SEI Manager Research: Our Solution to the Peer Group Problem

Performance is the most ubiquitous and common piece of information used to assess the success of an investment strategy. Most investors use it to decide whether to hire or fire a manager.

In our view, however, it can also be deceptive, especially when there are thousands of investment products from which to choose1.

One popular method of simplifying hiring and firing decisions is to designate a peer group or universe to compare manager performance. Databases such as eVestment, Morningstar and Lipper classify investment strategies into one or more peer groups, such as Large Growth or Foreign Blend.

The problem

Off-the-shelf peer universes may seem to be the most convenient solution for comparing investment managers. However, we believe that they are not usually the most accurate way to assess performance. Assigning strategies to peer groups is not as simple as it sounds. Classifying a manager in the wrong peer group may lead to false conclusions about the manager’s skill—or even expectations of when the manager may perform well or struggle, which may lead to poorly-timed firing or hiring decisions.

We see three issues with using off-the-shelf peer groups.

- Most are often overly broad; a given group may have hundreds of managers who really are not very similar.

- Peer-group classifications may be based on return patterns or (in some cases) the manager’s own judgment, which may lead to inconsistency.

- A significant number of managers don’t fit nicely or easily into the traditional style boxes of value, growth and core (or blend), forcing comparisons that don’t make sense.

Our solution

Instead of relying on third-party off-the-shelf peer universes, we have built our own.

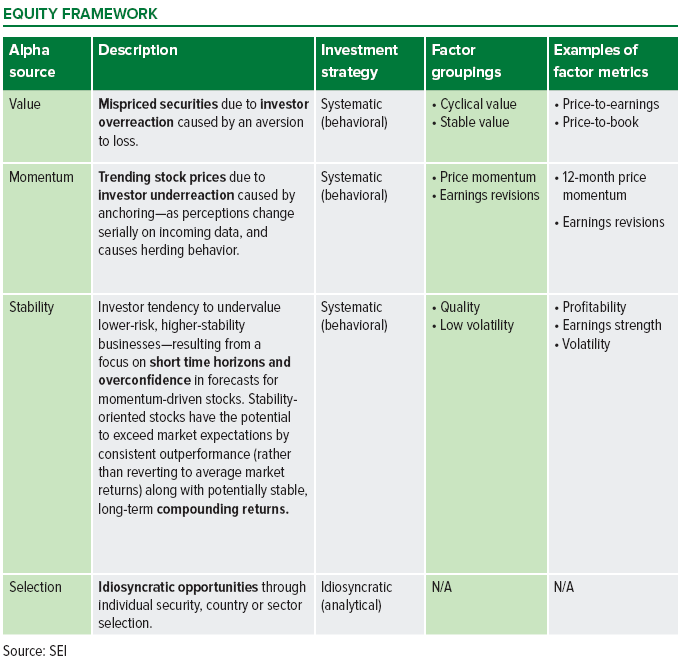

We engage in ongoing research to identify the factors that contribute to a portfolio outperforming its benchmark, which are often referred to as drivers of excess return—or alpha sources. We do this through a combination of conducting proprietary market analysis and modeling, engaging with external investment managers and reviewing third-party academic research.

Our alpha sources fall into two broad categories: systematic (which are tied to quantifiable historical market inefficiencies) and idiosyncratic (which are generated by unique insights of traditional active managers).

We proxy alpha-source drivers through a series of closely correlated factors (in terms of both risk and return) that depict common characteristics associated with that alpha source.

Below is a table that includes examples of our alpha sources and factors.

SEI Manager Research leverages its insights, understanding and implementation of alpha-source drivers to create bespoke peer universes that share common portfolio characteristics of actual manager holdings—not manager judgment or past performance. These holdings provide portfolio-level factor exposure data, which is used in a proprietary decision-tree algorithm to determine the most appropriate peer group for each manager.

We believe a holdings-based approach is the soundest way to create peer group cohorts because it reflects the decisions that are within a manager’s control. The manager determines what securities it buys or sells and the characteristics those securities embody. Returns are not something within a manager’s control, and relying on self-selected descriptions does not yield empirical consistency due to a lack of a common framework.

The factors we use are those that we believe are the most closely associated with our systematic alpha sources. We conduct analysis on a regular basis to help ensure our peer group universes reflect the most recent data available.

How this benefits our clients

Using our own peer groups—rather than the broader off-the-shelf peer groups—allows us to view the investment manager universe through an alpha-source lens instead of a traditional style-box lens.

Our peer universes tend to be much narrower than off-the-shelf alternatives, which means that the investment managers in each universe tend to be highly similar. Thus, we can more accurately compare manager performance and determine whether a manager’s performance is the result of luck or skill.

This approach helps to better distinguish beta from alpha, which can be useful in assessing appropriate fees to pay investment managers.

Our peer group work also allows us to refine our due-diligence efforts, gaining efficiency in focusing on key aspects that matter most to the manager’s investment philosophy and process.

Our proprietary factor analysis uses data that reach back by more than a decade. The resulting information provides us with insight into a strategy’s consistency (or lack thereof) in style over time. Knowing how an investment manager’s portfolio has changed over the years through various market environments helps us to understand how it may change going forward. This allows us to more accurately set performance expectations and better communicate our beliefs about how a manager should perform in a given environment.

Finally, our peer universes provide valuable information about investment managers that are not currently active on SEI’s platform. This knowledge can help us make portfolio construction decisions when working with clients who had previously invested with managers with whom we are unfamiliar.

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information provided by in the U.S. by SEI Investments Management Corporation.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alpha beta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

For full details of all of the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact your fund adviser (South Africa contact details provided above) for this information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.