SEI is Staying Calm COVID-19 Crisis: Asset Allocation Review

Investors have just come through one of the most challenging quarters in history. The speed of declines in equity markets and the corresponding volatility were unprecedented. Moves in the U.S. Treasury market were also unprecedented and left fixed-income markets in uncharted territory. Prices for crude oil flat out collapsed. There were few places to hide, and most of the areas favored by active investment managers like SEI were hit the worst.

We always preach the values of well-diversified portfolios with balanced risks across a wide range of sources. Over full market cycles (a bull market, a bear market and return to a bull market), which can sometimes run a decade or longer, we are highly confident in this approach. Of course when crisis strikes, as COVID-19 did, even the best laid plans can falter over short-time intervals. With that in mind, we do not believe that now is the time to make panicked, rash investment decisions. Accordingly, we aren’t going to make any strategic asset allocation decisions based on a few weeks or months of performance. That stated, we believe it may be helpful to review the first quarter from an asset allocation perspective.

Asset Allocation Principle: More Diversified Equity Exposures

Implementation: Small Cap, Emerging Market Equity, Reduced equity home country bias

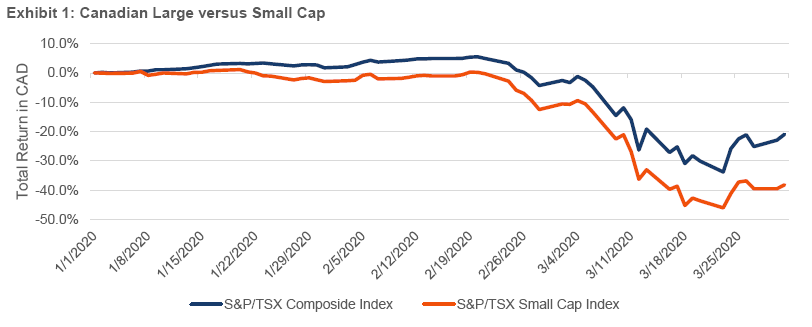

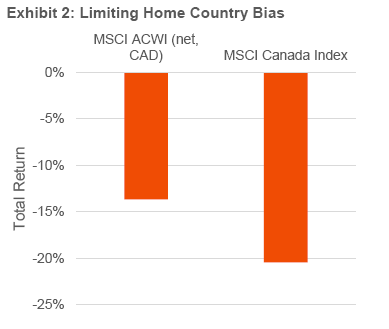

Performance discussion: As equity market returns were dominated by large companies, particularly in the U.S. technology space, more diversified exposures lagged concentrated U.S. or developed market large-cap indices. Within Canada, large-caps stocks outperformed small caps by more than 17% during the quarter. Emerging markets (as measured by the MSCI Emerging Markets Index Net) underperformed developed markets (as measured by the MSCI World Index Net) by over 2.5% during the quarter. Home country bias was a mixed bag: it benefited investors whose home markets outperformed (such as the U.S.) while detracting for investors whose markets lagged (such as the U.K. and Europe).

Strategy-level impact: Assuming a 6% allocation to small cap (roughly 10% of the 60% held in equities within a 60/40-like portfolio) split evenly between Canadian and US small stocks, this would have detracted 80 to 85 basis points relative to an all-large-cap implementation. Assuming a similarly-sized allocation to emerging-market equities, that exposure would have reduced returns by roughly 15 basis points. The effect of home country bias will vary both in direction and size depending on the investor’s home country and the magnitude of the bias.

Why this is an important strategic holding in our Strategies: Even though we try to limit our Strategies’ concentration in equity risk, equities remain a major driver of portfolio risk and return. Consequently, we seek to diversify our equity holdings as much as possible. Failing to do so would expose Strategies to unnecessary risk without being potentially rewarded with higher expected returns. Small-cap and emerging-market equities are integral components of the global capital markets and offer the potential for both higher returns and diversification relative to developed large-cap markets. Global diversification (as opposed to the heavy home country bias implemented by some of our peers) seeks to minimize exposure to any single country, economy or geopolitical situation. By spreading our Strategies’ equity risk across the globe, we are able to harvest long-term growth in equity markets without undue exposure to individual countries where markets are often dominated by a few issuers or sectors. Again, this diversification is designed to maximize expected return at any given level of risk.

