No, This Time is not Different (We Still Prefer to Buy Low/Sell High)

In rising markets, investors can become hyper-focused on past performance—even more so during bubbles and other anomalies. With headlines declaring ‘Goldilocks’ tech stocks as the new defensives1, market concentrations reaching the 99th percentile on a historical basis2, and pronouncements of the death of value investing, we re-examine the basic principles of ‘buying low’ as well as the inherent risks of ‘buying high’.

Risks of Ignoring the ‘Margin of Safety’

The founders of value investing, Benjamin Graham and David Dodd, noted that ‘the margin of safety is always dependent on the price paid’3. In other words, paying a low price generally increases an individual’s odds of making a profitable investment.

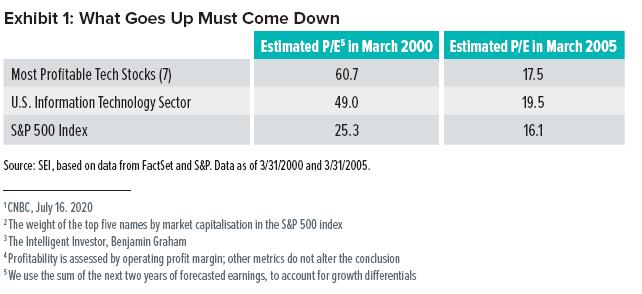

The risk of ignoring this basic principle was vividly illustrated during the tech bubble of 1999-2000. To make the comparison more relevant to today’s market, we examined the seven most profitable4 companies of the time within the U.S. Large Cap Technology sector (the ‘FANGs of 2000’), namely Microsoft, Cisco, Intel, Oracle, EMC, Applied Materials and Texas Instruments. We deliberately avoided frothier ‘dot-com’ segments; the stocks we chose were recognised leaders in their field, with strong earnings and sales growth, high barriers of entry, and innovative edges.

Of course, greatness alone is not a sufficient characteristic for a successful investing strategy. With valuations 2-3x of the broad equity market, a lot had to go right for those firms—and a lot had to go wrong for others—to justify such premium pricing. Indeed, a lot did go right. 20 years later, these companies are still around and, arguably, are still thriving.

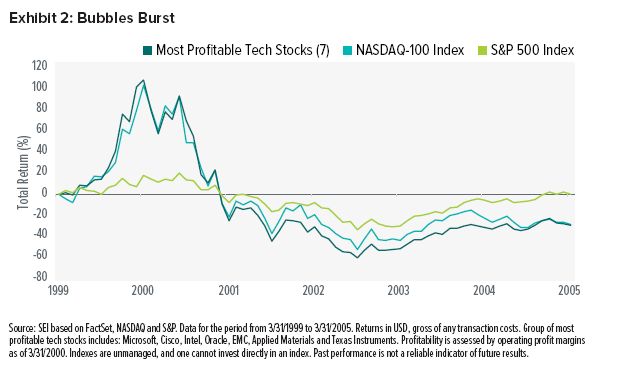

As shown in Exhibit 2, the same could not be said for the fortunes of investors in these companies. During the five years that followed the bursting of the tech bubble, valuations of these stocks came down to a reasonable premium and inflicted severe losses on investors who bought at or near the top of the market. Even when a lot went ‘right’, chasing performance by overpaying led to poor outcomes for the investors.

History Rhymes

As the old saying goes, history doesn’t repeat itself, but it rhymes. What parallels can we draw from the tech bubble experience? Plenty. For starters, today we are witnessing almost verbatim media headlines. ‘Dot com’ has been replaced with ‘cloud computing’, while ‘growth’ has been augmented with ‘quality’; ‘value’ now appears to be relegated to ‘junk’. These are all plausible, in fact, reasonable arguments. Except for one little problem: What might happen when prices for greatness revert to a more typical premium?

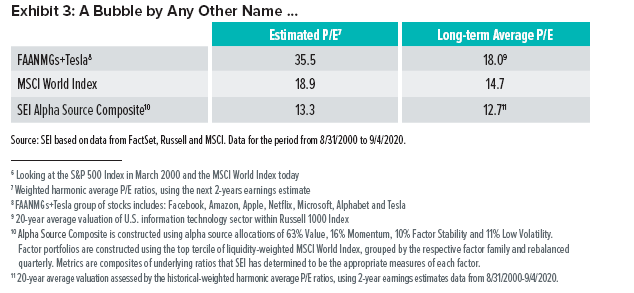

Looking at the valuations in Exhibit 3 below, we can see both good and bad news. First, we note that at 19x the next two years’ earnings, the equity market now is not as expensive as it was in March 20006. Likewise, the ‘greats’ of today are expensive but not as bad as their peers 20 years ago. Unfortunately, ‘my bubble is smaller than yours’ is not a valid argument for overpaying. A bubble is still a bubble.

The Cost of Greatness

Let’s examine what might happen when we return to normal. By ‘normal’, we don’t mean that the COVID-19 crisis will dissipate. We mean that optimistic earnings forecasts will be realised, regulatory scrutiny will remain scarce, and innovation in the rest of the economy will disappear. We’ll assume that the Yahoo of today will not face competition from the Google of tomorrow. And we’ll deliberately disregard inevitable competitive threats, a foolish conjecture as investors in Nokia, Intel and IBM would likely attest. Making all of these unreasonably rosy assumptions, we then analyse what might happen if multiples for the same good earnings revert to more reasonable premiums.

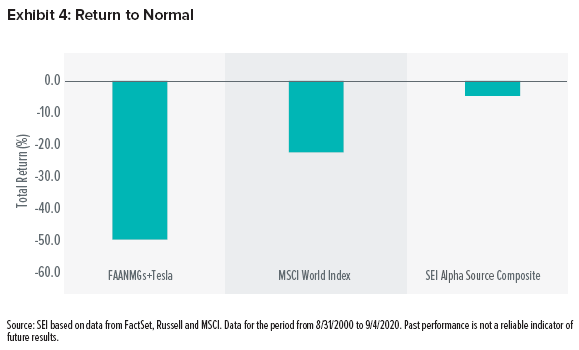

The picture implies that, either earnings growth over the following few years will significantly surprise on the upside (over already generally optimistic projections from the analyst community), or returns are going to be disappointing, not just for FAANMGs but the broader MSCI World Index as well. Relying on the U.S. Federal Reserve to further reduce the price of money and elevate valuations is also less plausible in a zero-interest-rate environment.

A More Prudent Approach

There is no silver bullet for long-term investment success. The unwinding of today’s bubble is unlikely to follow the precise pattern of the 2000s. We recognise relentless competitive forces at play, not only at the single-stock level but also at the alpha source and style level. In a world of ever-evolving ‘unknown unknowns’, diversification is the only prudent solution, as cliché as it sounds. To avoid the damage that Yahoo, Nokia and IBM saw in the 2000s is to ensure sufficiently broad allocations to other stocks, industries and asset classes. Whenever the fashion of the day favours a few, we remain sceptical and look elsewhere.

Our active strategies are based on processes that don’t rely on heroic assumptions. Our earnings advantage, or, to quote Benjamin Graham, ‘margin of safety’, is likely to cushion some of the blow when the normal becomes normal again. And no, we don’t believe that this time is different.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affiliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and the information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from qualified professionals. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Information contained herein that is based on external sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.