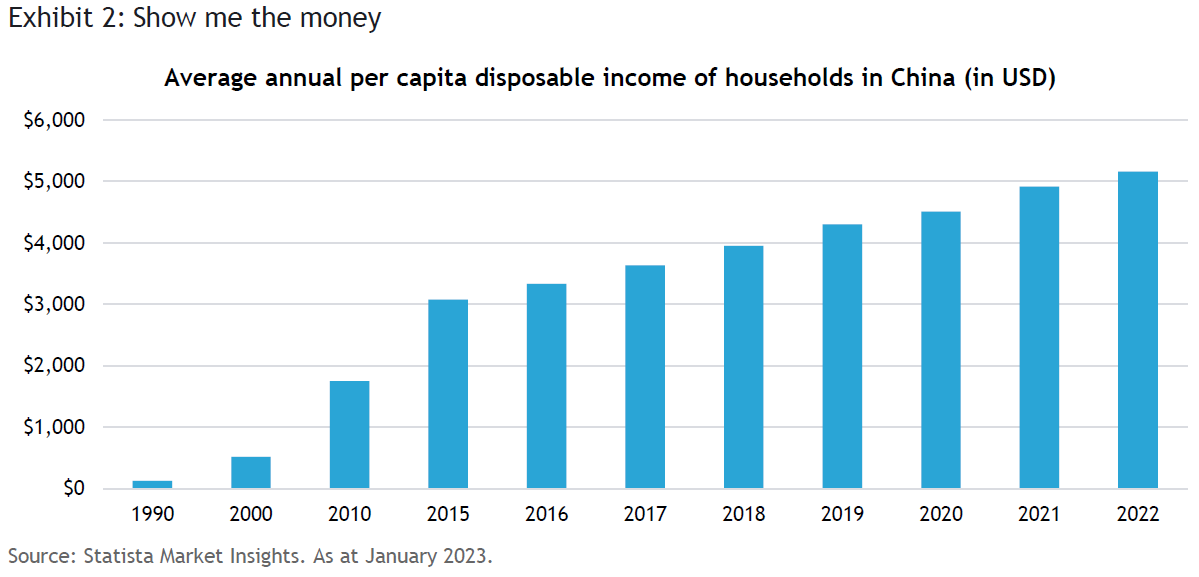

Notwithstanding a striking income gap between urban and rural populations in China, average disposable income per capita has steadily climbed, fueled in part by decades of economic reform and higher home values (Exhibit 2).

