The “Great Rotation”

Recent market chatter has hinted at the notion of a “Great Rotation” in U.S. equities, suggesting that investors may be:

- Selling bonds and buying riskier assets such as small-cap, emerging-market and international equities, as well as commodities

- Trading out of “stay-at-home” and into “going-out” stocks

- Favouring value and cyclical sectors over growth names

While we have seen some evidence of this, we believe it is also too early to tell if this is the beginning of a major secular shift in equity investment themes. If it does turn out to mark the beginning of a long-lasting shift, when did it start, and what have we seen so far? Various starting points have been suggested, spanning anywhere from early September to “Pfizer Monday” in November, when the drug marker first announced promising results in its coronavirus trials.

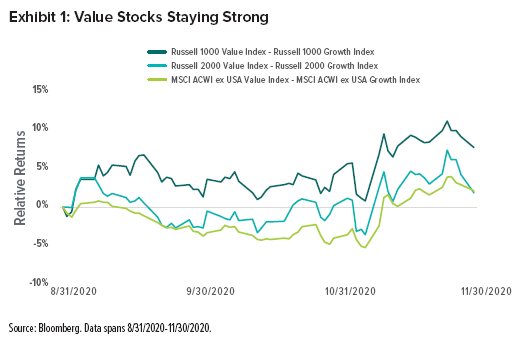

Since September, value style equity indexes have outpaced their growth counterparts to varying degrees across geographies and market capitalisations, most notably in U.S. large caps (Exhibit 1).

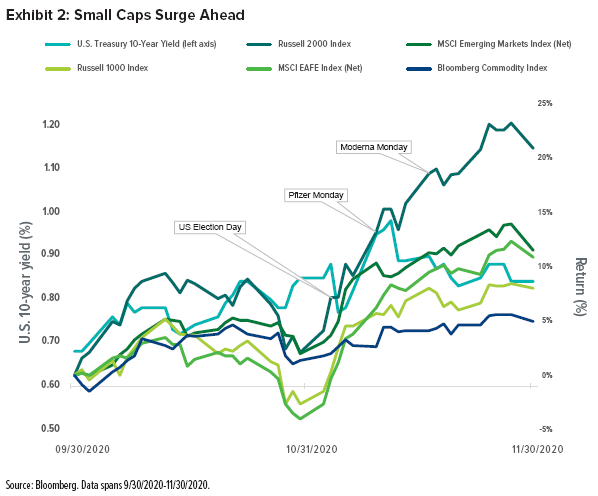

In October, U.S. Treasury yields started to tick up, at least partially owing to markets pricing in the potential for a Democratic sweep in the November election, which would have been expected to yield a larger fiscal expansion in the quarters ahead.

Since then, longer-dated Treasurys have posted negative performance; the U.S. 10-year yield climbed from 0.68% at the start of October to 0.84% two months later. Over the same period, U.S. small caps have outperformed, followed by international and emerging-market equities, while U.S. large caps have trailed. Commodities have also been broadly positive in the fourth quarter (Exhibit 2).

Since then, longer-dated Treasurys have posted negative performance; the U.S. 10-year yield climbed from 0.68% at the start of October to 0.84% two months later. Over the same period, U.S. small caps have outperformed, followed by international and emerging equities, while U.S. large caps have trailed. Commodities have also been broadly positive in the fourth quarter (Exhibit 2).

A Whole Lot of Value

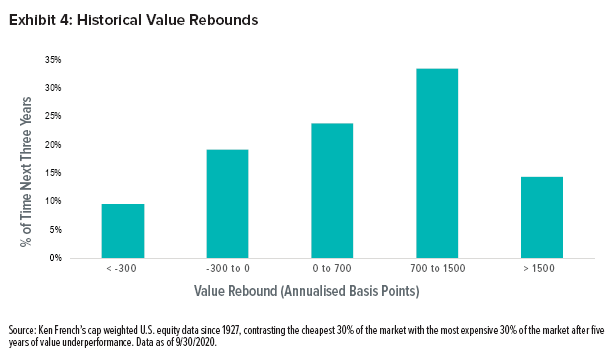

Ken French data show that prolonged periods (defined as rolling five-year time horizons) in which value underperforms have historically more often than not been followed by significant outperformance by value over the following three years. Value has rebounded and outperformed in more than 70 percent of these scenarios since 1927.

It’s not just the frequency, but also the magnitude of the gains generated by these formerly unloved stocks. In about one-third of observations, value stocks outperformed by an average of 7 percent to 15 percent annually. In nearly 15 percent of instances, value’s outperformance exceeded an annualised 15 percent.

While the returns in Exhibit 4 appear quite attractive, they also came after periods of underperformance. Even after accounting for the recent rebound in value, the current environment is one of the longest and most significant periods of value’s underperformance on record.

Extended periods of drawdowns to long-term alpha sources have historically been followed by rebounds in those same alpha sources. A disastrous period from 1998-2000 for value was followed by an extended run over the following six years. Excesses tend to correct over time, and severe excesses typically correct more sharply.

We are already observing several signs of potential normalisation. Announcements of highly effective vaccines have shaken the worries that the pandemic would last forever, while regulatory developments on both sides of the Atlantic have hinted that the run of large technology companies might no longer be as simple, forever or profitable as some investors have grown accustomed.

Our Portfolios

Our portfolios are diversified across a number of factors, including value, momentum, stability1, size and quality. While our value tilt has detracted over the past decade, history has shown that the times when value has been hard to embrace have also been the times when it has typically provided subsequent payoffs.

