Virus Spread Rattles Markets

The coronavirus outbreak has accelerated in recent days, amplifying the anxiety of already-concerned investors about its impact on global growth and corporate earnings. As a result, global equity-market volatility has increased and share prices have declined. These events have understandably brought back some of the investor fear felt during the 2008 market meltdown.

We expect volatility to continue for the short-term—as long as the extent of the impact on global economic activity remains unknown, which will likely be until the virus runs its course. But once it does, we have every reason to believe that business activity will return to normal.

Market indicators: mixed messages

We are seeing a mix of current global economic news:

- Initial (“flash”) U.S. Purchasing Managers Index (PMI) readings for February were surprisingly negative—with services at 49.4 versus an expected 53.3, and manufacturing at 50.8 versus an expectation of 51.5. (PMI readings are viewed as an indication of future economic activity. Readings above 50 are considered expansionary/positive. Those below 50 are considered contractionary/negative).

- On the other hand, eurozone flash PMIs improved unexpectedly. Manufacturing moved closer to expansion territory, increasing to 49.1 from 47.9 (beating the forecasted drop to 47.5). Services rose to 52.8 from 52.5 (surpassing an excepted deceleration to 52.2).

- Last week, China’s top leaders pledged a more proactive stance in fiscal and monetary stimulus, with the goal of limiting the outbreak’s impact on gross domestic product growth. If engaged, the efforts are expected to be broad-based. China also recently announced measures to alleviate debt pressures faced by small businesses as well as a temporary value-added tax exemption. Should the spread of the coronavirus slow, this stimulus boost could provide a tailwind to China’s domestic economy and create the potential for a quicker recovery.

- As of last Friday, February 24, 2020, S&P 500 Index blended revenue growth showed some upside surprise for the fourth quarter of last year. FactSet showed blended earnings growth for the Index in the final quarter of 2019, at 0.9% versus an expectation of -1.7%, with 87% of companies reporting actual results. In addition, there are encouraging results on the revenue side. Fourth-quarter blended revenue growth came in at 3.6% versus 2.9% forecasted, with 66% of companies beating top-line estimates. Obviously, the concern is in the future earnings guidance coming from companies after they evaluated the impact of the outbreak on their businesses. Of the 89 companies in the S&P 500 Index that issued their future earnings-per-share guidance, 61 guided lower for the first quarter of 2020—but that’s more or less in line with five-year averages. Anecdotal comments from U.S. companies have mostly noted supply-chain disruptions due to reduced business activity in China.

Portfolio managers: business as usual

The coronavirus only became a prominent investor concern about a month ago. As such, we have seen little impact on the general views of our international and emerging-markets managers, their ability to carry out their investment processes, or the way our managers cover stocks. While this could change if the problem persists, we would anticipate any disruption to be temporary.

In terms of on-the-ground activity, although mainland China is essentially shut down and Korea is on high alert, other cities (including Hong Kong and Singapore) are still accessible despite much less traffic. Singapore, in particular, is mostly business-as-usual despite the cancellation of large gatherings like conferences.

While investment manager research trips may be cancelled, phone and virtual meetings are still taking place, and networks of contacts continue to provide the same level of information, research and local insight.

Markets: muted outlook

As for the impact on stocks, the biggest uncertainty is how long this virus will last. Unfortunately, the forecast changes daily and there are many unknowns. While our managers are closely monitoring the situation, they have not made material changes at this point.

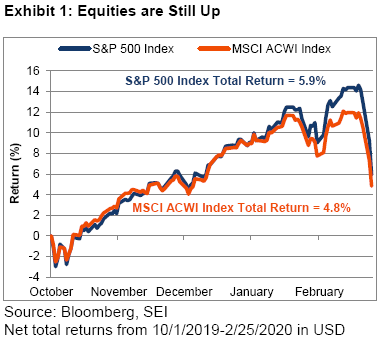

It’s also worth noting that major equity markets are still well-above where they started the fourth quarter of 2019 despite the sharp decline over the last few days. Extending that outlook back in time would reinforce the significant gains equities have posted in recent years. Some degree of pullback, whether virus-driven or not, is to be expected.

Important Information

SEI Investments Canada Company, a wholly-owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment. This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affiliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain "forward-looking information" ("FLI") as such term is defined under applicable Canadian securities laws. FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

There are risks involved with investing, including loss of principal. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations.