Investment-Grade Fixed Income: An All-Weather Investment

Investors who watched as high-flying tech stocks took a hit in September may have been tempted to pull money out of the equity market. In prior years, the traditional choice for reallocating those assets would be to move them out of stocks and invest in bonds. Yet, with the yield on high-quality government bonds hovering much closer to 0.5% than 1.0%, those looking to diversify with fixed income face a tough decision: hold cash and wait for rates to rise or add to a fixed-income allocation with interest rates near all-time lows.

While SEI understands the concern, we look at the fixed-income asset class through an entirely different lens—and believe investors should too. In our opinion, investment-grade fixed income is not typically purchased in pursuit of absolute return. Rather, we view it as a hedge against volatility in the equity market; it is a hedge that has also paid a premium over cash the last several years. Think of it as insurance policy against declines in the equity market that actually pays you (albeit not much) to avoid equity market volatility.

Consider that the FTSE Canada Universe Bond Index has returned 4.3% annualized over the last five years (as of September 30, 2020), and the FTSE 3-Month Treasury Bill Index, a proxy for an investor holding cash, has returned just 1.2% during the same period.

Investment-Grade Fixed-Income: A Core Holding

In portfolio construction terms, “core” holdings usually consist of multiple underlying securities that provide access to a broad section of a given financial market in a single portfolio. This construct provides a convenient way for investors to create a diversified portfolio without having to buy a large number of individual securities. Core holdings support investing discipline by supplying a focal point when making allocation decisions and promoting a balanced process to help meet long-term financial goals.

In the fixed-income space, core funds seek to provide investors with a fixed-income allocation that may not demand much adjustment over market cycles. They typically invest in investment-grade fixed-income securities of corporate, federal and provincial issuers, including insured mortgage- and asset-backed securities. Investment-grade securities are those with an equivalent rating of BBB- or higher from a nationally recognized credit rating agency and are viewed as high-quality holdings with a low risk of default. Core fixed income offers diversification benefits when added to a portfolio of stocks. Government of Canada bonds, for example, tend to be more defensive and have historically been negatively correlated with stock market performance.

The Case for Core Fixed

An investor who avoids fixed-income holdings may have little in their portfolio to offset a decline if the equity market sees an extended flight to quality. A flight-to-quality occurs when individuals sell assets they view as riskier and purchase less-volatile investments, like government bonds. We believe this is of particular importance at this point in time as the market has been driven higher by a narrow group of stocks; an investor choosing cash over fixed income today would not only be losing portfolio diversification, but would be doing so at a time when most experts agree that there is plenty of uncertainty remaining as to the full economic impact of the COVID-19 pandemic and plenty of concern regarding the recent surge in gold and technology sector equity prices.

Canadian GDP data showed a 3.0% gain for July 2020, the third consecutive monthly gain following March and April declines of -7.4% and -11.6%, respectively. While more recent data has been positive, the 12-month average remains well below zero. Resurging cases of COVID-19 have also been reported, with hotspots in Ontario and Quebec reaching daily case rates higher than those reported during the initial wave. Localized shutdowns are likely to occur if case counts continue to rise, and unsuccessful containment could once again push health care resources to the brink. The results could be broad-based federal and provincial measures, adding even more pressure on businesses and the overall economy.

In such a scenario, long-term and intermediate-term fixed-income securities could experience greater price appreciation than investments in T-bills, cash or even guaranteed investment certificates. If the spread of COVID-19 can be contained to manageable levels, and the economy returns to more normal levels, intermediate-term bonds would still be likely to hold their value, particularly if the Bank of Canada (the “Bank”) were to continue holding its key lending rate historically low over the next few years.

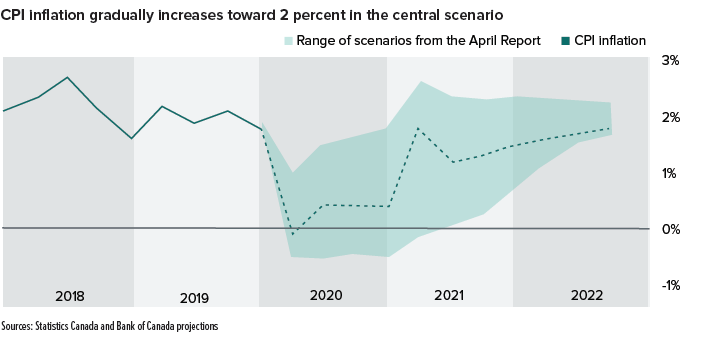

Current projections suggest that the Bank will maintain its policy lending rate for at least the next several quarters. In the central bank’s July 2020 Monetary Policy Report, the Bank confirmed that as the economy recuperates, extraordinary monetary policy support will be required and that the policy interest rate will likely be held at the effective lower bound to give the economy breathing room in order to achieve and maintain its 2% inflation target. Under the Bank’s central scenario, it estimates the mostly likely prediction of how long it might take the Canadian economy to recover to the point where its long-term target of 2.0% inflation is sustainable. Note that the following chart indicates inflation may not hit the desired 2.0% target until at least the end of 2022.

As long as the Bank’s overnight lending rate remains near zero, bond yields are unlikely to rise materially from current levels. While the U.S. Federal Reserve and the Bank of Canada have both expressed distain against the possibility of negative interest rates, we should keep in mind that on a global basis, approximately $15 trillion (USD) of negative-yielding debt currently trades on secondary markets across the globe. Collectively, these factors bode well for intermediate and core fixed-income solutions, which generate additional yield over their Federal counterparts.

Low yields will provide a headwind for the absolute level of return that bonds can generate. However, the asset class remains attractive and can be thought of as a type of portfolio insurance that pays investors to hold assets while also mitigating volatility within an investor’s overall portfolio. Let’s also not ignore the potential to generate strong positive returns if economic conditions were to deteriorate and cause intermediate and longer-term interest rates to drift even lower.

Active Management Can Help

The halt to economic activity as the COVID-19 pandemic spread in 2020 drove significant bouts of illiquidity in financial markets, as well as mass unemployment for consumers and challenging fundamentals for businesses.

While the Bank reacted by moving interest rates to an historic low and created several facilities designed to restore proper market functioning and support market liquidity, plenty of challenges remained as of the end of September―including widespread credit-rating downgrades and rising bankruptcies. However, we do not see these ongoing issues as cause for concern; at SEI, we see them as opportunities for active fixed-income investors.

We believe investment-grade corporate bonds present an opportunity to capitalize on their excess liquidity premium—mostly through new-issue debt, as new bonds coming to market have been more attractively priced than those available in the secondary market. We think this can represent a source of excess return generation through our active management.

Market Timing is Tough

Trying to time the market’s moves is challenging, if not impossible. Once an investor has exited an asset class, they have to decide another asset class to enter; additional timing decisions must be made if the same market is later reentered. Mistiming any of these entries and exits can be costly.

Instead, maintaining a diversified portfolio as part of a long-term investment plan helps investors withstand the market’s gyrations. Diversification is essential when constructing an investment portfolio. A variety of asset classes (including both equity and fixed income) helps ensure that you aren’t putting all of your eggs in one basket, and if one class dips, exposure to a different asset class can potentially mitigate loss.

While creating a well-rounded portfolio is an essential part of a long-term investment plan, it doesn’t necessarily require holding a large number of different mutual funds. Although investors may allocate some of their overall portfolios to noncore investments in an effort to improve total returns, core funds can be used as the foundation of a diversified and reliable investment strategy.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the investment fund manager and portfolio manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.