FAQ: Russian-related holdings and exposure

This FAQ is designed to help provide an update on the current Russia/Ukraine crisis and portfolio exposure to Russian-related securities.

Q. Do I have any exposure to Russian-related securities remaining in my portfolio?

A. In order to ensure that our response is clear, we need to define several terms, including:

- Russian-related securities, as defined by SEI (and aligned with the definitions used by major index providers and other data providers) are:

i) Securities listed on an exchange domiciled in Russia, Ukraine or Belarus;

ii) Securities listed on an exchange outside of these countries but that derive an extensive portion of their business from Russian, Ukrainian or Belorussian operations;

iii) Debt issued by Russian, Ukrainian or Belorussian public or private entities.

- Russian-related holdings are Russian-related stocks or bonds owned by an SEI Fund, regardless of value.

- Russian-related exposure refers to the value of the Russian-related holdings stated as a percentage of the value of the Fund as a whole.

The value of Russian securities steeply declined in the aftermath of the invasion as the market absorbed domestic and international sanctions against Russia, actions by index providers, and suspension of trading of certain Russian securities.

Any portfolio that had holdings in Russian-related equity securities when the Russian financial markets closed still owns those holdings. However, in terms of exposure, most of those holdings currently have little or no value. If your portfolio includes Russian-related equity securities that are all valued at $0, you have Russian-related holdings but your current exposure is zero. This can be seen clearly in the holdings chart where columns show 0 exposure.

It is important to keep in mind that if and when Russian financial markets reopen, equity securities that are currently valued at zero could rise in price. By regulation, security valuations are required to be based on the fair market value (FMV) of securities, and cannot be based on political views or an intention to avoid exposure to Russian-related securities. Therefore, if the FMV of Russian securities increases, then a portfolio that includes Russian holdings will also see its value rise in tandem. The portfolio’s corresponding exposure to Russia will also increase. In other words, the Russian exposure in the portfolio could increase even though there have been no additional purchases of Russian-related securities.

Q. I do not want Russian holdings in my portfolio. How can I remove them today?

A. Western countries are currently unable to sell Russian equities. Russian-related fixed-income securities face a depressed and illiquid market. Managers will look to sell positions as liquidity permits.

If it is imperative for you to remove Russian holdings from your portfolio immediately, and you own a pooled product (such as a mutual fund or ETF) that still holds Russian-related securities, you will need to trade out of that mutual fund or ETF. If you own Russia-related securities in a separate account, you will be unable to liquidate those holdings unless and until they become tradeable again.

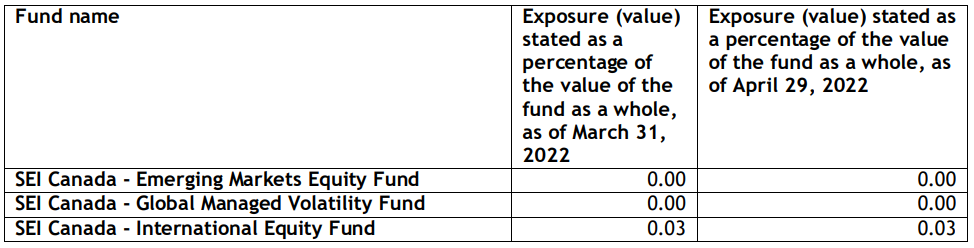

Q. Which SEI Funds have holdings in Russia-related securities and what is the current exposure (value) of those holdings in those portfolios?

A. The chart below highlights exposure at the end of March and end of April. The Funds that had Russian-related equity holdings at the end of February still have them at the end of April. As previously noted, a portfolio holding Russian-related securities that are all valued at $0, still has Russian-related holdings but the current exposure is zero because they have no value. This can be seen clearly in the chart where columns show 0 exposure.

Note: Note: If exposure increased from March to April, this is due to an increase in value of existing holdings and not the purchase of additional securities.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Diversification may not protect against market risk.

Bonds and bond funds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. TIPS can provide investors a hedge against inflation, as the inflation adjustment feature helps preserve the purchasing power of the investment. Because of this inflation adjustment feature, inflation protected bonds typically have lower yields than conventional fixed rate bonds. Commodity investments and derivatives may be more volatile and less liquid than direct investments in the underlying commodities themselves. Commodity-related equity returns can also be affected by the issuer’s financial structure or the performance of unrelated businesses.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.