Rising Rates and Bond Markets: Keep Calm and Clip On

Global bond yields have risen over the past year, with the average yield on the Bloomberg Global Aggregate Bond Index climbing by roughly 40 basis points over the 12 months ending December 31. Recent changes in Canadian bond yields have been even more dramatic as the average yield for the FTSE Canada Universe Index increased 80 basis points over the same period. The rise in yields has been driven by several factors, including the rollout of COVID-19 vaccines and a gradual reopening of the economy. The impact has led to significant increases in economic growth for most developed nations. As more countries reopen their economies, extraordinary monetary and fiscal stimulus has not only allowed economies to weather the impact of the pandemic but has fueled a rebound in employment leading to an imbalance between demand-driven growth and supply. Not only has this pushed prices higher in key economic sectors such as food, housing, and energy, but surging demand has led to bottlenecks in the supply chain and further exacerbated the situation. Headline inflation rates have clearly moved higher, and expectations for abnormally high inflation remain heightened, adding further upward pressure on yields.

With bond prices moving inversely to yields, some fixed-income investors are understandably concerned about the possibility of falling bond prices. Experiencing a price decline in any asset can be disconcerting. This is why SEI focuses on helping clients build well-diversified investment solutions to help protect against downside risks and market volatility. Maintaining exposure to core and investment-grade bonds plays a critical role in managing these risks even in the unlikely case of a longstanding move to significantly higher bond yields.

Why Own Bonds?

With interest rates still at historically low levels, some investors are asking whether there is still a role for core, investment-grade bonds in a diversified portfolio. We believe there is. First, bonds can provide meaningful income generation. While the current income received from bonds is quite low compared to history, we believe the relationship to cash and yields on riskier assets are within reason as compared to those of the last 25 years.

With no other consideration than the comparison of current yield levels to historical averages, an investor might conclude that core bonds are overvalued. However, just because core bond yields are at historic lows, they aren’t necessarily overvalued owing to where the yields on other asset classes sit (the opportunity cost). An investor who desires greater income might have to take on additional risk/duration/illiquidity. As with any portfolio repositioning, the change in exposure comes with tradeoffs that should be balanced with other goals and objectives. In other words, we think that the current level of core bond yields can be justified given everything else in the current state of financial markets.

Additionally, bonds still provide valuable diversification benefits. Because the returns on high-quality bonds tend to behave differently than the returns on riskier, growth-oriented assets like stocks, they can help lower the volatility of an overall portfolio. In other words, in an optimal investment portfolio, some assets should rise when other assets fall—which is often what happens in the relationship between stock and investment-grade bonds1.

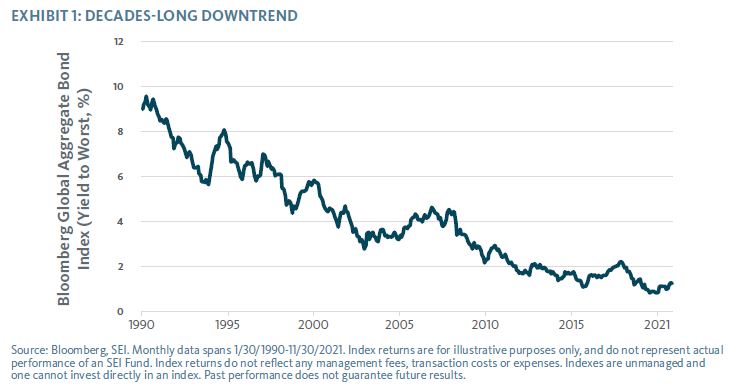

A Multi-Decade Tailwind

A nearly four-decade-long downtrend in global interest rates, as shown in Exhibit 1, provided a longstanding boost to bond returns. The broad downtrend in global rates continued into mid-2020, falling to record lows in many countries as the global pandemic took hold. Interest rates have since moved higher, thanks to strengthening growth and inflation outlooks fostered by forceful policy measures and the arrival of effective vaccines. Thus, the more interesting (and perhaps pressing) question is how serious the risk of higher interest rates is to future returns on investors’ bond holdings.

