Sticking with Value: Patience and Persistence Required

Over the long run, value investing has generally outperformed the broader U.S. equity market when it comes to building wealth. Patient investors who have stayed true to a value-minded philosophy over several economic cycles have seen compelling results as the market eventually recognised the underlying worth of the assets.

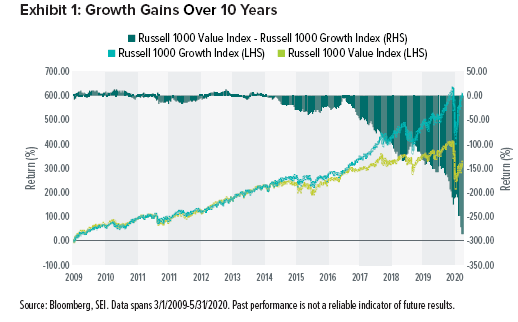

However, in the five-month period ending May 31, 2020, the Russell 1000 Value Index trailed the Russell 1000 Growth Index by over 20%. Since the end of the global financial crisis in March 2009, the Russell 1000 Value Index has lagged the Russell 1000 Growth Index by more than 5% annualised. In periods like this, when a particular area of the market underperforms relative to expectations over a long period of time, some investors are understandably tempted to stray from a commitment to their original philosophy. Exhibit 1 highlights the growing disparity between growth and value over the last several years.

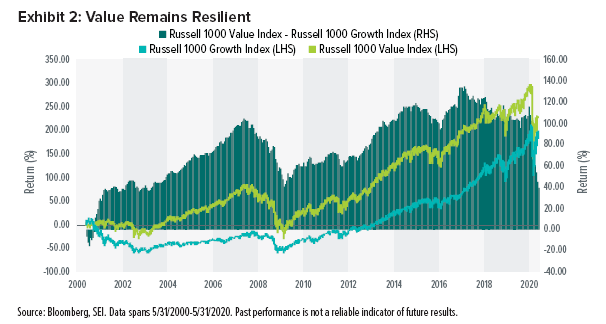

While value occasionally lagged growth over the last 20 years, value-oriented portfolios recovered each time—at least for investors who stayed the course. Despite the outperformance of growth stocks over the last 10 years, we need not look far back beyond the 10 years to witness the potential consequence of straying from value (as shown in Exhibit 2).

Over the 20-year period ending May 31, 2020, the Russell 1000 Value Index returned 6.1% annually, beating the Russell 1000 Growth Index at 5.4%. Value investors were challenged to remain patient through multiple periods when the benchmark Index underperformed its growth counterpart, but the index still came out ahead over full the 20-year period.

The temptation to believe that “this time is different”—that the benefit of value investing has actually run its course—becomes stronger when the outperformance of growth is fresh in investors’ minds. It is especially difficult to keep perspective when the stocks moving the growth index are those that typically receive the most media attention, including some of the larger technology companies.

There have been bouts of relatively concentrated outperformance within mega-cap growth stocks versus the broader U.S. equity market in the past several years. Such periods often raise questions among investors about whether or not there is still a need to include value names in their portfolios. In our view, there is always a need for value exposure.

Whenever we invest in an asset class, our decision is about future opportunities. We think the lofty price of growth stocks currently suggests that near-term upside potential is limited. Although value seemed to show signs of a recovery over the last two weeks of May, we believe it’s important to be wary of trying to “market time” a catalyst or specific style to be in favour. While valuation spreads are wide, and there should be some reversion to the mean, we think it would still be a stretch to say with certainty that now is the exact time to buy value.

Catalysts are often difficult to see or predict. Accordingly, as always, we believe in a diversified approach to investing. In view of the vast uncertainties facing investors, the “prediction game” is arguably even more challenging than usual. We do not think it best to assume that growth stocks will always be on top—nor do we think investors should attempt a move to value that is perfectly timed with a market shift. Rather, we believe that investors are better positioned for long-term success when seeking a diversified portfolio that encompasses both asset classes, while also taking value’s historical long-run outperformance to mind. Recent volatility and sharp style rotations should serve as reminders that trends do not last forever.

Index Definitions

Russell 1000 Growth Index: The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

Russell 1000 Value Index: The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Index returns are for illustrative purposes only, and do not represent actual performance of an SEI Fund. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.