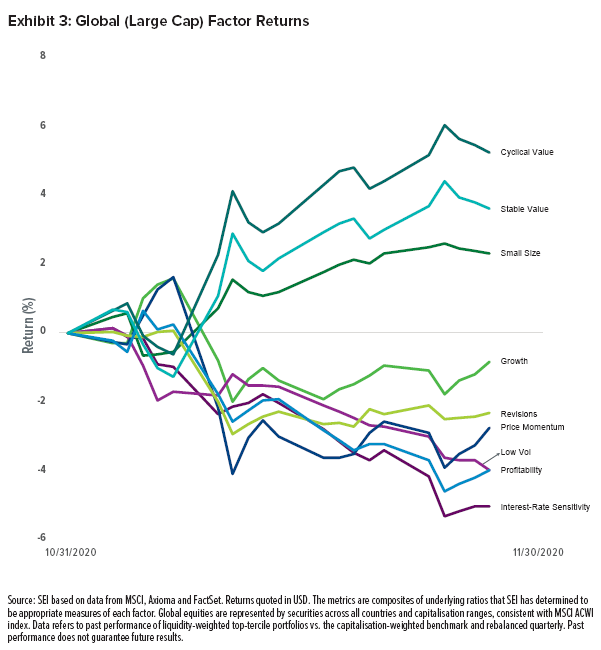

In the U.S. large-cap space (as measured by the Russell 1000 Index), a style rotation has been evident over the three months ending November 30, with fits and starts in between. In November, from a factor perspective, cyclical value had a more pronounced move; high volatility and companies in weak financial condition tended to fair best, while profitability and low-volatility characteristics were significant underperformers.

Our large-cap value sub-advisers have outperformed broader index benchmarks through holdings in the financials, materials, and industrials sectors. Despite holding overweights to some less cyclical sectors like consumer staples and healthcare, our large-cap portfolios have performed well.

Value managers in our U.S. small-cap portfolios generally contributed positively to performance. Some value managers bought restaurants, airlines, and cruise companies that have been great performance-turnaround stories. However, overweight allocations to stability managers had the greatest negative impact on relative performance and outweighed the positive performance from value within small caps.

Our international equity portfolios continued to favour value and were able to rotate into COVID-selloff names in November, although underweights to energy, the best-performing sector during the month, detracted.

Our Take on the Recent Performance

We are now seeing pockets of value starting to outperform. There is a strong case to be made that value is a coiled spring that may be in just the early stages of a release. The Russell 1000 Growth index remains approximately 50 percent more expensive than the Russell 1000 Value Index, and we are seeing similar valuation differences in small cap. Value remains extremely cheap compared to growth, no matter which lens you look through. The quality has not deteriorated in the cheap stocks as both the large-cap and small-cap value indexes offer about 2.0% advantage in dividend yield over their growth style index counterparts (as of November 30, 2020).

The positive results reported by vaccine makers are encouraging for the outlook of the global economy, and investors have been looking across the valley of troubling rises in COVID-19 cases and hospitalisations in their repricing of cyclical stocks.

We know that short-term performance can be noisy—at SEI, we would much prefer to study and reflect on longer periods than days and weeks—but as the financial media frames high-level narratives around it, there are important nuances often overlooked which can and do have varying impacts on our portfolios.

These developments in equity markets are certainly encouraging for how many of our portfolios are positioned, but whether recent performance marks the start of a “Great Rotation” will only be certain in hindsight.

Our Outlook

There are still risks related to the virus and its impact on the global economy, but we believe the groundwork is being laid for economic activity to return to pre-pandemic levels. Vaccines have begun distribution and additional fiscal support is on the way. Additionally, central bank rhetoric continues to indicate that policy rates are on hold for the foreseeable future, that all policy tools remain on the table, and that higher inflation would be welcomed.

At SEI, we have suggested that recessions have a way of shaking up leadership trends in financial markets, and we are optimistic on several fronts that investors could continue to shift from stay-at-home-oriented assets, and toward underappreciated, economically-sensitive assets that should stand to benefit most from strengthening global economic growth in 2021—this continuation would give us more confidence that a secular style change is underway.

We believe the current performance gap between growth and value still represents what may be the most attractive investment environment for value stocks that we have seen in nearly 20 years.

Over the next several years, signs of a continued value recovery should be overwhelmingly clear. Economic activity will likely normalise, with vaccines or natural immunity, while fiscal spending and accommodative central bank policy will likely lead to higher inflation.

As the market prices in such developments, “long-duration” growth and expensive high-profitability stocks should be pressured, while momentum investors are likely to rotate into new themes, potentially adding more fuel to the value rally.

Important Information

SEI Investments Canada Company, a wholly owned subsidiary of SEI Investments Company, is the Manager of the SEI Funds in Canada.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Funds or any security in particular, nor an opinion regarding the appropriateness of any investment.

This commentary has been provided by SEI Investments Management Corporation (“SIMC”), a U.S. affliate of SEI Investments Canada Company. SIMC is not registered in any capacity with any Canadian regulator, nor is the author, and the information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from qualified professionals. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Funds.

This material may contain “forward-looking information” (“FLI”) as such term is defined under applicable Canadian securities laws.

FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds and bond funds will decrease in value as interest rates rise.

Information contained herein that is based on external sources is believed to be reliable, but is not guaranteed by SEI Investments Canada Company, and the information may be incomplete or may change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.