The inevitable folly of forecasting.

SEI has released several papers in recent weeks on the importance of staying committed to a strategic investment portfolio even when markets are experiencing downside volatility. In this commentary, we provide additional evidence to support this view while also acknowledging some nuances involved in market forecasting and active adjustments to (and within) a strategic asset allocation.

Predicting the future is hard

You may have heard an apocryphal quote along the lines of “It’s difficult to make predictions, especially about the future.” It’s been attributed to writer Mark Twain, Nobel physicist Niels Bohr, baseball player Yogi Berra, and many others, but according to quoteinvestigator.com, it appears to have first appeared in the writings of a 20th-century Dutch politician.

While the origin story of the quote is not directly relevant to this discussion, it does provide another good example of the “Information Age” sometimes being anything but. What is relevant is its assertion, albeit tongue-in-cheek, that trying to predict the future is, like most domains of human judgment or decision-making, an incredibly error-prone exercise. There is rich literature, especially in the field of psychology, that has established and tried to model the various factors that make people and organizations prone to errors, while also exploring various methods for how we might better manage the cognitive and emotional biases underlying human fallibility. When it comes to predicting the future, we have an innate tendency to believe we can discern meaningful patterns in our environment and make sound inferences, predictions and decisions based on them2, but even professional forecasters are prone to wide differences in judgment and produce forecasts that rarely, if ever, prove accurate. However, there is some room for nuance, and we’ll close by discussing the role that judgments about the current and future states of economies and markets can play within a strategic portfolio when the risks and expense of such activities are acceptable to an investor.

Why does forecasting skill matter?

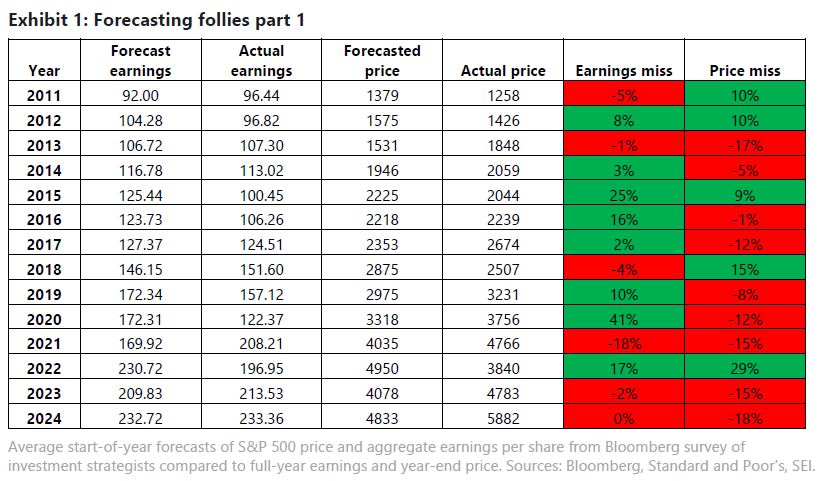

As we’ve argued in recent papers, the discomfort that arises from financial market volatility can understandably cause investors to react in ways that are more likely to undermine, rather than support, financial success. While it should be obvious that panic and loss avoidance are poor grounds for making decisions, much less wholesale changes to an investment strategy, even sober-minded professional forecasters are rarely, if ever, correct about the future. Let’s look at historical annual earnings and year-end price forecasts for the S&P 500 Index of large-cap U.S. stocks as an example. As the table in Exhibit 1 shows, the market almost never ends up where aggregate survey forecasts predict.

It’s also interesting to note that there’s no clear correlation between earnings forecasts that proved too optimistic (or pessimistic) and whether the associated price forecast for the same year proved overly optimistic or pessimistic. In half of the years shown in Exhibit 1, when strategists as a group were too optimistic or pessimistic about earnings, the market proved their price forecasts wrong in the other direction. In fact, the average-earnings-forecast and average-price-forecast misses over this period have opposite signs—strategists’ earnings forecasts were nearly 7% too high on average, while their price forecasts were more than 2% too low.

