SEI forward.

Tales of the tape (YTD as of 3/31/2023): U.S. equity +7.50%, Global ex-U.S. equity +7.00%, Global treasuries +3.08%, U.S. 10- year Treasurys +3.70%, Commodities -5.36%

Notables (YTD as of 3/31/2023): U.S. banking sector -17.26%, U.S. technology sector +21.82%, Equal-weight S&P +2.93%, Gold +8.11%

Uncertainties abounded in the first three months of 2023 as markets digested the impacts of an unprecedented global tightening cycle, banks failures, and forced mergers. Somewhat surprisingly, despite this laundry list of market headwinds, investors broadly finished the quarter no worse for wear. Pockets of pain were clearly felt for sure, but the story of the quarter is one of resilience and divergence.

Mega-cap technology stocks acted like a new flight to quality asset as banking concerns erupted in March, providing a ballast to both U.S. and global-developed equities while the banking sector as a whole was painted with a broad negative brush. Credit was relatively well behaved despite resurfacing memories of 2008 while U.S. Treasurys and gold played their typical roles as safe ports in the storm.

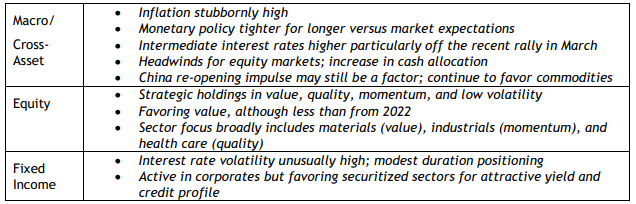

Outlook

Looking forward, we see opportunities and risks in both the resilient (equities, credit) and the divergent (value, rates). Specifically, we are fading the resilient and leaning into the divergent.

From a top down perspective, we remain cautious on equity markets. The strong rally in growth stocks at the end of the quarter prompted us to modestly raise cash levels relative to U.S. large cap equities. We see the impact of higher rates and tighter policy expanding beyond the highly sensitive (i.e. housing) sectors into the broader economy. We also question the highly reactive central bank moves expected by the market. Investors have become Pavlovian in regard to central bank stimulus—equity markets fall, central banks cut rates. We question whether this reaction function will remain in place in a regime of stubborn inflation rates. In other words, we see headwinds for the equity markets and do not expect central banks to come to the rescue as they have in the past.

Within equities we continue to focus on our core approach; favoring high quality companies with positive earnings momentum at reasonable valuations. Value specifically remains a more focused exposure (although is, in general, slightly down from 2022) due to our view that valuation spreads, or the dispersion between stocks representing high and low measures of value, remains historically wide. Our positioning is also supported indirectly by our top-down views on stubborn inflation and less reactive central banks which also suggests higher interest rates in the near term. Our sector positioning, as a reminder, is a result of our stock selection and our alpha source approach; we focus our portfolios on value, quality, momentum and at times, low-volatility stocks and avoid other exposures, such as speculative growth names. Broadly, our equity shareholders will currently find our portfolios leaning into financials and materials given our preference for value, industrials given our positioning in momentum, and health care via our quality and low-volatility positioning.

Regarding fixed income, interest rate volatility has been historic in nature during the first quarter which has prompted some caution regarding duration exposure. Our top-down view is for higher rates based on our economic outlook and the recent rally in the space which we see as overdone. Our portfolio positioning, however, remains modest and more mixed—from slightly long to slight short duration.

As previously noted, credit markets have held up relatively well, however, similar to our directional view of equity markets, we see benefits in a more defensive posture. Our investment-grade portfolios continue to shy away from below investment grade and have been favoring more securitized sectors, such as asset- and mortgage-backed securities to attain attractive yields and a better credit profile. Default rates have been running below trend and favorable maturity profiles may enable a more stable environment even in challenging economic times. That said, our high-yield portfolios have also been selectively upgrading exposures as the current yield environment doesn’t warrant stretching for extra basis points.

Lastly, while the reopening of China was greeted with much fanfare to close out 2022, investors appear increasingly skeptical thus far in 2023. We remain cautiously optimistic here that the economic impact of from China could outperform current expectations. This near term potential for robust economic growth out of Asia, coupled with our longer term focus on structural under investment in several sectors leads to our continued, favorable view of commodities.

In closing, while the first quarter of the New Year was a challenging one, we believe our portfolios are well positioned going forward.

Summary views

Indexes

U.S. equity=S&P 500 Index, Global ex-U.S. equity=MSCI ACWI ex-U.S. Index, Global treasuries=Bloomberg Global Treasury Index, 10-year Treasurys=ICE BofA Current 10-year U.S. Treasury Index, Commodities=Bloomberg Commodity Index, U.S. banking sector=S&P Banks Select Industry Index, U.S. technology sector=S&P Information Technology Sector Index, Equal-weight S&P=S&P 500 Equal Weighted Index, Gold=S&P Goldman Sachs Commodity Gold Index.

Important information

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755- 1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorized and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.