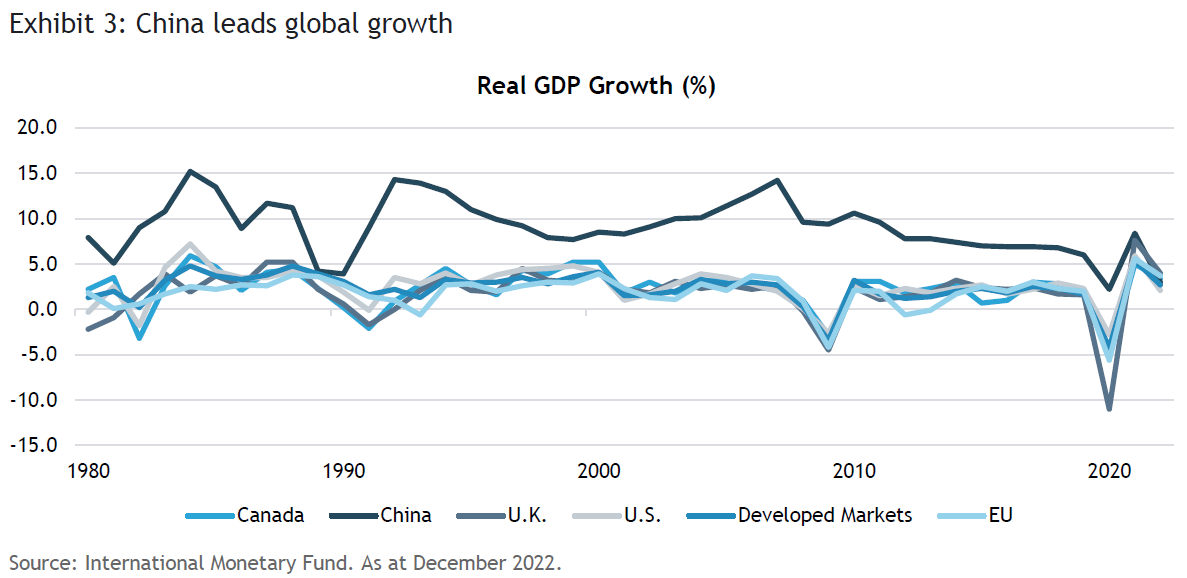

With more household income available to spend on non-essential goods and services, Chinese consumers are helping to fuel the nation’s economic growth. As shown in Exhibit 3, China’s real gross domestic product (GDP) growth, a measure of economic activity, has comfortably exceeded the collective GDP growth of all developed markets globally for the last four decades. Even if China’s growth rate were to stabilize or slow, it would still be the second largest economy in the world at $18 trillion.

Overlooked opportunities

China’s relatively elevated average disposable income has generally afforded its people higher quality of life―bringing more demand for luxury goods such as cars, televisions, cell phones, and other discretionary goods and services. While Chinese consumers have demonstrated an affinity for global brands, the data in Exhibits 4, 5, and 6 are examples that domestic Chinese brands are major market players and taking advantage of growing market opportunities.

Exhibit 4: Fully charged electric vehicles market

Electric vehicles (EV) are the future. While Tesla certainly garners most of the attention in North America’s market, China-based company BYD has an almost 30% share of the country’s EV market (in unit sales) compared to less than 8% for Tesla.

Exhibit 5: Sportswear market gaining speed

American sportswear brands Nike and Adidas have long held the largest market share of sportswear in China. Recent years have seen that share erode in favor of local brands such as Li Ning and Anta, which embody Chinese cultural traditions and national pride. In 2022, while Nike held the top spot in Chinese sportswear at 22.6%, local brand Anta Sports secured the second spot (with 20.4 %) and displaced Adidas (at 11.2%). Not far behind was Chinese manufacturer Li Ning, which increased its market share to 10.4%. If this trend persists, local brands will likely capture a bigger market share of a fast growing industry, which may present attractive investment opportunities.

Exhibit 6: Smart TVs on demand

While Japan’s Sony along with South Korea’s LG and Samsung are customer favorites in North America and Europe for binge watching shows and cheering on their favorite sports teams, the picture is different in China. Domestic brands Xiaomi and Hisense lead the way, with 14% market share each, followed by Skyworth and TCL, which each hold 11% as of 2021. Chinese customers’ preference for a more personalized and on-demand digital-media experience has boosted demand for high-quality smart, internet-enabled televisions.

In a shrinking world, look to diversify

In a world that feels to be getting smaller, China serves as a reminder that there are indeed considerable opportunities across the globe. While investors may have valid concerns about certain countries or industries within emerging markets—including China— this does not undermine the case for holding a strategic allocation to emerging market equities. The asset class continues to enjoy higher growth and attractive relative valuation over its developed peers. Whether it is semiconductors, electric vehicles, or consumer retail, deglobalization will lead to different winners in major economies around the world, and many will likely be local companies. A global portfolio may benefit from not only risk diversification but investment opportunities as well.

Glossary

Developed markets: Countries that are generally stable and have a relatively high level of economic growth. Its capital markets are developed, with a high level of regulation and oversight, a market exchange, and good liquidity in its debt and equity markets. Developed markets are mostly found in North America, Western Europe and Australasia, and include the U.K., U.S., Canada, France, Germany, Italy, Japan and Australia.

Emerging markets: Countries whose financial markets are progressing toward becoming advanced, as shown by some liquidity in local debt and equity markets and the existence of some form of market exchange and regulatory body. Typically, these markets are more advanced than Frontier Markets, but less advanced than Developed Markets.

Frontier markets: A pre-emerging market. They are typically small counties with relatively illiquid stock markets composed of thinly traded stocks.

Real Gross Domestic Product (GDP): Real gross domestic product (GDP) is an inflation-adjusted measure that reflects the value of all goods and services produced by an economy in a given year.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. There are risks involved with investing, including possible loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Diversification may not protect against market risk.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments and the use of an asset allocation service. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).