Asset Allocation Principle: Use of Low-Volatility Equity

Implementation: Global Managed Volatility

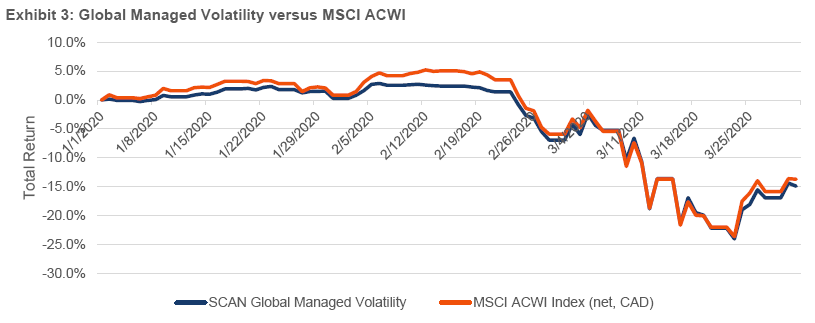

Performance Discussion: Given the low-beta nature of managed volatility, we generally expect it to outperform in sharp equity market downturns. In the first quarter of 2020, however, low-volatility equities declined more than would be expected in such a sell-off.

Global Managed Volatility lagged the MSCI ACWI Index – Net during the quarter. This performance is explained by a few unusual phenomena—namely, the dramatic underperformance of small-cap stocks (managed volatility is diversified across the size spectrum, whereas the benchmarks are concentrated in larger names) and the dominance of mega-cap U.S. technology companies. As the technology sector is not generally characterized by low volatility, it is a much larger portion of the full-beta benchmark than of the managed volatility funds. So, when technology outpaces every other sector, managed volatility can lag.

Strategy-level impact: Our impact analysis compares the managed volatility fund to a 70%/30% combination of its benchmark and cash, with the split determined by the approximate beta exhibited by the fund over the last five years. Assuming a 25% allocation to managed volatility, this implementation accounted for up to 125 to 150 basis points of reduced performance relative to the 70/30 beta proxy (as measured by the MSCI ACWI - Net and the FTSE Canada 30-Day T-Bill Index) during the quarter.

Why this is an important strategic holding in our Strategies: SEI was a pioneer in low volatility investing. We believe that allocating to managed volatility affords our investors similar expected returns with potentially meaningfully lower risk compared to the benchmark market. The cost associated with this potential advantage is tracking error: in order to harvest the benefits of managed volatility, investors must be comfortable with these funds behaving differently than cap-weighted benchmarks, including the potential for periods of large outperformance and underperformance. Given the consistency with which managed volatility has cushioned losses during other market declines and the fact that the risk reduction did not come at the cost of materially lower returns, we believe that the trade-off between improved risk-adjusted returns and higher tracking error remains attractive.