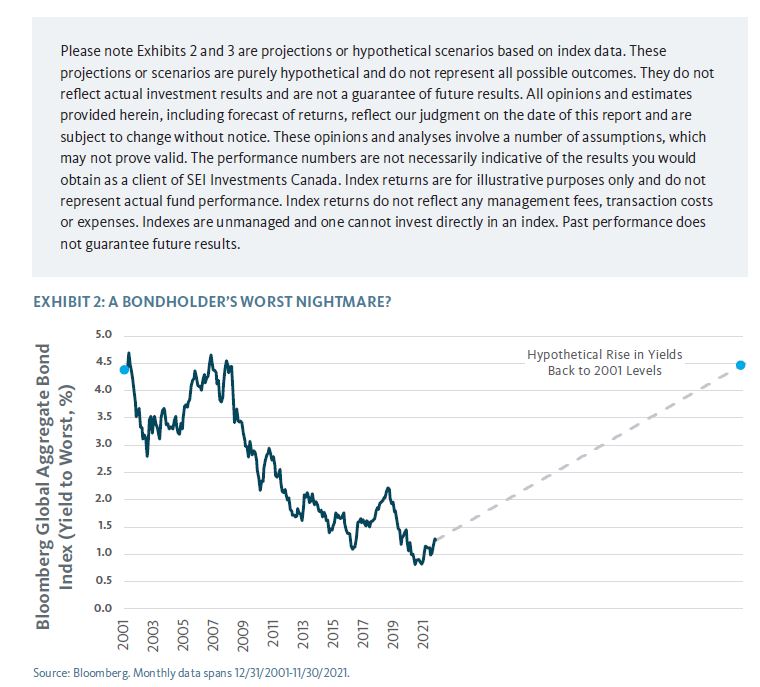

Prices Matter, But Cash Flows Matter More

To help investors observe this risk, we examined the components of global bond returns over the last 20 years. SEI then analysed what returns might look like if we saw the last two decades of falling interest rates reverse course over the next 20 years (Exhibit 2). Interestingly, the additional boost to core bond returns from rising bond prices (falling interest rates) was just over one-tenth of the total annualized return on the Bloomberg Global Aggregate Bond Index. While that’s not insignificant, it does highlight that scheduled interest payments are a far more important factor in the total return earned from bonds.

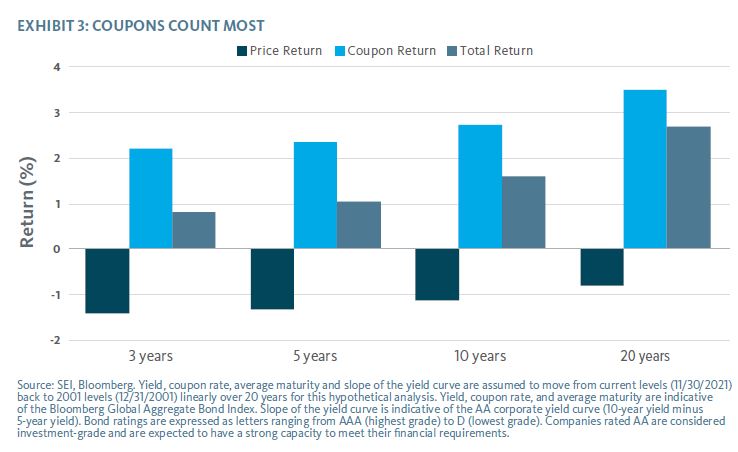

Courtesy of those recurring interest payments, simulated bond returns on the same index would still likely be positive even if interest rates reversed course in a straight line for the next 20 years. As shown in Exhibit 3, the impact of rising interest rates on bond prices would impose a relatively small drag on overall returns. More importantly, the benefits of reinvesting cash flows, interest payments and principal repayments into higher-yielding bonds over time could easily overcome this.

The Takeaway: Hold onto Your Bonds

To reiterate, SEI does not expect bond yields to retrace the decline of the last 20+ years. However, our analysis highlights the importance of investors remaining resolute as a healthier economy and more persistent inflation elevate the potential for longer-term rates to rise further. Investment-grade bonds should not only be able to produce positive returns in a multiyear period of moderately rising interest rates, but they should continue to provide valuable diversification, overall risk management, and income benefits as well.

Glossary

Basis point is equal to 1/100 of 1% and is generally used to express differences between interest rates.

Downside risk explains a worst-case scenario for an investment.

Duration is a measure of a security’s price sensitivity to changes in interest rates.

Fiscal policy refers to the use of government spending and tax policies to influence economic conditions.

Investment-grade bonds are believed to have a lower risk of default and receive higher ratings by the credit rating agencies.

Monetary policy refers to the actions undertaken by a country’s central bank to control money supply and promote economic growth.

Yield is the amount that a bond pays each year in interest as a percent of its current price.

Yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating.

Yield to worst is a measure of the lowest possible yield received on a bond that does not default.

Index Definitions

Bloomberg Global Aggregate Bond Index measures the return of the global, investment-grade debt market.

FTSE Canada Universe Bond Index measures performance in the Canadian domestic bond market and is the most widely used performance indicator of marketable government and corporate bonds for Canada..

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.