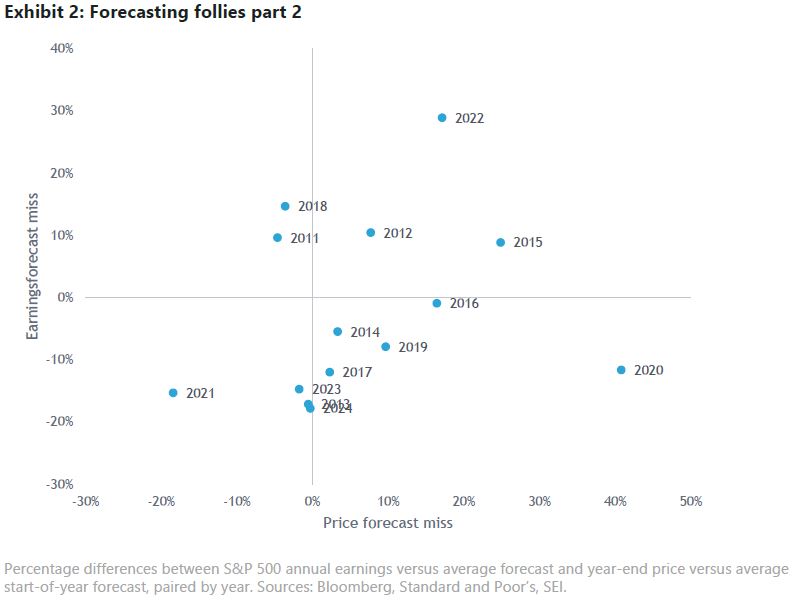

Exhibit 2 provides a graphical illustration of just how noisy the relationship between earnings-forecast and price-forecast misses has been. Annual earnings and price forecasts that missed in the same direction fall in the top-right and bottom-left quadrants; half of the observations lie in the other two quadrants.

Both exhibits drive home just how complex and behaviorally driven financial markets tend to be and provide further support for the argument that investors should not abandon a sound and diversified investment strategy when volatility arises.

Is there any room for nuance?

While the debate over market forecasting has gone on for many decades, SEI believes investors should only under specific conditions make changes to a strategic portfolio that is well-suited to their objectives and circumstances. Naturally, there is some room for nuance, specifically in the areas of active asset allocation, active investment management, and capital market assumptions.

While the track record of aggregated economic and market forecasts is not compelling4, it’s entirely possible that there is a relatively small number of practitioners who possess the skill to forecast market outcomes more accurately than other forecasters with some degree of consistency. If those practitioners can be identified, it can make sense to allocate some portion of assets to a strategy that seeks to benefit over time from their insights.

Similarly, within asset classes, active management can make sense, especially in areas of the market that are less “efficient” in terms of market fundamentals and pricing, manager competition, and crowding, etc. This certainly involves some element of forecasting, often in terms of issuer fundamentals, but at times regarding economic or market dynamics. Successful allocation to active managers also requires careful analysis and identification of practitioner skill.

In both of the aforementioned areas, identifying skill and differentiating it from luck is a challenge, and it goes well beyond just looking at performance track records. Investors need to assess the soundness of a firm’s investment philosophy, the reliability of its investment process, and the quality of its people. SEI has a long history in manager evaluation and, where appropriate for an investor, offers portfolio components like those described above. Most importantly, when including these types of components in a strategic investment portfolio, we are very careful not to allow any one of them to dominate overall risk or change desired portfolio-risk-and-return characteristics.

Finally, another important nuance is the formulation and use of capital market assumptions (CMAs) in the construction of strategic portfolios. CMAs, like most types of forward-looking market estimates, are incredibly error-prone, especially if we look at them in isolated, discrete time periods as we did with strategists’ full-year earnings and year-end price targets above. Most practitioners who formulate CMAs understand all too well that they are simply trying to come up with estimates of how various markets are likely to behave, on average, over long periods in terms of returns, return volatility, and return correlations to other asset classes to develop some insight into expected portfolio behavior and potential outcomes. To meet the requirements of most portfolio-construction processes, CMA formulation typically produces single “point estimates” of return behavior. But good strategic portfolio design is based on the understanding that these are just estimates, are inherently imprecise, and that realized market outcomes are nearly guaranteed to differ from these baseline point estimates, even for the most thoughtful producers of CMAs.

What should investors do?

At the risk of sounding repetitive, we think investors should thoughtfully construct diversified portfolios appropriate to their unique objectives, risks, and risk appetite. A well-designed strategic allocation should be able to weather periods of volatility. Of course, even the best-designed portfolios will experience volatility from time to time. However, if they have been constructed to try to diversify risks as much as possible, they should help investors achieve their goals—whether long-term or short-term—by staying invested and avoiding the folly of emotionally driven forecasts of an always-uncertain future. As some old Dutch politician once wrote, that’s really, really hard to do well.

Index definitions

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs, and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information in Canada is provided by SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company (SEI), and the Manager of the SEI Funds in Canada.

In the UK and the EEA this information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has not been registered as a prospectus with the Monetary Authority of Singapore.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.