Asset Allocation Principle: A Modest Amount of Inflation Protection Securities

Implementation: Inflation-Linked Bonds

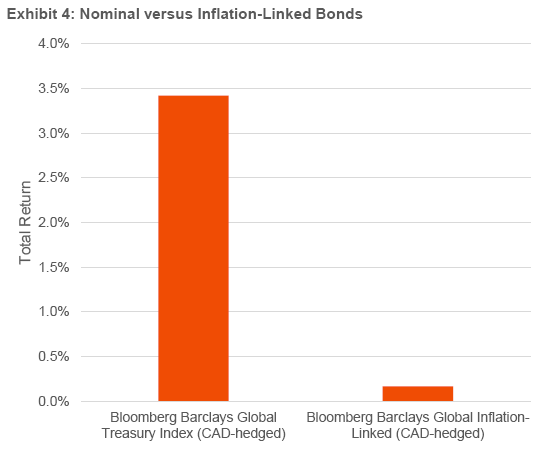

Performance discussion: Inflation-sensitive assets suffered substantially during the quarter as inflation expectations cratered, driven lower in part by the steep drop in commodity prices. While some level of decline is to be expected as aggregate demand fell due to virus containment measures, this period was highly unusual in that this demand destruction was accompanied by adverse supply moves. Somewhat paradoxically, in the face of plummeting oil prices, Saudi Arabia and Russia entered a price war in early March, exacerbating the downward pressure on oil and other inflation-sensitive assets as they flooded markets with excess oil. Global inflation-linked bonds underperformed nominal bonds by over 300 basis points over the quarter.

Strategy-level impact: Assuming a 5% allocation to inflation-linked bonds, this holding would have detracted roughly 15 basis points compared to a portfolio of nominal bonds.

Why this is an important strategic holding in our Strategies: Most traditional “stock/nominal bond” portfolios carry little to no inflation protection. Accordingly, an unexpected spike in inflation may result in unsatisfactory real (inflation-adjusted) returns. It is clear that nominal bonds, with their fixed coupon and principal payments, are subject to the risk that unexpected inflation will erode their purchasing power over time. Less obvious, but at least as meaningful, is the sensitivity of equity prices to unexpected inflation shocks. Central banks around the globe agree that inflation poses a threat to real economic activity and, by extension, to corporate profits and equity returns. Because the goal of an investment portfolio is to support spending at some future time, the risk that the value of that spending will be eroded by inflation is real and relevant. Consequently, we seek more meaningful exposure to inflation-sensitive assets than certain peers and more naïve approaches.

Asset Allocation Principle: Credit Exposure, Funded From Both Stocks and Bonds

Implementation: High Yield Bonds

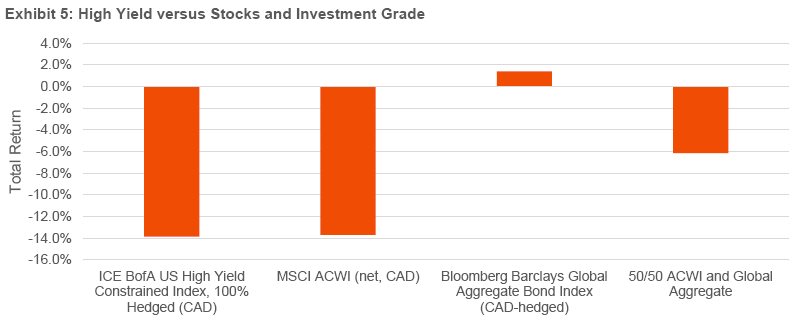

Performance discussion: Non-investment-grade credit experienced substantial losses in the quarter as economic activity plummeted and yield spreads between investment-grade and non-investment grade bonds skyrocketed. High yield, though it pays fixed coupons like traditional fixed income, is highly exposed to the economic cycle like equity. As such, we view them it as a “hybrid” asset class consisting of both equity and fixed income exposure, and our allocations to it reflect this perspective. While this framework benefited our Strategies compared to funding such allocations strictly from investment-grade bonds (which performed far better), credit exposure nevertheless detracted from portfolio returns over the quarter. Using a 50/50 combination of global equities (MSCI ACWI Index – Net) and global fixed income (Bloomberg Barclays Global Aggregate Index – CAD hedged) as a “hybrid” proxy, high yield debt lagged this reference portfolio during the quarter.

Strategy-level impact: Assuming a 5% allocation to high yield, this would have detracted roughly 35 to 40 basis points at the portfolio level compared to the 50/50 hybrid proxy.

Why this is an important strategic holding in our Strategies: High-yield debt offers higher expected returns than investment-grade bonds as compensation for both credit and liquidity risk. While these risks do relate to risks in other portions of the portfolio (namely, equities), they are not perfectly correlated, meaning this exposure should offer valuable diversification benefits in the context of a total portfolio. Our exposure to high-yield, while relatively modest, contributes positively to overall expected portfolio risk-adjusted returns.

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.